Amazon Expands AI Content And Pharmacy Platforms As Valuation Gap Widens

Amazon.com, Inc. AMZN | 209.77 | -0.38% |

- Amazon.com (NasdaqGS:AMZN) is preparing a marketplace that lets publishers license content directly to AI developers.

- The company is also rapidly expanding Amazon Pharmacy same day prescription delivery to nearly 4,500 US cities and towns.

- Both moves point to a bigger push into AI infrastructure and healthcare delivery platforms beyond its core retail and cloud businesses.

Amazon.com, trading at $206.96, sits at the center of two big shifts: AI content access and digital healthcare. The stock shows mixed recent performance, with a 104.6% gain over 3 years but declines of 11.2% over the past week and 16.0% over the past month. That combination means you are looking at a company with a strong multi year track record alongside a period of recent pressure.

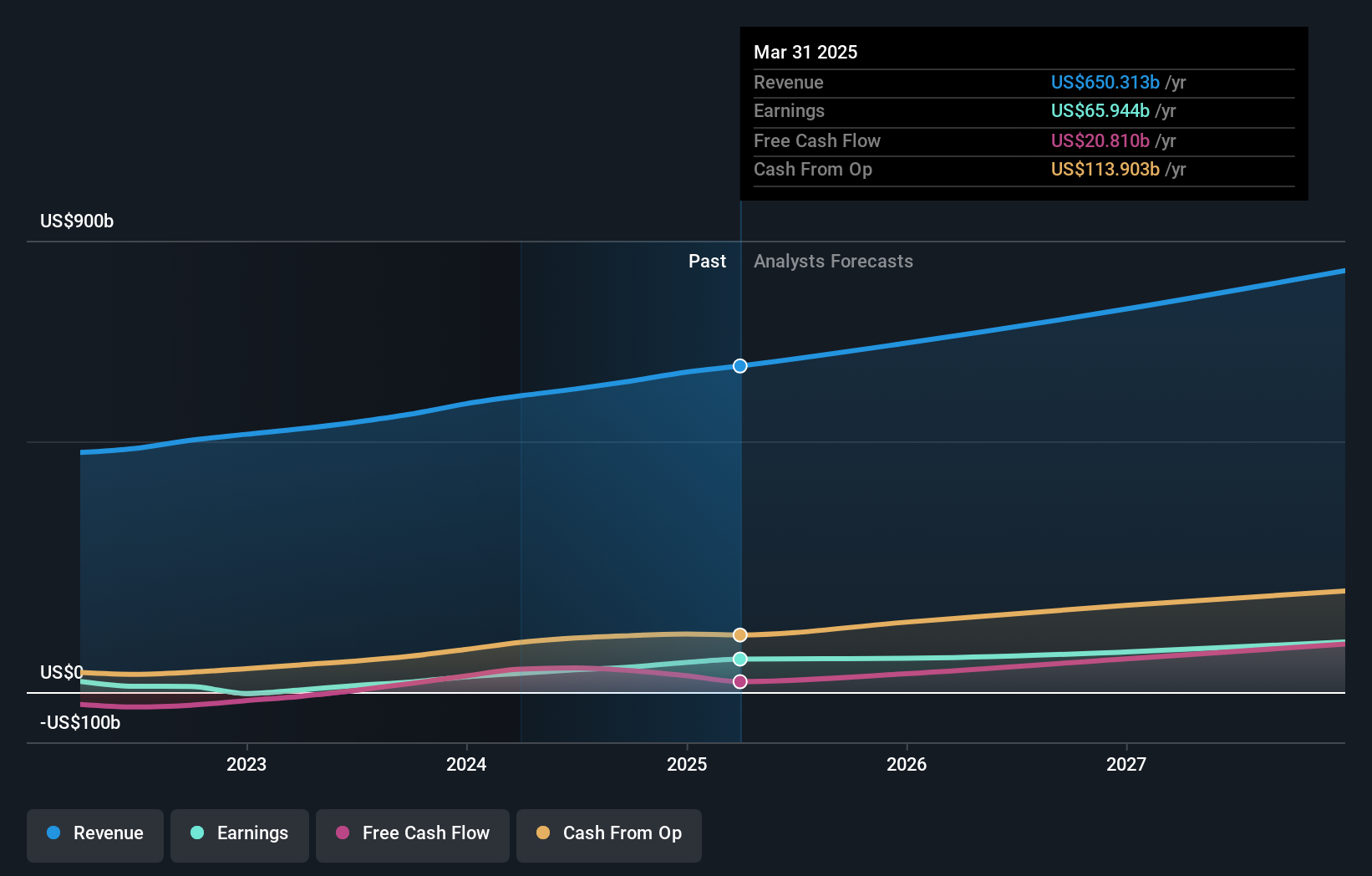

For investors tracking NasdaqGS:AMZN, these moves in AI content licensing and same day pharmacy delivery highlight areas where the business is trying to build new platforms around existing traffic, data and logistics. As details emerge on licensing economics and pharmacy coverage, the focus will likely be on how these efforts affect user engagement, margins and the balance between investment spend and cash generation.

Stay updated on the most important news stories for Amazon.com by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Amazon.com.

Quick Assessment

- ✅ Price vs Analyst Target: At US$206.96, the price sits about 27% below the US$283.49 analyst consensus target.

- ✅ Simply Wall St Valuation: Simply Wall St’s model views Amazon.com as undervalued, trading roughly 40.2% below estimated fair value.

- ❌ Recent Momentum: The 30 day return of 16.0% decline signals short term pressure despite the longer term gains.

There is only one way to know the right time to buy, sell or hold Amazon.com. Head to Simply Wall St's company report for the latest analysis of Amazon.com's Fair Value.

Key Considerations

- 📊 The AI content marketplace and expanded pharmacy delivery both rely on Amazon.com’s existing traffic, logistics and data to widen its platform reach.

- 📊 It may be useful to track how these moves relate to revenue, the net income margin of 10.8%, and whether the 28.6x P/E and 26.7x forward P/E remain in line with market expectations.

- ⚠️ One flagged risk is a high level of non cash earnings, so it can be helpful to monitor the gap between accounting profit and underlying cash generation as these initiatives scale.

Dig Deeper

For a more complete view, including additional risks and potential rewards, explore the complete Amazon.com analysis. You can also visit the community page for Amazon.com to see how other investors interpret this news and its implications for the company's narrative.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.