Alkermes (ALKS) Stock Near Fair Value After Positive Alixorexton Phase 2 Results

Alkermes Public Limited Company ALKS | 0.00 |

Alkermes (ALKS) is back in focus after unveiling detailed Vibrance-2 phase 2 data for alixorexton in narcolepsy type 2, showing statistically significant improvements in wakefulness, sleepiness, fatigue and cognition, with a favorable safety profile.

Alkermes shares have been on a strong run, with a 30-day share price return of 22.26% and a 90-day share price return of 58.42%. The 1-year total shareholder return of 53.76% and 5-year total shareholder return of 85.71% point to momentum that recent alixorexton data appears to have reinforced.

If this kind of clinical catalyst interests you, it could be a useful moment to broaden your watchlist with other healthcare companies using AI in treatment and drug development via the 38 healthcare AI stocks.

With Alkermes now trading near its analyst price target and carrying a P/E of 48.39 despite a value score of 2 and a large modelled intrinsic discount, is the market leaving room for upside, or already pricing in future growth?

Most Popular Narrative: 2% Overvalued

Compared with Alkermes' last close at $44.99, the most followed narrative fair value of $44.24 sits slightly lower, framing debates about how much of the orexin and sleep opportunity is already reflected in the price.

The company is benefitting from margin expansion efforts and cost discipline, seen in lower cost of goods sold post divestiture of lower margin manufacturing operations, which, together with growing proprietary product sales, is driving higher net margins and increasing free cash flow generation.

Curious what kind of revenue trajectory, earnings path and future P/E this narrative leans on to back that fair value? The underlying model stitches together detailed assumptions on growth, margins and discount rate to support that $44.24 figure without treating the current rally in Alkermes as the final word.

Result: Fair Value of $44.24 (OVERVALUED)

However, Alkermes still faces pressure from rising R&D spending on orexin trials and heavy reliance on a concentrated product portfolio that could be tested by competition.

Another View: Alkermes Through a Cash Flow Lens

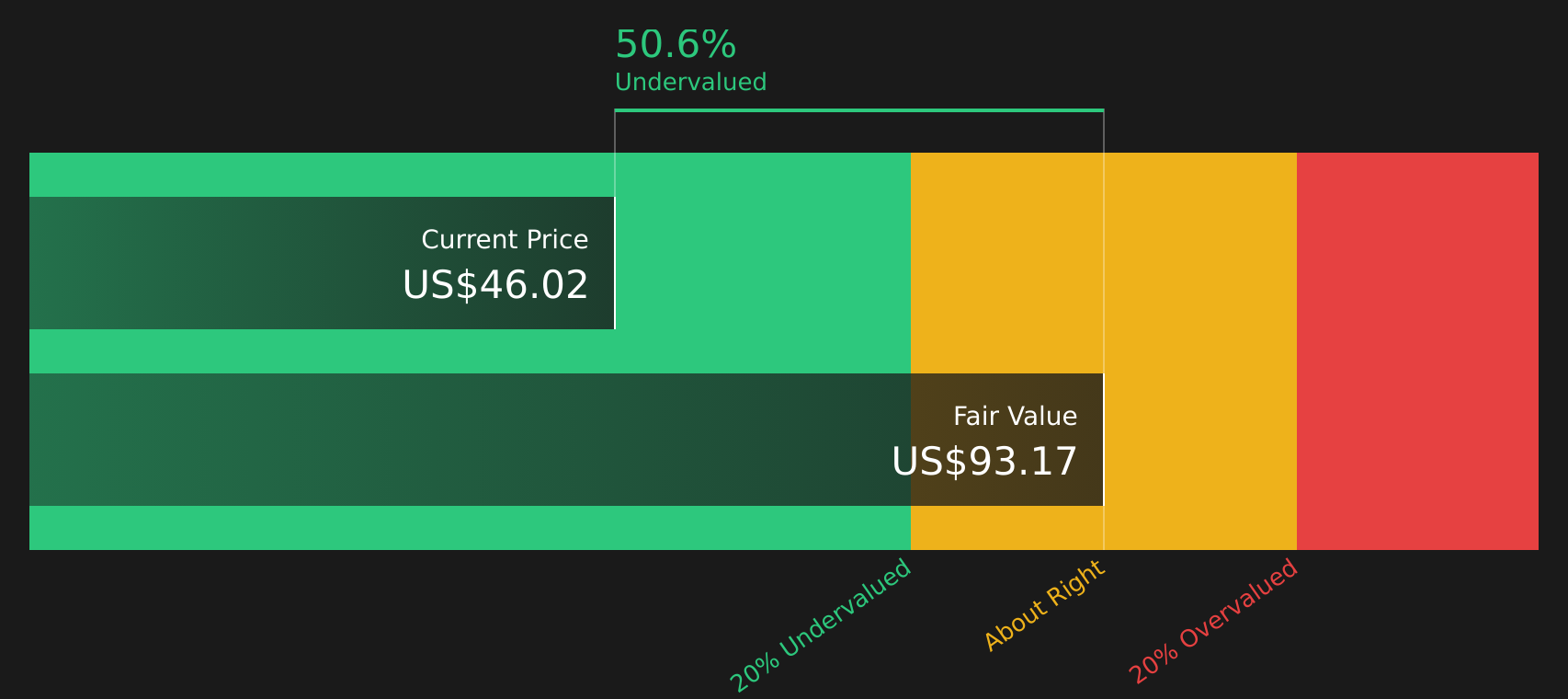

While the analyst fair value of $44.24 suggests Alkermes is slightly overvalued, the SWS DCF model points in the opposite direction, with an estimated future cash flow value of $93.53 and the shares at $44.99. When one model implies a large discount and another does not, which set of assumptions appears more realistic?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Alkermes for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals around Alkermes leave you undecided, this is the moment to look through the data and weigh the trade off between its risks and rewards for yourself by checking the 2 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Alkermes?

Alkermes might have your attention today, but you do not want to miss other opportunities that could fit your portfolio just as well or even better.

- Spot potential bargains early by scanning companies that show up in the screener containing 19 high quality undiscovered gems before they attract wider attention.

- Focus on resilience first and hunt for companies in the 66 resilient stocks with low risk scores where business fundamentals and volatility scores work in your favor.

- Prioritize financial strength and sift through stocks in the solid balance sheet and fundamentals stocks screener (48 results) so weak balance sheets do not catch you off guard later.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.