AGCO (AGCO) Valuation Check After New AE50 Awards Recognition

AGCO Corporation AGCO | 114.59 | -2.68% |

AGCO’s AE50 awards and what they might mean for the stock

AGCO (AGCO) recently received seven 2026 AE50 awards from the American Society of Agricultural and Biological Engineers, spotlighting its agricultural machinery and technology across Fendt, Massey Ferguson and PTx brands.

For investors, this kind of industry recognition can be a useful prompt to reassess how AGCO’s product portfolio, financial profile and current valuation align with expectations for future demand and profitability.

AGCO’s AE50 wins arrive at a time when momentum has picked up, with a 1-day share price return of 5.40% and a 90-day share price return of 9.20%. The 1-year total shareholder return sits at 27.01%, while the 3-year total shareholder return reflects an 11.59% decline, suggesting more recent optimism following a weaker multi year patch.

If AGCO’s recognition in precision agriculture has you thinking about what else is out there, it could be a good moment to scan auto manufacturers for other machinery focused names riding similar themes.

AGCO’s shares have recently climbed, yet the stock still trades slightly below the average analyst price target and at a sizable implied intrinsic discount. This raises the core question: is there still an opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 5.2% Undervalued

AGCO’s most followed narrative sees fair value at about US$119.57 per share, compared with the last close of US$113.32. This points to a modest valuation gap.

AGCO's global parts and aftermarket expansion leverages both e-commerce and service innovation, capitalizing on the aging installed base and growing focus on recurring, high-margin revenues. According to this narrative, that strategy is expected to support more stable and resilient long-term earnings and margin performance across cycles.

Curious what kind of earnings mix supports that valuation uplift? The narrative leans on steadier aftermarket cash flows and a future profit multiple below many current machinery peers. Want to see how those moving parts fit together over the next few years?

Result: Fair Value of $119.57 (UNDERVALUED)

However, this hinges on farmer demand and dealer inventories improving, while tariffs and trade frictions or slower precision ag adoption could quickly challenge that upbeat earnings path.

Another View: Market Ratios Paint a Different Picture

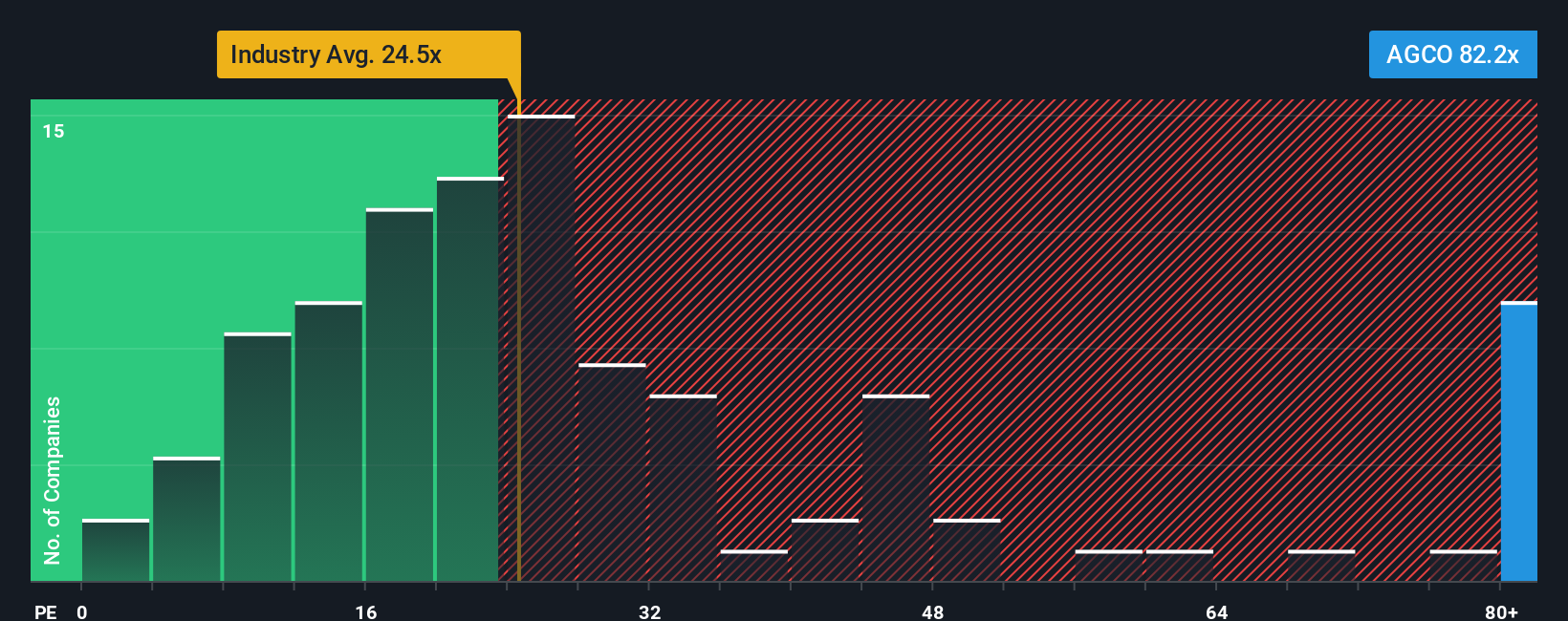

AGCO screens as good value on some metrics, yet its 22.5x P/E is slightly higher than a 21.6x peer average and lower than the 25.6x US Machinery industry and a 24.2x fair ratio. In practice, that mix suggests a limited margin of safety if sentiment cools. Which signal do you trust more?

Build Your Own AGCO Narrative

If you see the data pointing in a different direction, or just prefer to test your own thesis, you can build a full AGCO story yourself in minutes with Do it your way.

A great starting point for your AGCO research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If AGCO has sparked your interest, do not stop here. Give yourself options by scanning a few more corners of the market before you make any moves.

- Spot potential high risk, high reward names by checking out these 3546 penny stocks with strong financials that already show stronger financials than many tiny peers.

- Tap into the AI theme by reviewing these 28 AI penny stocks that already tie artificial intelligence to real products and revenues.

- Hunt for mispriced opportunities by screening these 877 undervalued stocks based on cash flows where current prices sit below cash-flow-based estimates.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.