Alnylam’s Cardiovascular RNAi Collaboration With Tenaya Might Change The Case For Investing In ALNY

Alnylam Pharmaceuticals, Inc ALNY | 317.67 | -3.84% |

- Earlier this month, Tenaya Therapeutics announced a research collaboration with Alnylam Pharmaceuticals to validate up to 15 gene targets for cardiovascular disease, receiving an upfront US$10 million payment, cost reimbursement over two years, and eligibility for as much as US$1.13 billion in development and commercial milestones.

- The collaboration highlights Alnylam’s effort to extend its RNAi platform into cardiovascular indications while outsourcing early target validation to a specialist partner, potentially broadening its long-term pipeline without absorbing all the upfront scientific risk.

- We’ll now examine how this cardiovascular collaboration with Tenaya could influence Alnylam’s investment narrative and long-term RNAi growth plans.

Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

Alnylam Pharmaceuticals Investment Narrative Recap

To own Alnylam, you need to believe its RNAi platform can keep translating into commercially relevant drugs while the TTR franchise funds that effort. The Tenaya cardiovascular deal usefully seeds optionality in a new area, but it does not materially change the near term focus on AMVUTTRA execution and pricing pressure, or the key risk that high R&D and SG&A spending could outstrip revenue if newer programs underperform.

The Tenaya collaboration also sits alongside Alnylam’s recent push into cardiovascular outcomes with zilebesiran, where the large ZENITH study started enrolling around 11,000 patients in late 2025. Taken together, these moves show how Alnylam is trying to build beyond rare disease into broader cardiometabolic indications, which could become increasingly important if payer pressure intensifies on the existing TTR franchise.

Yet beneath the growth story, investors should also be aware of rising rebate obligations and AMVUTTRA net price pressure that could...

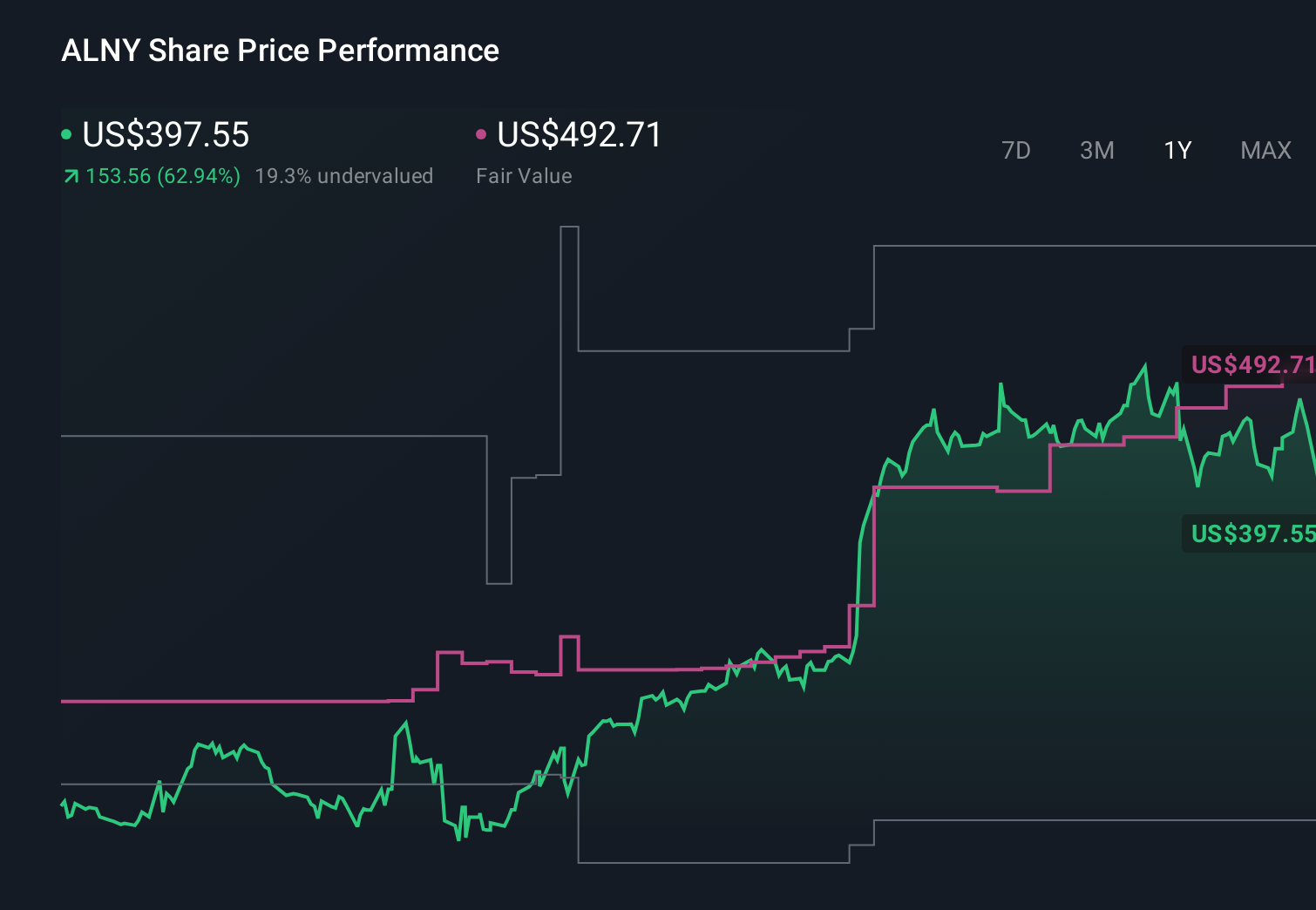

Alnylam Pharmaceuticals' narrative projects $7.0 billion revenue and $1.9 billion earnings by 2028. This requires 41.8% yearly revenue growth and about a $2.2 billion earnings increase from -$319.1 million today.

Uncover how Alnylam Pharmaceuticals' forecasts yield a $491.92 fair value, a 54% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue could reach about US$12.3 billion and earnings US$5.8 billion by 2028, which is far more upbeat than consensus and sits uncomfortably against concerns about sustained TTR concentration risk and pricing pressure; the Tenaya cardiovascular deal may eventually shift either view, so it is worth comparing these very different expectations before you decide how you feel about Alnylam’s path from here.

Explore 5 other fair value estimates on Alnylam Pharmaceuticals - why the stock might be worth just $315.96!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Alnylam Pharmaceuticals research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Alnylam Pharmaceuticals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Alnylam Pharmaceuticals' overall financial health at a glance.

Interested In Other Possibilities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.