Akamai Technologies (AKAM) Wins AI Security Backing, Is The Upside Already Priced In?

Akamai Technologies, Inc. AKAM | 0.00 |

Akamai Technologies (AKAM) is back in focus after being selected as the security backbone for World Wide Technology’s ARMOR framework for AI operations, while also earning a 2026 Gartner Customers’ Choice recognition for edge distribution platforms.

Recent AI security partnerships and customer recognition appear to be catching investor attention, with Akamai Technologies’ share price up 10.67% over one day and 15.47% over ninety days. Its one year total shareholder return of 56.98% suggests strong momentum.

If Akamai’s AI and edge wins interest you, it could be worth broadening your research beyond a single stock by reviewing 52 AI infrastructure stocks

Bulls point to Akamai Technologies’ AI security role and strong recent returns, while bears question how much of that story is already reflected in the price. The numbers behind today’s valuation help show which side the evidence leans toward.

Most Popular Narrative: 20.5% Undervalued

The most followed narrative on Akamai Technologies places fair value at $159.30 versus the last close of $126.57, framing the current AI driven optimism through a detailed set of growth and margin assumptions that sit behind that gap.

The proliferation of AI applications requiring secure, ultra-low-latency infrastructure benefits Akamai's globally distributed platform, as evidenced by new AI Gateway and Firewall for AI offerings. This positions the company to capture new AI-driven workloads, supporting both future top-line growth and potentially higher net margins via value-added solutions.

Read the complete narrative. Read the complete narrative.

Want to see what justifies that higher fair value on Akamai Technologies? The narrative leans heavily on specific revenue growth, margin expansion and a richer profit multiple. Curious which exact assumptions need to hold for that story to work.

Result: Fair Value of $159.30 (UNDERVALUED)

However, Akamai Technologies still faces the risk that heavier cloud and AI infrastructure spending will pressure margins, while dependence on a few large compute contracts leaves earnings more exposed.

Another View on Akamai Technologies' Valuation

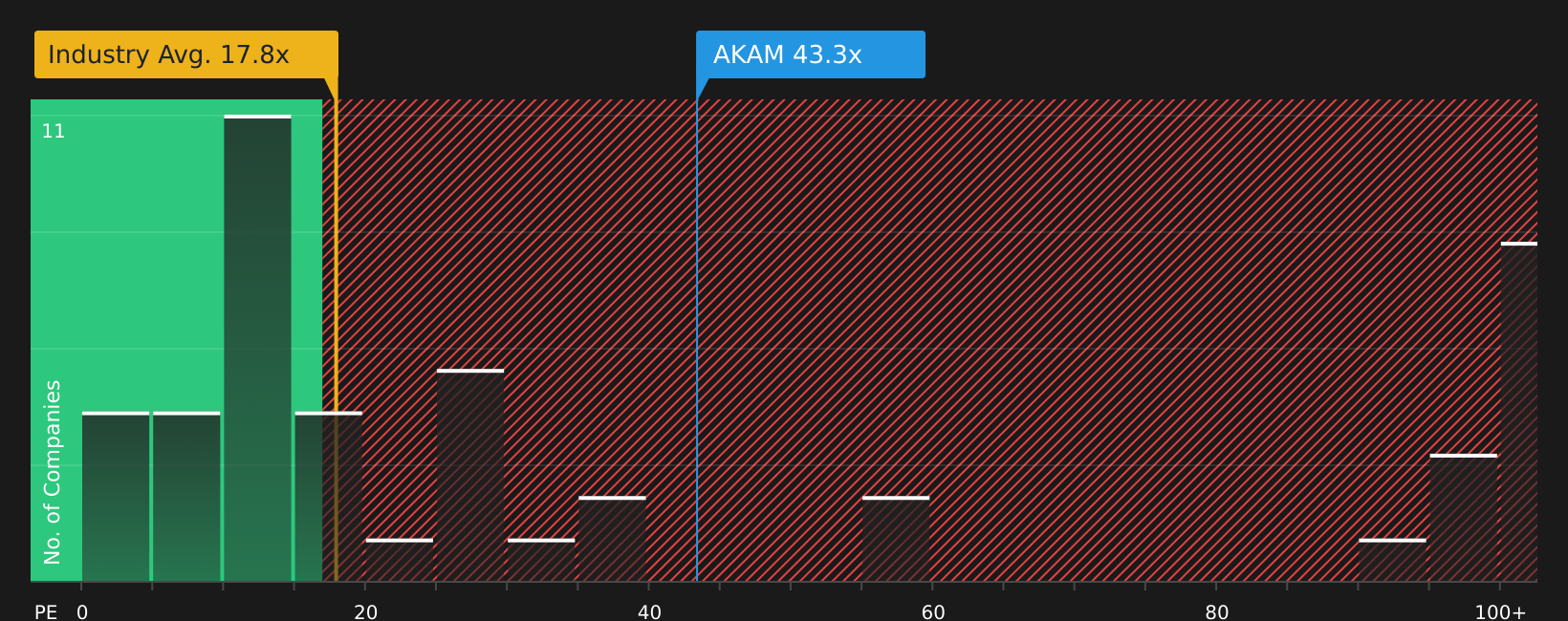

While the community narrative suggests Akamai Technologies is 20.5% undervalued based on analyst targets, the current P/E of 42.3x tells a more cautious story. That is higher than the US IT industry average of 18x and above a fair ratio of 33.4x, which points to a market that already prices in a lot of optimism.

Peers on average trade at 51.8x, so Akamai does not look stretched against that group, but the gap versus the fair ratio leaves less room if growth or margins fall short of expectations. Which reference point do you trust more when you think about valuation risk versus potential upside?

Next Steps

With sentiment split between opportunity and caution around Akamai Technologies, use this period of heightened interest to weigh the 1 key reward and 2 important warning signs.

Looking for more ideas beyond Akamai Technologies?

Do not stop at Akamai Technologies when there are other opportunities to research. Use these focused stock ideas to pressure test and strengthen your overall portfolio.

- Target quality at a discount by reviewing companies in the 44 high quality undervalued stocks that combine solid fundamentals with prices that may not fully reflect their strengths.

- Prioritise resilience and sleep easier at night by assessing stocks in the 72 resilient stocks with low risk scores that score well on balance sheet strength and risk metrics.

- Spot tomorrow's potential standouts early by scanning the screener containing 19 high quality undiscovered gems where strong business metrics have yet to attract broad market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.