Alliance Resource Partners (ARLP) Dividend Coverage Concerns Reinforce Skeptical Income Narratives

Alliance Resource Partners, L.P. ARLP | 28.17 | +2.18% |

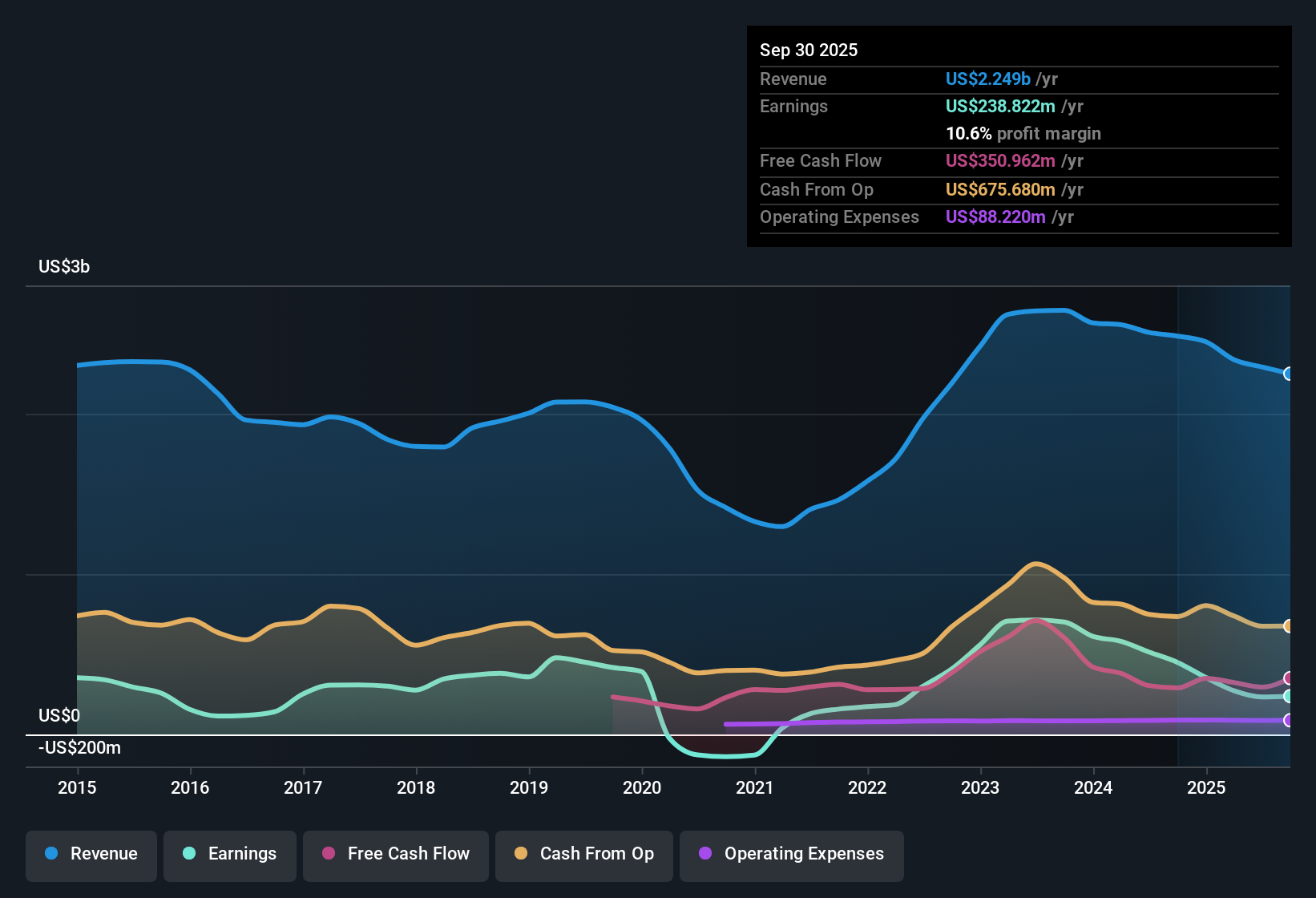

Alliance Resource Partners (ARLP) has wrapped up FY 2025 with fourth quarter revenue of US$535.5 million and basic EPS of US$0.64, alongside net income of US$82.7 million, setting a clear benchmark for the year just finished. Looking back over recent quarters, the partnership has seen quarterly revenue move between US$535.5 million and US$571.4 million in 2025, with EPS ranging from US$0.46 to US$0.73. Trailing twelve month figures show revenue of about US$2.2 billion and EPS of US$2.42. With a trailing net margin of 14.2%, investors will be weighing how consistently ARLP can keep translating its top line into profit in the quarters ahead.

See our full analysis for Alliance Resource Partners.With the numbers on the table, the next step is to set these results against the widely held narratives around ARLP to see which views the data supports and where the story might need updating.

Trailing EPS And Profit Mix Across 2025

- Across FY 2025, quarterly basic EPS moved between US$0.46 and US$0.73 while quarterly net income ranged from US$58.7 million to US$94.2 million, showing that profit shifted within a relatively tight band as revenue stayed between about US$535 million and US$571 million.

- Bulls often point to ARLP’s longer term earnings growth of 16.5% per year and the forecast 7.8% annual earnings growth, and this set of 2025 numbers is consistent with that by showing profitability across the period. At the same time, quarterly swings in EPS, such as US$0.46 in Q2 2025 versus US$0.73 in Q3 2025, also remind you that results can move around within the year.

To see how analysts connect these earnings patterns with ARLP's longer term story, check out the full balanced narrative that ties the numbers together. 📊 Read the full Alliance Resource Partners Consensus Narrative.

14.2% Net Margin And Payout Strain

- On a trailing basis, ARLP’s net margin sits at 14.2%, a touch below the 14.5% margin cited for the prior year, while the trailing dividend yield of 9.72% is flagged as not well covered by earnings.

- Bears highlight the risk that a near 10% yield is hard to maintain if profitability softens, and the small margin step down from 14.5% to 14.2%, alongside trailing twelve month net income of US$311.2 million on about US$2.2b of revenue, gives that concern some grounding even though the company remains clearly profitable.

- Critics point to the gap between earnings and distributions as a key pressure point, and the data here aligns with that view by showing only a slim change in margins while the payout is still marked as weakly covered.

- At the same time, the fact that ARLP is earning over US$300 million in trailing net income shows the issue is about coverage levels rather than an absence of profit, which is an important distinction for income focused holders.

10.2x P/E And 63.8% Gap To DCF

- ARLP is trading on a trailing P/E of 10.2x, below both peers at 20.2x and the US Oil & Gas industry at 13.7x, and its share price of US$24.69 sits about 63.8% under an indicated DCF fair value of US$68.28.

- Supporters argue that this discount, together with five year earnings growth of 16.5% per year and forecast revenue growth of 3.9% per year, supports a view that the market may be underpricing the partnership. However, the below market growth forecasts and the flagged dividend coverage issue show why some investors might still hesitate even with that large model value gap.

- What stands out is the combination of a lower P/E than both peers and industry, and a DCF fair value almost 3x the current price, which is a very large spread for a company that is already profitable.

- In contrast, the slower forecast growth rates compared with the cited broader US market help explain why the discount exists, since not everyone will pay peer level multiples for earnings expected to grow at about 7.8% per year.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Alliance Resource Partners's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

ARLP’s high dividend yield, flagged as not well covered by earnings alongside a modest net margin, raises questions about how reliable that income stream really is.

If you want income that looks better supported, use our these 1818 dividend stocks with yields > 3% to quickly focus on companies offering yields with stronger coverage and potentially fewer payout headaches.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.