Alkermes (ALKS) Advances Alixorexton As Valuation Debate Follows Phase 2 Narcolepsy Data

Alkermes Public Limited Company ALKS | 0.00 |

Why the Vibrance-2 data matters for Alkermes stock

Alkermes (ALKS) recently reported detailed phase 2 Vibrance-2 data for alixorexton in narcolepsy type 2, meeting dual primary endpoints on wakefulness and daytime sleepiness, and has now moved the program into global phase 3 trials.

For investors, this update highlights how Alkermes is positioning alixorexton within a broader neurology focused pipeline that already includes treatments for schizophrenia, bipolar I disorder, substance dependence and sleep related conditions.

Alkermes shares have shown strong momentum recently, with a 55.8% 90 day share price return and a 94.9% year to date share price return. The 5 year total shareholder return sits at 121.3%.

If the Vibrance 2 results have you rethinking where growth in healthcare might come from next, it can be useful to scan beyond a single stock using 40 healthcare AI stocks

With Alkermes trading at $55.08, above an average analyst price target of $48.13 yet at an estimated 42% discount to intrinsic value, is there still a potential opportunity here or is the market already pricing in future growth?

Most Popular Narrative: 16% Overvalued

Compared with Alkermes' last close at $55.08, the most followed narrative fair value of $47.69 suggests the current price sits above that modeled range. The story hinges heavily on how the orexin franchise plays out.

Results from the Vibrance 1 Phase II study and the expanding orexin agonist pipeline de-risk the company's long-term R&D strategy, opening avenues to additional addressable disorders beyond narcolepsy and highlighting potential for future multi-indication revenue streams pending successful late-stage trials and commercialization.

Want to understand why this narrative supports a higher earnings profile for Alkermes over time? The story leans on faster earnings growth, improving margins and a richer profit multiple than many biopharma peers. Curious which forecast levers matter most to that $47.69 fair value and how sensitive the outcome is to orexin trial milestones? The full narrative lays out the numbers behind those assumptions in detail.

Result: Fair Value of $47.69 (OVERVALUED)

However, Alkermes still faces meaningful execution risk, including higher R&D spending on the orexin program and reliance on a concentrated set of proprietary products.

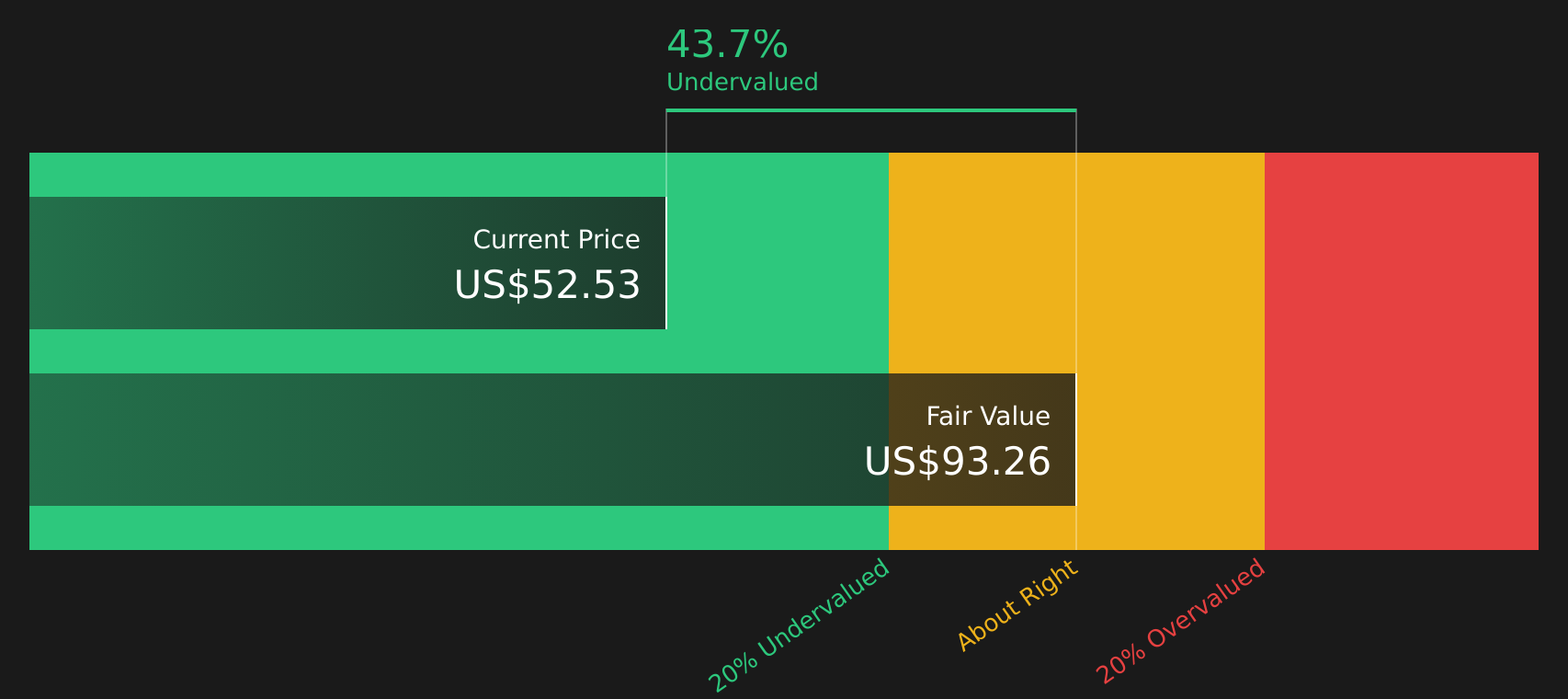

Another View: Alkermes Through a Cash Flow Lens

While the most popular narrative pegs Alkermes at 16% overvalued around a fair value of $47.69, our DCF model presents a different perspective. On that approach, Alkermes at $55.08 screens as trading about 42% below an estimated future cash flow value of $94.27. This contrast raises the question of which signal investors should focus on.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Alkermes for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on valuation and differing views on Alkermes' orexin opportunity, it helps to move quickly and stress test the assumptions that matter most, starting with 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Alkermes?

If Alkermes has you thinking differently about healthcare, do not stop here. Broaden your watchlist now so you are not late to the next opportunity.

- Spot potential turnaround candidates early by scanning 21 elite penny stocks with strong financials that combine smaller market caps with more resilient financial profiles.

- Target stronger entry points by reviewing 44 high quality undervalued stocks that pair attractive fundamentals with pricing that does not fully reflect their underlying metrics.

- Strengthen income potential by focusing on 8 dividend fortresses that aim to balance higher yields with more robust business models.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.