Affirm Holdings (AFRM) Valuation Check After New Intuit And Expedia Partnerships

Affirm AFRM | 46.31 | +1.69% |

Affirm Holdings (AFRM) is back in focus after unveiling exclusive, multi year partnerships with Intuit’s QuickBooks Payments and Expedia Group. These moves plug its pay over time offering into two large, existing user bases.

Despite a string of new partnerships with Fiserv, Bolt, Expedia Group and Intuit, the stock has recently cooled, with a 30 day share price return of 16.26% and a year to date share price return of 16.26%. Even so, longer term total shareholder returns remain very mixed, with a 1 year total shareholder return of 3.52%, a 3 year total shareholder return above 2.5x, and a 5 year total shareholder return that is still down 49.50%. This suggests sentiment has swung sharply at different points as investors reassess growth potential and risk around the buy now, pay later model.

If payment trends like buy now, pay later have your attention, it may be worth broadening your search to other high growth tech and AI names via high growth tech and AI stocks.

With new exclusive deals across QuickBooks, Expedia, Fiserv and Bolt, and the share price still well below its three-year high, you have to ask: is Affirm undervalued today, or is the market already pricing in future growth?

Most Popular Narrative: 33.1% Undervalued

Affirm’s most followed narrative pins fair value at about $92.71 per share versus the last close of $61.99, framing a wide valuation gap that hinges on aggressive growth and margin assumptions in the years ahead.

Rapid growth and strong engagement with Affirm Card, an actively invested product moving toward high attach rates and greater offline usage, expands Affirm's addressable market beyond online retail, diversifies revenue streams, and drives higher frequency of transactions, which should accelerate GMV and contribute to margin improvement.

Want to see what kind of revenue ramp and margin lift sit behind that $92.71 figure? The narrative leans on faster top line gains, rising profitability and a richer earnings multiple than many financial peers. Curious how those ingredients combine into a 33.1% gap to today’s price? The full story is in the detailed projections, not the headline number.

Result: Fair Value of $92.71 (UNDERVALUED)

However, this upbeat story can crack if a major merchant exits, or if rising competition and credit losses start to pressure margins and growth expectations.

Another View: High Multiple Flags A Different Risk

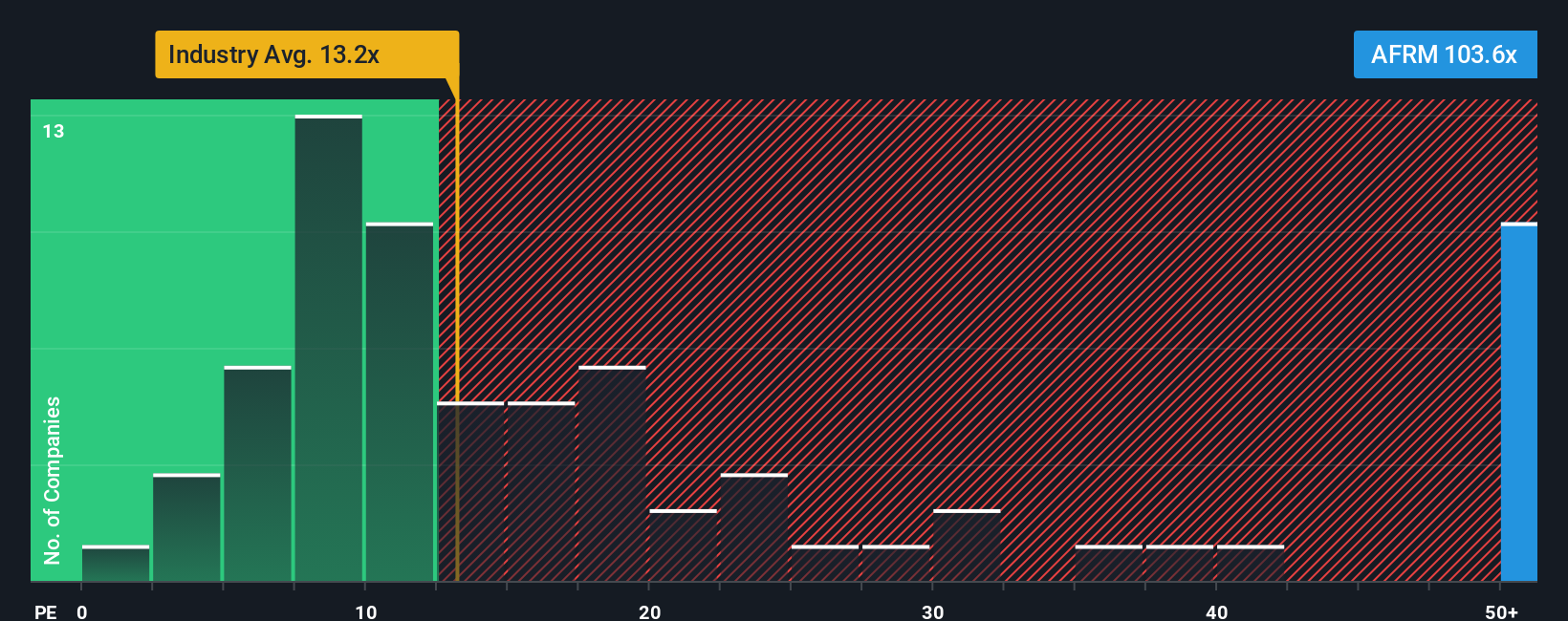

Analysts see Affirm as 33.1% undervalued on earnings forecasts, but the current P/E of 87.8x is far above the US Diversified Financial industry at 15.3x, the peer average at 28x, and a fair ratio of 29.5x. That kind of gap can cut both ways. Which signal matters more to you?

Build Your Own Affirm Holdings Narrative

If you look at these numbers and come to a different conclusion, or simply prefer to test your own assumptions, you can build a custom view in just a few minutes with Do it your way.

A great starting point for your Affirm Holdings research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Affirm has sparked your interest, do not stop there. Widen your search now so you are not relying on a single opportunity.

- Spot potential early movers by checking out these 3542 penny stocks with strong financials that pair small share prices with balance sheets and fundamentals you can actually assess.

- Target future focused themes by scanning these 112 healthcare AI stocks that connect medical demand with real use cases in artificial intelligence.

- Hunt for income ideas through these 13 dividend stocks with yields > 3% that focus on companies offering yields above 3% rather than leaving your cash idle.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.