Acadia Healthcare Company (ACHC) Stock Could Be 108.3% Overvalued After Expansion News

Acadia Healthcare Company, Inc. ACHC | 0.00 |

Recent headlines around Acadia Healthcare Company (ACHC) focus on its facility expansion and new partnerships as demand for behavioral health services grows. This has drawn investor attention to how this capacity buildout could influence future earnings power.

The recent facility expansion story comes alongside a strong recovery in Acadia Healthcare Company’s share price, with a 1-day share price return of 5.83%, a 30-day share price return of 8.04% and a year-to-date share price return of 74.04%. However, the 3-year total shareholder return is still down 67.16%, indicating near-term momentum but a longer-term hole to climb out of.

If Acadia’s growth plans have caught your attention and you want to see what else is shaping the future of care, it is worth scanning a wider field of behavioral and medical technology names through the healthcare focused AI stock screener, starting with 40 healthcare AI stocks.

With Acadia Healthcare Company’s shares rebounding sharply this year but still lagging over 3 years, and trading below the average analyst price target, the key question is whether there is still an attractive entry point or if the current price already reflects the company’s future growth prospects.

Most Popular Narrative: 108.3% Overvalued

According to the most followed narrative, Acadia Healthcare Company’s fair value of $11.94 sits well below the last close of $24.87. This puts a spotlight on how its long term earnings power is being framed.

ACHC’s valuation often reflects investor concern around margins and regulatory scrutiny. However, it may understate the company’s long-term positioning within a structurally growing healthcare segment.

This is not a high-growth technology story. It is a capacity-and-execution story in a market where demand is persistent and under-supplied. If Acadia continues to expand responsibly while maintaining care quality, its relevance is likely to increase rather than fade.

Want to see what sits behind that gap between fair value and share price? The narrative leans heavily on future profitability, measured margins, and a valuation multiple usually reserved for steadier compounders.

Result: Fair Value of $11.94 (OVERVALUED)

However, Acadia Healthcare’s narrative could shift quickly if operational issues pressure margins again or if regulatory scrutiny tightens around behavioral health reimbursement and quality standards.

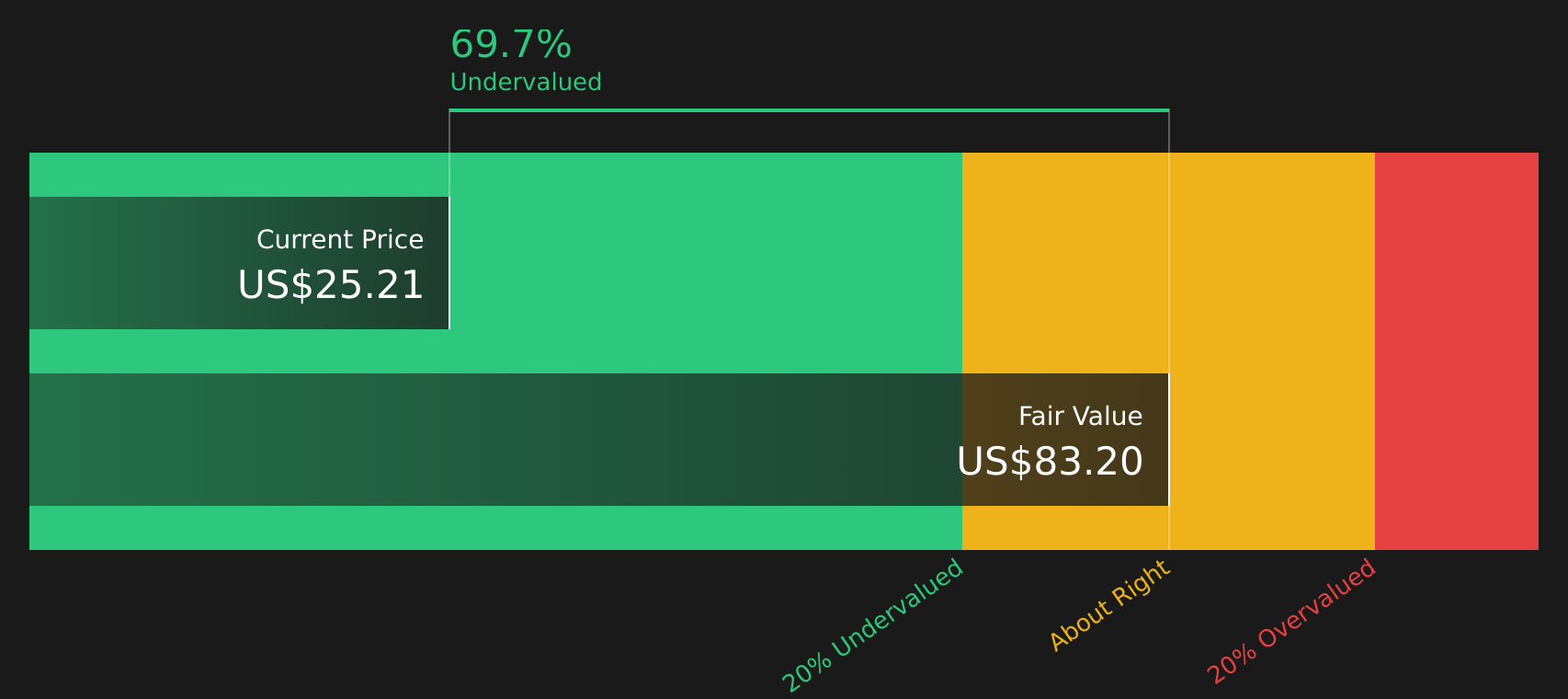

Another View: Cash Flow Signals for Acadia Healthcare Company

While the popular narrative pegs Acadia Healthcare Company as 108.3% overvalued with a fair value of $11.94, the SWS DCF model points in the opposite direction. On that view, ACHC shares at $24.87 sit well below an estimated future cash flow value of $83.20, suggesting a very different risk reward profile. Which lens do you put more weight on when both are grounded in numbers but tell competing stories?

Next Steps

With such mixed signals around Acadia Healthcare Company, it helps to look at the numbers yourself and weigh both the concerns and the upside. To see how the balance of 3 key rewards and 1 important warning sign lines up with your own risk tolerance, take a close look at the 3 key rewards and 1 important warning sign

Looking for more investment ideas beyond Acadia Healthcare Company?

If Acadia Healthcare Company has sharpened your focus on where to put fresh capital, do not stop here. Broaden your watchlist with targeted stock ideas now.

- Target potential value opportunities by reviewing companies flagged in the 45 high quality undervalued stocks before others spot them.

- Prioritize resilience first by scanning the 66 resilient stocks with low risk scores and see which stocks score well on downside protection.

- Hunt for underfollowed opportunities by checking the screener containing 19 high quality undiscovered gems that pair strong fundamentals with less crowded attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.