AdaptHealth (AHCO) Gains On Reaffirmed Buy Rating, Is It Still A Bargain?

ADAPTHEALTH CORP AHCO | 0.00 |

AdaptHealth (AHCO) shares moved after a Truist Securities analyst reiterated a positive rating following recent meetings with management, a reminder that investor sentiment often reacts quickly to updated views on a company’s outlook.

At a share price of US$10.02, AdaptHealth has seen a 7 day share price return of 3.83%, but its 90 day share price return is down 10.54% and the 5 year total shareholder return is down 63.24%. This indicates that recent optimism after management meetings and the annual stockholder vote sits against a weaker longer term record.

If this kind of mixed momentum has you thinking about diversification, it could be a good moment to scan a focused set of healthcare related AI opportunities through the 39 healthcare AI stocks

With AdaptHealth trading at US$10.02 and screening on some measures as at a discount to certain valuation estimates, the key question now is simple: are investors overlooking potential here, or is the market already factoring in future growth?

Price-to-Sales of 0.4x: Is it justified?

On simple measures, AdaptHealth looks inexpensive compared to much of US healthcare, with a Price-to-Sales (P/S) ratio of 0.4x at a share price of $10.02. However, that same multiple screens above some closer peers.

The P/S ratio compares the company’s market value with its annual revenue, which for AdaptHealth is $3.29b across sleep, respiratory, diabetes and at home wellness equipment and services. For a business that is currently loss making, P/S is often used as a rough shorthand for how much investors are paying for each dollar of sales when earnings are not yet a reliable guide.

Here, the picture is mixed. AdaptHealth’s P/S of 0.4x is described as good value against the broader US Healthcare industry average of 1.3x. This is a wide gap that suggests the market is assigning a lower value to its revenue base than to many other healthcare stocks. At the same time, that same 0.4x is described as expensive relative to a closer peer group average of 0.3x. There is also an estimated “fair” P/S of 0.6x that the market could potentially move toward if sentiment or fundamentals shift.

Against that backdrop, valuation tools indicate AdaptHealth is trading at a discount to an internal fair ratio assessment. This provides scope for investors to weigh whether the current multiple properly reflects an unprofitable company that reports annual revenue growth of 6.4% and an annual loss of $79.63m.

Result: Price-to-Sales of 0.4x (UNDERVALUED)

However, AdaptHealth still carries clear risks, including ongoing losses of $79.63m and reliance on Medicare, Medicaid and commercial payors, which could pressure pricing or volumes.

Another view on AdaptHealth: what the DCF model says

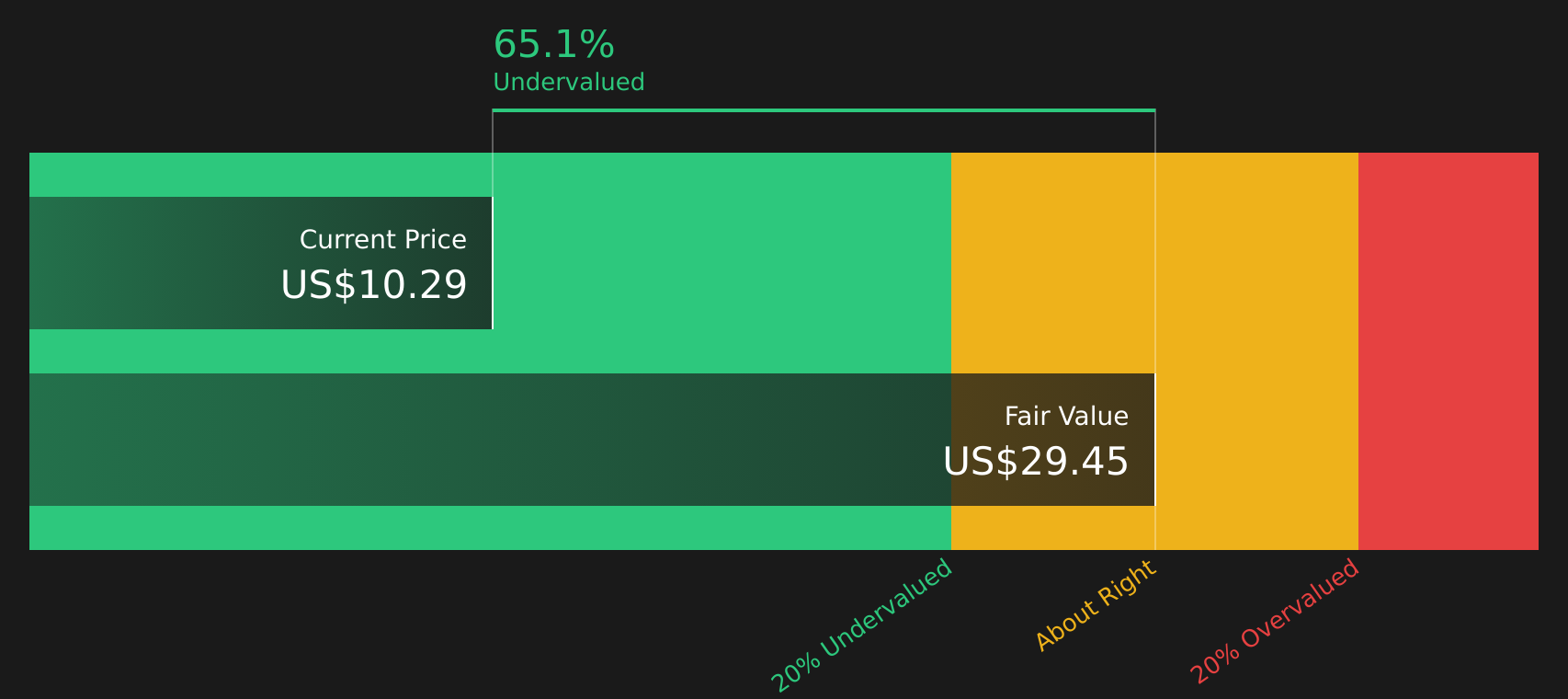

While the P/S ratio presents AdaptHealth as relatively cheap, the SWS DCF model goes further and suggests that the stock at $10.02 trades below an estimated future cash flow value of $29.54. That is a wide gap, so the key question is whether it indicates a potential opportunity or signals higher risk.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out AdaptHealth for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 43 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this AdaptHealth story has you weighing caution against potential rewards, you may want to quickly check the underlying data and then judge the balance of its prospects for yourself, starting with the 2 key rewards.

Looking for more AdaptHealth style investment ideas?

If AdaptHealth has sharpened your interest in new opportunities, do not stop here, use the Simply Wall Street Screener to keep building a broader, better informed watchlist.

- Spot potential mispricings early by scanning for companies that currently look attractively priced using the 43 high quality undervalued stocks.

- Prioritise resilience by focusing on businesses highlighted in the 67 resilient stocks with low risk scores that align with your comfort for steadier risk profiles.

- Unearth lesser known opportunities before the crowd by searching through the screener containing 19 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.