AI Hardware Costs Are Rising and These US Equipment Stocks Stand Out

Kulicke & Soffa Industries, Inc. KLIC | 0.00 |

Stubborn import price pressure and talk of higher for longer rates are putting U.S. industrial and technology equipment stocks under a sharper spotlight, especially those tied to machinery, computers, and semiconductors. With Chinese import costs climbing and AI related hardware getting more expensive, some companies could see margins squeezed while others may find room to improve pricing power. This article explains how the latest data may affect a selection of large equipment manufacturers and what that could mean for investors. Ahead, you will see 3 stocks from the screener that may be positively exposed to this news.

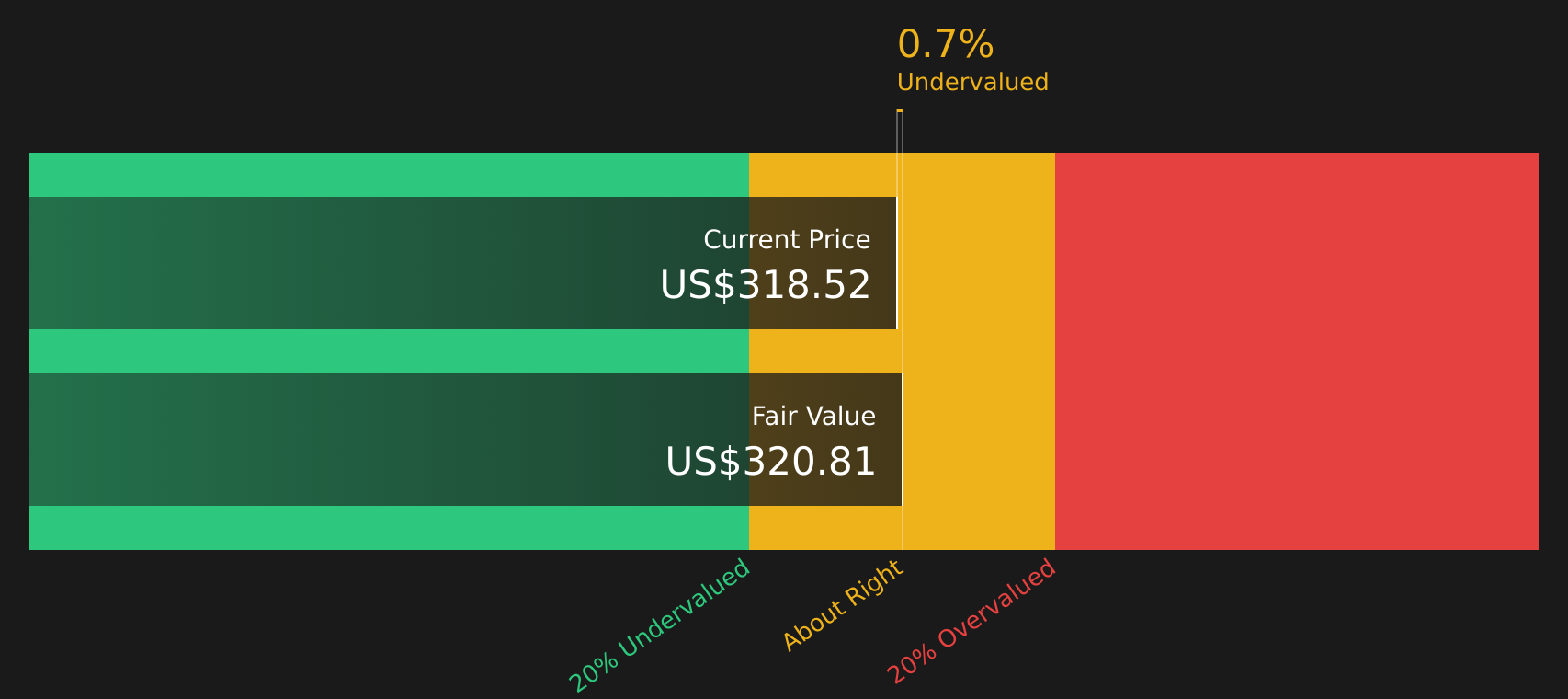

Kulicke and Soffa Industries (KLIC)

Overview: Kulicke and Soffa Industries supplies the tools and consumables that chip manufacturers use to assemble semiconductors and advanced packages, serving customers across general semiconductor, memory, power devices, LEDs and sensors. Its equipment sits in the middle of critical production flows for AI hardware, automotive electronics and broader electronics manufacturing, with a long operating history dating back to 1951 and headquarters in Singapore.

Operations: Kulicke and Soffa Industries generates most of its revenue from Ball Bonding Equipment (about US$437.5m), followed by Aftermarket Products & Services (around US$166.7m), Advanced Solutions (about US$68.6m), Wedge Bonding Equipment (about US$76.4m) and smaller contributions from All Others (about US$19.0m), with a large portion of sales linked to China and related adjustments.

Market Cap: US$5.6b

Investors looking at how rising import costs and higher AI related hardware prices could reshape supply chains may want to pay attention to Kulicke and Soffa Industries. The company sits at the heart of semiconductor assembly, with recent quarters showing stronger demand across memory, automotive and industrial markets and guidance pointing to higher revenues and earnings. At the same time, its high P/E multiple, dependence on utilization staying elevated and early stage bets on thermocompression and advanced packaging leave little room for disappointment if AI equipment enthusiasm cools. Add in insider selling and frequent one off items, and this is a stock where expectations are high and execution risk matters. This combination may make it a candidate for closer scrutiny in a higher for longer interest rate environment.

Kulicke and Soffa Industries sits at the intersection of AI excitement, high P/E expectations and supply chain pressure, and the real puzzle is how that balance holds up over a full cycle, starting with the 2 key rewards and 2 important warning signs

Nova (NVMI)

Overview: Nova Ltd. provides metrology and process control systems that help semiconductor manufacturers measure and monitor critical steps like lithography, etch, deposition and advanced packaging, so chips can be produced reliably at cutting edge dimensions. Its tools and software serve leading logic, foundry, memory and packaging customers across major chipmaking regions.

Operations: Nova generates about US$902.5m in revenue from semiconductor equipment and services.

Market Cap: US$15.0b

Nova is positioned for investors watching higher import costs and AI related equipment inflation, because its metrology systems are closely tied to global chip capacity build outs. Its supply chain is described as mostly localized, and management recently said this limits tariff pressure on gross margins to an estimated 30 to 50 basis points. The company is exposed to rising semiconductor complexity, with advanced packaging and hybrid bonding tools receiving tool of record status at major foundries. Analysts have highlighted expectations for revenue and earnings growth alongside high margins. The trade off is meaningful customer concentration, heavy R&D spend and a valuation that already reflects a strong outlook, so execution and capital allocation remain important focus areas.

Nova’s metrology tools are central to rising chip complexity and AI hardware demand, yet the full story is not in the headlines. Discover the analyst forecasts for Nova investors may be missing.

ESCO Technologies (ESE)

Overview: ESCO Technologies develops highly engineered filtration, power management, testing, and diagnostic systems used in commercial and military aviation, naval platforms, utilities, and industrial applications, with products ranging from aerospace components and electro-explosive devices to RF test facilities and electromagnetic shielding solutions.

Operations: ESCO Technologies generates most of its revenue from Aerospace & Defense at about US$600.8m, followed by the Utility Solutions Group at roughly US$383.6m and Test at around US$263.6m.

Market Cap: US$8.5b

ESCO Technologies may be of interest to investors watching reshoring and domestic supply chains, as it sells mission critical equipment to utilities and defense customers while being more of a net exporter than an importer. The utility and aerospace backlogs provide visibility, but a rich P/E ratio and the large Megger acquisition financed with new debt indicate that expectations are already high. Management has spoken about using pricing to stay ahead of inflation and tariffs. However, integration risk, tariff-related demand swings, and lower current profit margins remain important considerations. Investors may weigh whether ESCO’s combination of grid reliability, defense exposure, and testing expertise justifies that premium over time.

ESCO Technologies’ premium valuation, growing backlogs and new Megger debt raise a bigger question: how does the full picture stack up once you see the ESCO Technologies financial health report?

The three stocks covered here are only a starting point, as the full screener surfaced 45 more U.S. industrial and technology equipment companies with similarly detailed stories and risk profiles across machinery, computers and semiconductors in the U.S. Industrial and Technology Equipment Manufacturers screener. Use Simply Wall St to identify and analyze the exact catalysts, financial traits and narratives that matter to you so you can focus on the highest conviction ideas in this theme.

Take Control of Your Investment Journey

If Kulicke and Soffa Industries or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Momentum Flies

Fresh stock ideas move fast, and the best entry points rarely stay quiet for long. Before these themes gain full momentum and get crowded, review them now and act early.

- Spot resilient compounders by scanning a curated list of solid balance sheet and fundamentals (47 results) that highlights businesses built to handle shocks while others are still getting caught off guard.

- Ride secular spending trends by using the focused 35 power grid technology and infrastructure stocks to find companies positioned in the backbone of energy infrastructure while it is still under the radar for now.

- Target early AI tailwinds by reviewing the hand picked 62 profitable AI stocks that aren't just burning cash before the crowd chases headlines and pushes latecomers into less attractive risk reward trade offs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.