Adaptive Biotechnologies (ADPT) Stock Looks Reasonable On Cash Flow Yet Rich On Sales

Adaptive Biotechnologies ADPT | 0.00 |

Adaptive Biotechnologies stock has delivered a very strong 196.2% return over the past three years, yet the current checks suggest it no longer looks obviously cheap. The Discounted Cash Flow (DCF) intrinsic value points to a roughly fair price, while market multiples lean rich.

- Over the last three years, Adaptive Biotechnologies has returned 196.2%, which puts extra attention on whether recent gains already reflect much of the good news.

- Regulatory use of the clonoSEQ assay in trials and plans to separate the MRD and immune medicine businesses can support optimism around future cash generation, but the upsized US$300m convertible notes offering may weigh on valuation if investors focus on dilution risk.

- On Simply Wall St's broader checks, Adaptive Biotechnologies screens as expensive overall, scoring just 1 out of 6 on valuation, which signals more of a premium than a clear bargain.

The stock's next move may depend on whether the current price fairly reflects Adaptive Biotechnologies' intrinsic value or is asking investors to pay too much for its growth story.

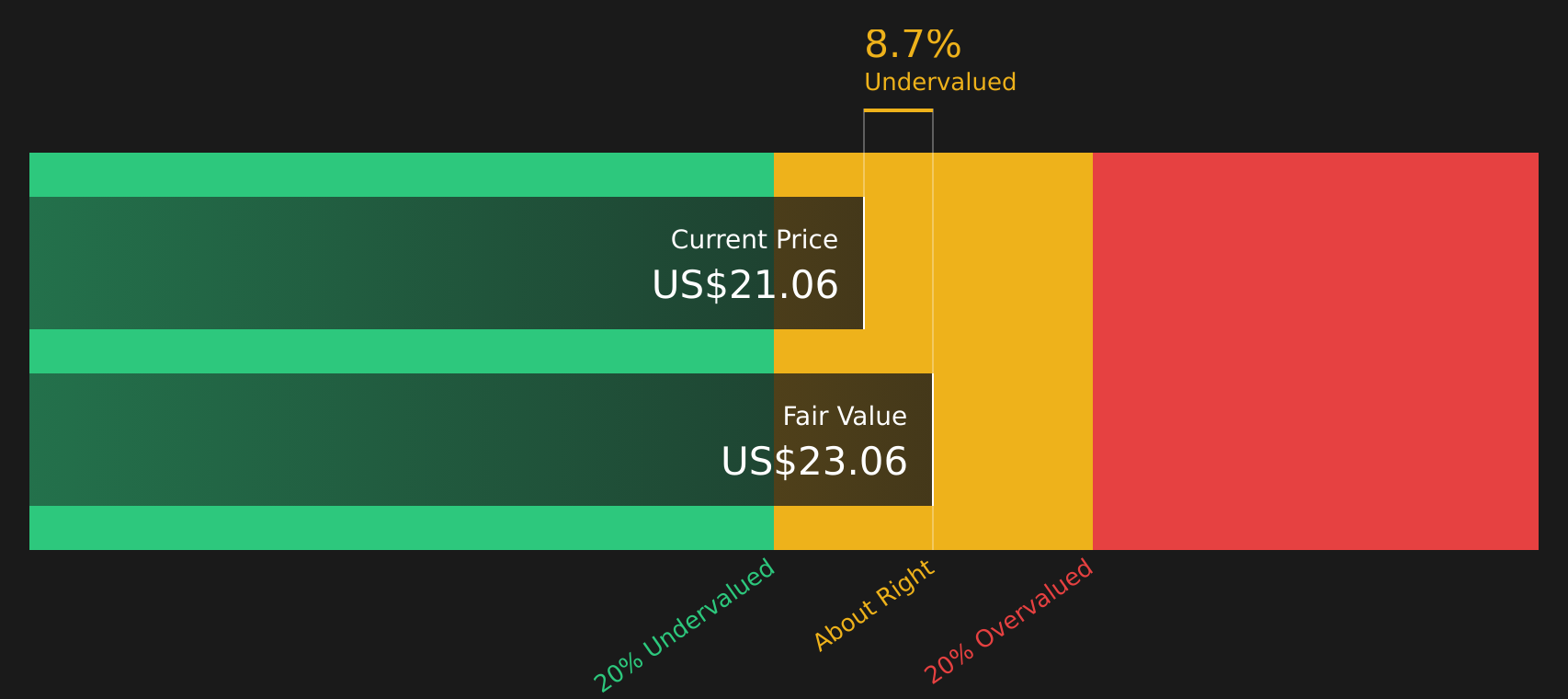

Does Adaptive Biotechnologies Look Fairly Valued on Cash Flow?

The Discounted Cash Flow (DCF) model estimates what Adaptive Biotechnologies could be worth based on projected future cash flows. The latest twelve month free cash flow is a loss of about $33.8 million, so the model assumes cash generation recovers and then grows over time from this weaker starting point.

On those assumptions, the DCF points to an estimated intrinsic value of about $23.10 per share, which implies the stock is roughly 5.6% undervalued versus the current price. The recent upsized $300 million convertible notes offering, along with the planned separation of the MRD and immune medicine businesses, helps explain why the market might hesitate to fully price in that DCF estimate despite the implied discount.

Overall, Adaptive Biotechnologies stock currently screens as approximately fairly valued, with only a modest DCF discount to the market price.

Adaptive Biotechnologies is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Has Adaptive Biotechnologies Run Too Far on Sales?

The P/S ratio suits Adaptive Biotechnologies because revenue is a more relevant anchor than earnings while the business is still reporting losses. The stock trades on a P/S of about 11.8x, compared with a Life Sciences industry average of roughly 4.2x and a peer group average near 9.5x, so the market is clearly assigning a premium to Adaptive Biotechnologies' revenue base.

The tailored fair P/S ratio for Adaptive Biotechnologies, which factors in its growth profile, margins, size and risk, is estimated at about 4.7x. That is well below the current 11.8x, indicating that investors are paying a high price for each dollar of sales relative to what this framework would typically support. Even when set against already elevated peer multiples, the stock appears stretched on this measure rather than like a clear bargain.

On the P/S multiple, Adaptive Biotechnologies stock appears overvalued compared with both its fair ratio and sector benchmarks.

The Adaptive Biotechnologies Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the Adaptive Biotechnologies valuation puzzle leaves off. They spell out which combinations of future growth, margins and earnings would need to occur for the stock to be worth materially more or less than it is today, based on scenarios that sit on Simply Wall St's Community page. Each narrative ties a fair value to a particular mix of potential catalysts and risks so you can see over time which storyline is coming through in the numbers.

Community views on Adaptive Biotechnologies are split, with one camp seeing longer term upside potential and another questioning how much is already reflected in the price.

Bull case: roughly fairly valued

"Adaptive's leadership in digital TCR antigen prediction and AI-driven immune sequencing uniquely positions the company to capture growing demand for precision diagnostics and immune monitoring..."

Bear case: 8% overvalued

"Prolonged unprofitability at the total company level, with continued operating losses and ongoing cash burn, could require dilutive capital raises or further cost-cutting..."

Do you think there's more to the story for Adaptive Biotechnologies? Head over to our Community to see what others are saying!

The Bottom Line

Adaptive Biotechnologies sits in a middle ground where the Discounted Cash Flow (DCF) view suggests only a modest intrinsic value gap, while the market-multiple view flags the stock as overvalued relative to peers and a tailored fair ratio. Broader checks line up with the idea that this is no longer a clear value play, even if the DCF implies some upside on long term cash generation. What really divides bulls and bears now is whether future growth and margins will ultimately justify the premium multiple, or whether the stock will need to grow into its valuation from here.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.