Airbnb (ABNB) Valuation Reconsidered After Recent Share Price Pullback

Airbnb, Inc. ABNB | 137.51 | +2.73% |

Why Airbnb is back on investors’ radar

Airbnb (ABNB) has drawn fresh attention after a recent pullback, with the share price showing declines over the past month and year that contrast with the company’s latest reported revenue and net income figures.

Airbnb’s recent 30 day share price return of a 13.6% decline and 1 year total shareholder return of a 10.6% loss suggest momentum has cooled, reflecting a more cautious stance on future growth and risk than in earlier periods.

If this shift in sentiment has you reassessing where you deploy capital next, it could be a good moment to scan 23 top founder-led companies for other ideas beyond the travel space.

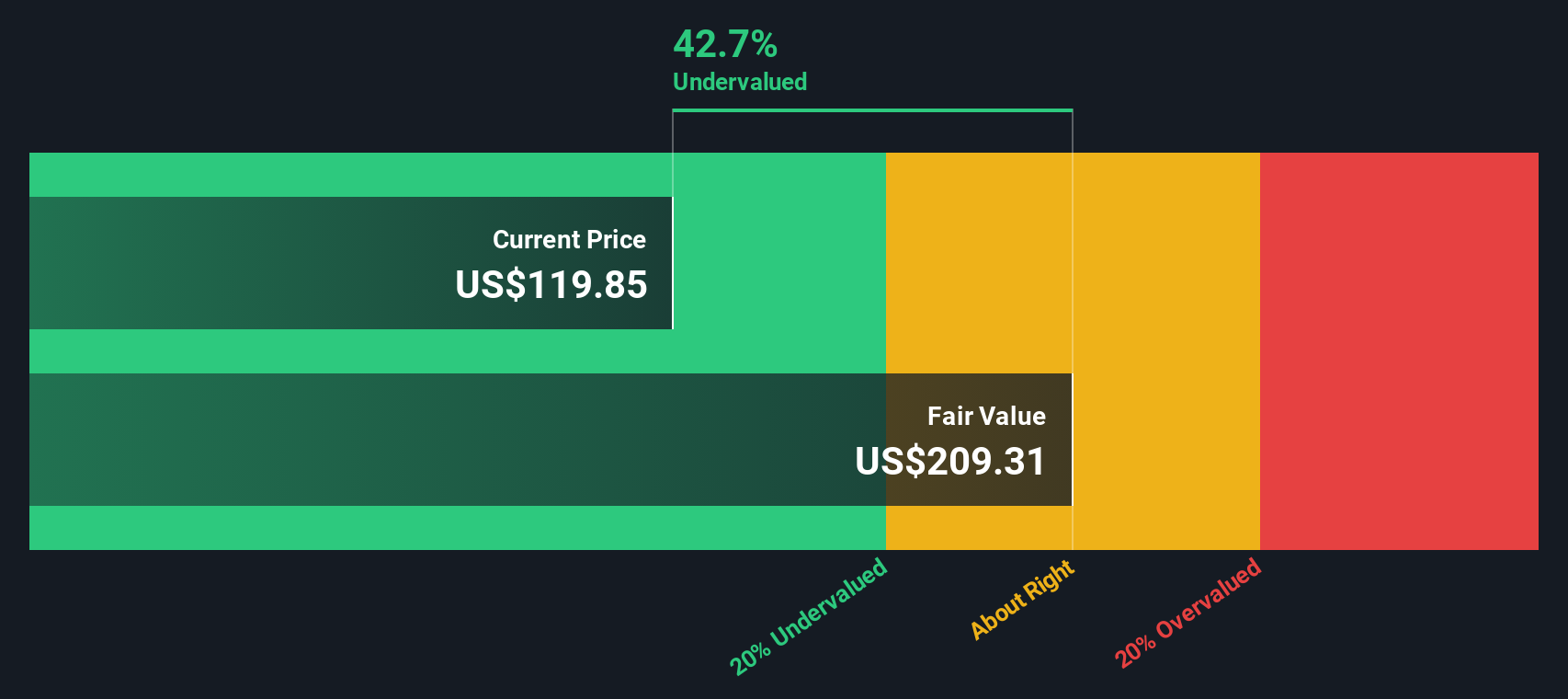

So with a recent pullback, an intrinsic discount of about 43% and revenue and net income in the billions, is Airbnb offering you a genuine value opportunity, or is the market already pricing in the growth story ahead?

Most Popular Narrative: 40% Overvalued

Airbnb’s last close around $120 lines up closely with a narrative fair value of about $120 according to TickerTickle, even though our DCF model points to a much higher figure. The story behind that fair value really matters.

International markets are now picking up the growth while the US market is cooling a bit. They’ve launched long-term rentals, made over 500 product improvements, and are going all-in on AI to make the platform smoother. It’s easier now to find the right stay without scrolling for 20 minutes.

If you are curious how a global platform, steady revenue assumptions, richer profit margins and a future earnings multiple all fit together into one valuation story, the full narrative spells out which pieces carry the most weight and how they stack up against today’s price.

Result: Fair Value of $119.83 (OVERVALUED)

However, ongoing regulatory pressure in key markets and uncertainty around the long term potential of Experiences could both weaken the current focus on growth.

Another view on value

That user narrative pins Airbnb’s fair value near $120 and calls the stock overvalued, yet our DCF model lands much higher at about $211 per share. This suggests the price could be materially below the value of future cash flows. So which story do you think is closer to reality?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Airbnb for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Airbnb Narrative

If you see the numbers differently or prefer to build your own view from the ground up, you can shape a custom thesis in minutes: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Airbnb.

Looking for more investment ideas?

If Airbnb has you thinking about what else might belong on your watchlist, do not stop here. Broaden your options and line up your next potential moves.

- Spot potential value now by checking companies on our 51 high quality undervalued stocks that pair solid fundamentals with prices that may not fully reflect them.

- Strengthen your income stream by reviewing the 14 dividend fortresses that could help anchor a portfolio with higher-yielding names.

- Lower the bumpiness of your ride by scanning the 83 resilient stocks with low risk scores that our filters flag for more resilient profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.