Adtran (ADTN) Stock Valuation After Patent Lawsuit Settlement Removes A Legal Overhang

ADTRAN Holdings, Inc. ADTN | 0.00 |

Patent settlement removes a legal overhang for ADTRAN Holdings (ADTN)

ADTRAN Holdings (ADTN) has resolved a multi year patent lawsuit with a non practicing entity by securing a full settlement, a dismissal of all claims with prejudice, and a payment to the company related to its counterclaims.

This legal outcome closes off a source of uncertainty around ADTRAN's intellectual property and litigation exposure, providing investors with a clearer view of the stock without this case in the background.

The latest legal settlement lands at a time when ADTRAN's share price has shown strong momentum over 90 days and year to date, while the 1 year total shareholder return is also positive despite some recent short term share price volatility.

If you are reassessing telecom and network equipment exposure after this outcome, it can be useful to widen the lens and see how other infrastructure focused stocks are trading through the 34 power grid technology and infrastructure stocks

With ADTRAN stock up 75.1% year to date and 94.4% over 1 year, yet still below some analyst price targets, investors may ask whether this legal win is still underappreciated or whether the market is already pricing in potential future developments.

Most Popular Narrative: 22.1% Undervalued

With ADTRAN trading at $15.20 against a narrative fair value of $19.50, the gap between price and modelled outcome is hard to ignore.

Expanding global demand for high-speed broadband, particularly residential fiber upgrades and multi-gigabit services, is fueling strong customer wins and backlog growth across both North America and Europe, supporting continued revenue acceleration over the coming quarters. Rising infrastructure investment for AI computing, cloud, and 5G densification is driving higher demand for ADTRAN's optical networking solutions and cross-selling opportunities, which should boost both revenue and market share as these trends intensify.

Curious what sits behind that valuation gap? The narrative leans on steady revenue expansion, a swing from losses to profits, and a rich future earnings multiple that is usually reserved for faster growing peers.

Result: Fair Value of $19.50 (UNDERVALUED)

However, the story can change quickly if broadband investment slows or FX swings hit earnings. This would challenge both the 8.6% revenue assumptions and the rich future P/E.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

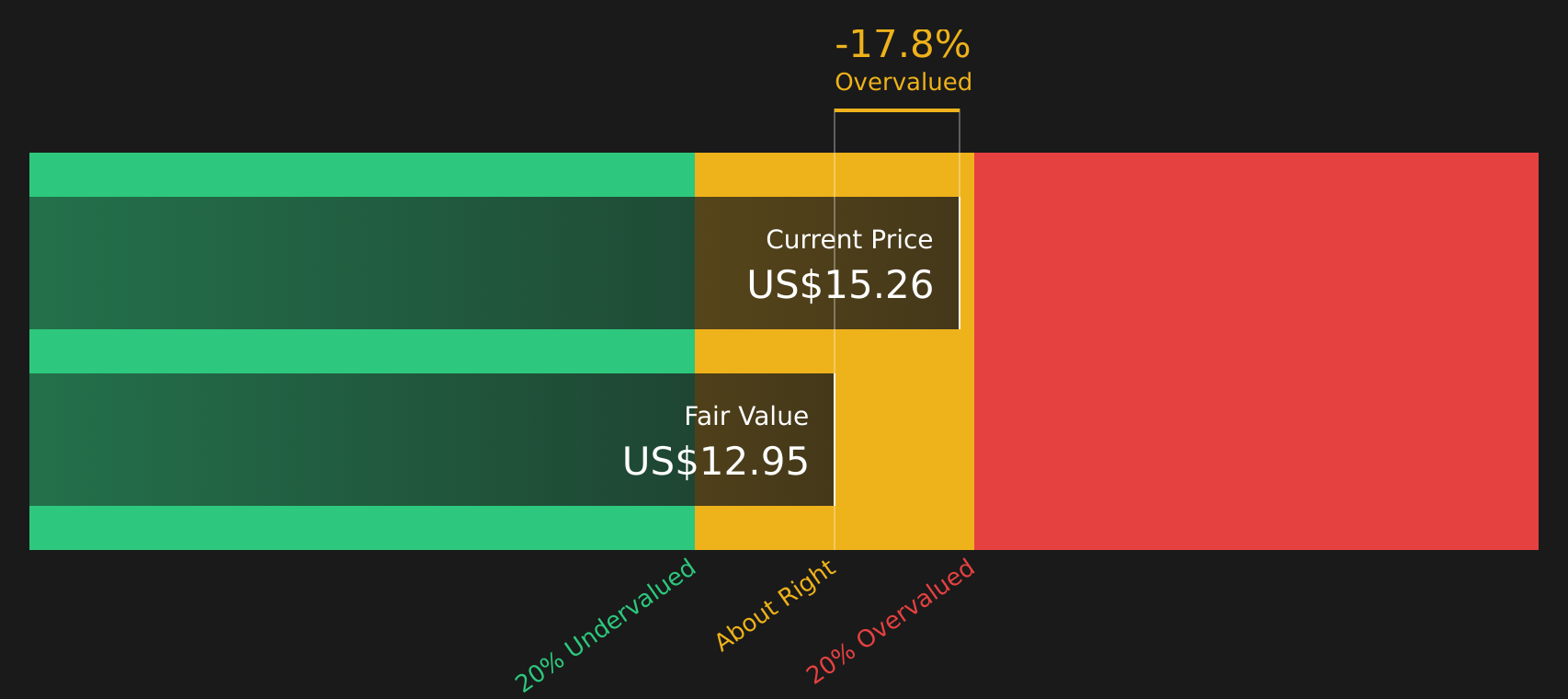

Another way to look at value

That 22.1% narrative gap points to upside, but the SWS DCF model is less generous. On this view, ADTRAN trades at $15.20 against an estimated future cash flow value of $12.94, which screens as overvalued. It raises a simple question: which story do you trust more, earnings potential or cash flows?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ADTRAN Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on value, legal clarity, and sentiment, the key question is what you think happens next. Take a closer look at both sides of the story and weigh the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If ADTRAN has sharpened your thinking, do not stop here. Use the Simply Wall Street Screener to uncover fresh stock ideas that fit your style.

- Spot potential bargains early by scanning screener containing 20 high quality undiscovered gems that align with stronger fundamentals before they appear on everyone else's radar.

- Prioritise resilience and capital preservation by reviewing 67 resilient stocks with low risk scores that score well on stability and downside control.

- Target quality first by focusing on companies in the solid balance sheet and fundamentals stocks screener (47 results) that combine financial strength with consistent fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.