Align Technology (ALGN) Stock Valuation After Earnings Beat And Renewed Investor Optimism

Align Technology, Inc. ALGN | 0.00 |

Align Technology (ALGN) has jumped back onto investors’ radar after quarterly results beat analyst expectations on both revenue and earnings per share, with bullish ratings and supportive technical signals reinforcing the shift in sentiment.

At a share price of $174.84, Align’s recent 7 day share price return of 4.23% and 30 day share price return of 11.19% suggest momentum is building again, even though the 1 year total shareholder return is slightly down and longer term total shareholder returns over 3 and 5 years remain sharply weaker.

If Align’s rebound has your attention, this is a good moment to scan the broader healthcare AI opportunity set with our 40 healthcare AI stocks

With Align trading at a discount to both one valuation estimate and the average analyst price target, yet carrying a weak 3 and 5 year shareholder return record, investors face a key question: Is there genuine value here, or is the market already pricing in whatever growth comes next?

Most Popular Narrative: 13.1% Overvalued

According to the most widely followed narrative, Align’s fair value is set at $154.62, which sits below the last close of $174.84 and presents the recent rebound in a more cautious light.

Today, Align operates in a different environment. Inflation, discretionary spending pressure, and rising competition are testing whether premium orthodontics can sustain growth without sacrificing margins.

The core narrative focuses on Align’s ability to keep margins supported while balancing premium pricing, disciplined investment, and measured growth in new markets. Investors may wish to examine which revenue and earnings assumptions sit behind that view, and how they translate into that specific fair value, before weighing this rebound against the longer term track record.

Result: Fair Value of $154.62 (OVERVALUED)

However, your thesis can be tested quickly if competitive pricing undercuts Align’s premium positioning, or if cost conscious consumers pull back on elective orthodontic treatments.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

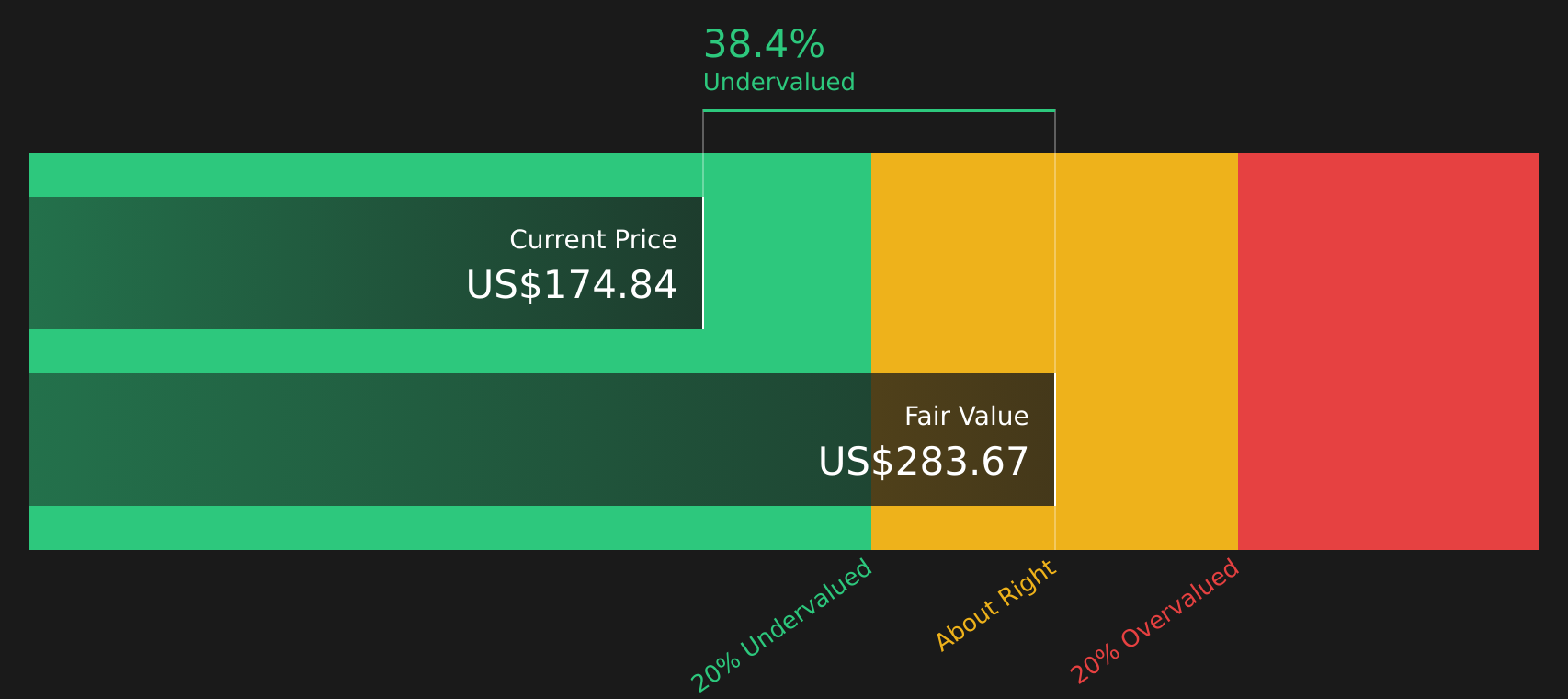

Another View: DCF Points in the Opposite Direction

While the popular narrative tags Align as 13.1% overvalued at a fair value of $154.62, the SWS DCF model paints a very different picture. On that measure, Align at $174.84 is trading roughly 38.4% below an estimated future cash flow value of $283.67, which suggests the market may be attaching a heavy execution discount. Which story do you think better reflects the risk you are willing to take on?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Align Technology for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment split between caution and optimism, this is the moment to review the numbers yourself, weigh the trade offs, and see the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If Align has sharpened your focus, do not stop here. Use the Simply Wall Street Screener to uncover fresh stocks that match your risk and return preferences.

- Target income potential with companies that have higher yields and resilient payouts by scanning the 8 dividend fortresses.

- Hunt for mispriced opportunities by sorting through the 44 high quality undervalued stocks and see which stocks the market may be overlooking.

- Prioritise resilience by focusing on companies flagged in the 71 resilient stocks with low risk scores so your portfolio is not solely exposed to higher volatility ideas.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.