Akamai Technologies (AKAM) Stock After New AI Agentic Framework And Partnerships What Is The Valuation Signal

Akamai Technologies, Inc. AKAM | 0.00 |

Akamai Technologies (AKAM) has drawn fresh attention after launching a unified agentic framework that connects identity, observability, trust, and edge security into a single, real time decision layer for AI driven interactions.

The stock has pulled back recently, with a 7 day share price return of 5.4% and 30 day share price return of 11.1% from its latest close of US$134.20. However, the 90 day share price return of 26.8% and 1 year total shareholder return of 67.8% suggest momentum has been positive over a longer window as Akamai signs new AI security partnerships and expands its edge focused cloud offering.

If Akamai’s AI push has your attention, it can be useful to see what else is happening around the infrastructure that supports these workloads, including the 48 AI infrastructure stocks

With Akamai reporting annual revenue of US$4.27b, net income of US$435.18m, and trading around US$134.20, the key question is simple: is the current AI excitement already in the price or is there still a potential opportunity for investors who find the company’s profile appealing?

Most Popular Narrative: 15.8% Undervalued

Compared with the last close at $134.20, the most followed narrative sees Akamai's fair value at $159.30, built on detailed growth and margin assumptions.

The proliferation of AI applications requiring secure, ultra-low-latency infrastructure benefits Akamai's globally distributed platform, as evidenced by new AI Gateway and Firewall for AI offerings. This positions the company to capture new AI-driven workloads, supporting both future top-line growth and potentially higher net margins via value-added solutions.

Curious what revenue path and margin rebuild sit behind that fair value, and which earnings outcome range analysts are anchoring to their models? The narrative breaks down how growth in newer cloud and security lines is weighed against pressure in legacy delivery, and how a richer future P/E assumption fits into that picture.

Result: Fair Value of $159.30 (UNDERVALUED)

However, this hinges on cloud and security growth offsetting pressure in the legacy delivery segment, and on large AI related contracts scaling without squeezing margins too hard.

Another Angle: Multiples Point To A Richer Price

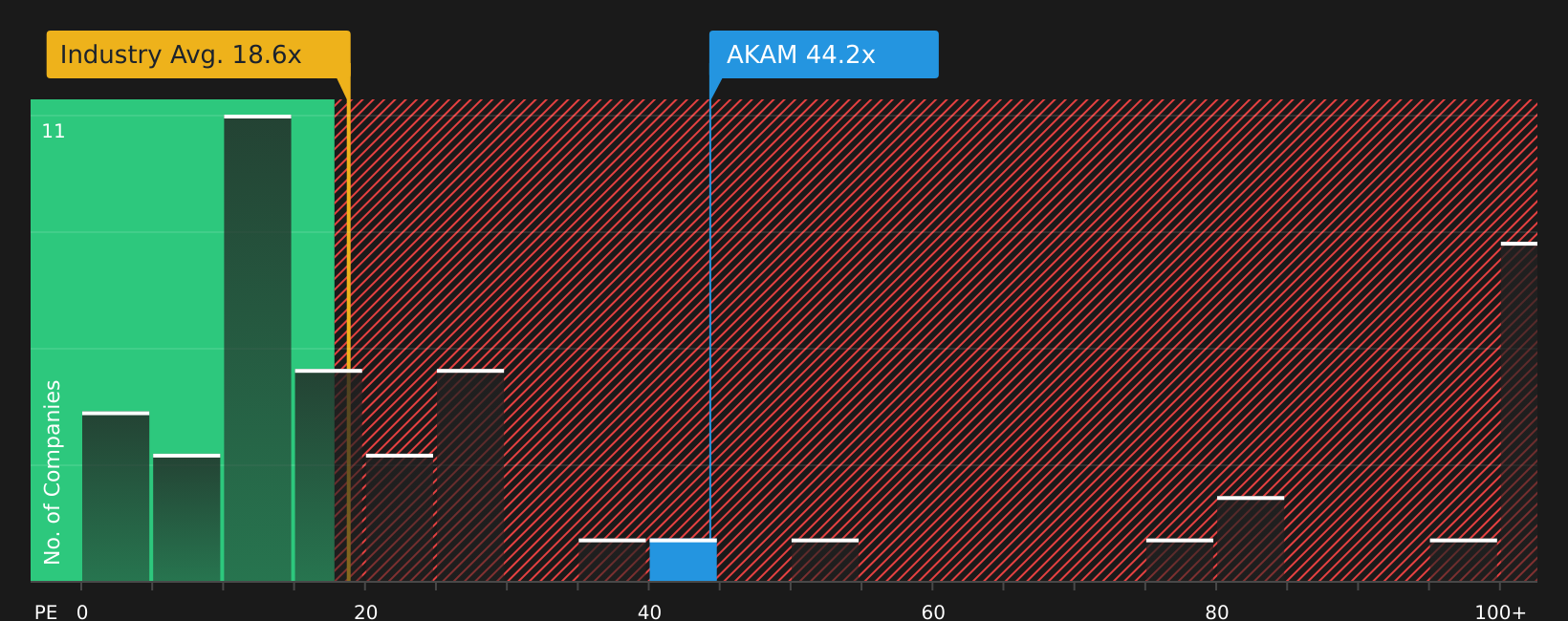

That 15.8% undervalued narrative sits alongside a very different signal from simple valuation ratios. Akamai currently trades on a P/E of 44.8x, compared with a fair ratio of 34.8x, the US IT industry at 19.1x, and direct peers at 51.1x, which suggests less room for error if growth or margins disappoint.

For investors weighing these mixed signals, it helps to see how the current P/E stacks up against what the fair ratio implies over different scenarios, and where that leaves potential valuation risk or opportunity in practice, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment clearly mixed between upside potential and valuation risk, it makes sense to act promptly and evaluate the data independently, beginning with the balance of 1 key reward and 2 important warning signs

Looking for more investment ideas?

If Akamai has sharpened your focus on AI and infrastructure, now is the moment to broaden your watchlist so you do not miss other compelling setups.

- Spot potential mispricing by scanning 47 high quality undervalued stocks that combine solid fundamentals with prices that may not fully reflect their profiles.

- Strengthen portfolio resilience by reviewing 68 resilient stocks with low risk scores that show steadier risk scores and more robust business characteristics.

- Add extra income potential by studying 9 dividend fortresses offering higher yields that could support total return over time.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.