American Eagle Outfitters (AEO) Could Be 28% Undervalued On CFO Transition News

American Eagle Outfitters, Inc. AEO | 0.00 |

American Eagle Outfitters (AEO) is in focus after announcing a planned change in its finance leadership, with long-serving CFO Mike Mathias shifting to an advisory role and Ravi Thanawala set to assume the CFO position.

American Eagle Outfitters’ recent CFO announcement and equity plan changes come after a mixed stretch, with a 7.13% 30 day share price return and year to date share price return down 34.41%. At the same time, a 1 year total shareholder return of 73.15% and 3 year total shareholder return of 57.12% point to longer term gains that investors will weigh alongside leadership continuity and capital allocation plans.

If this kind of corporate reshaping has you thinking about what else could be on your radar, now is a good time to broaden your search and uncover 20 top founder-led companies

With American Eagle Outfitters shares down 34.41% year to date, yet still showing a 73.15% 1 year total return and trading about 13.7% below the average analyst price target, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 27.6% Undervalued

At a last close of $17.29 versus a narrative fair value of $23.89, American Eagle Outfitters is framed as materially undervalued, with that gap tied to long term earnings and margin assumptions rather than short term trading swings.

The company is optimizing operations by investing strategically in their store fleet and digital platforms to support multi-channel growth, enhance speed, and agility in their supply chain. These efforts are expected to improve net margins through efficiency gains.

Want to see what sits behind that earnings uplift story? The narrative leans on a specific mix of revenue expansion, margin reset, and a future earnings multiple that differs from today. Curious which of those levers does the heavy lifting in the fair value math?

Result: Fair Value of $23.89 (UNDERVALUED)

However, American Eagle Outfitters still faces softer consumer demand and higher markdown risk, which could pressure margins and challenge the earnings and valuation narrative that investors are weighing.

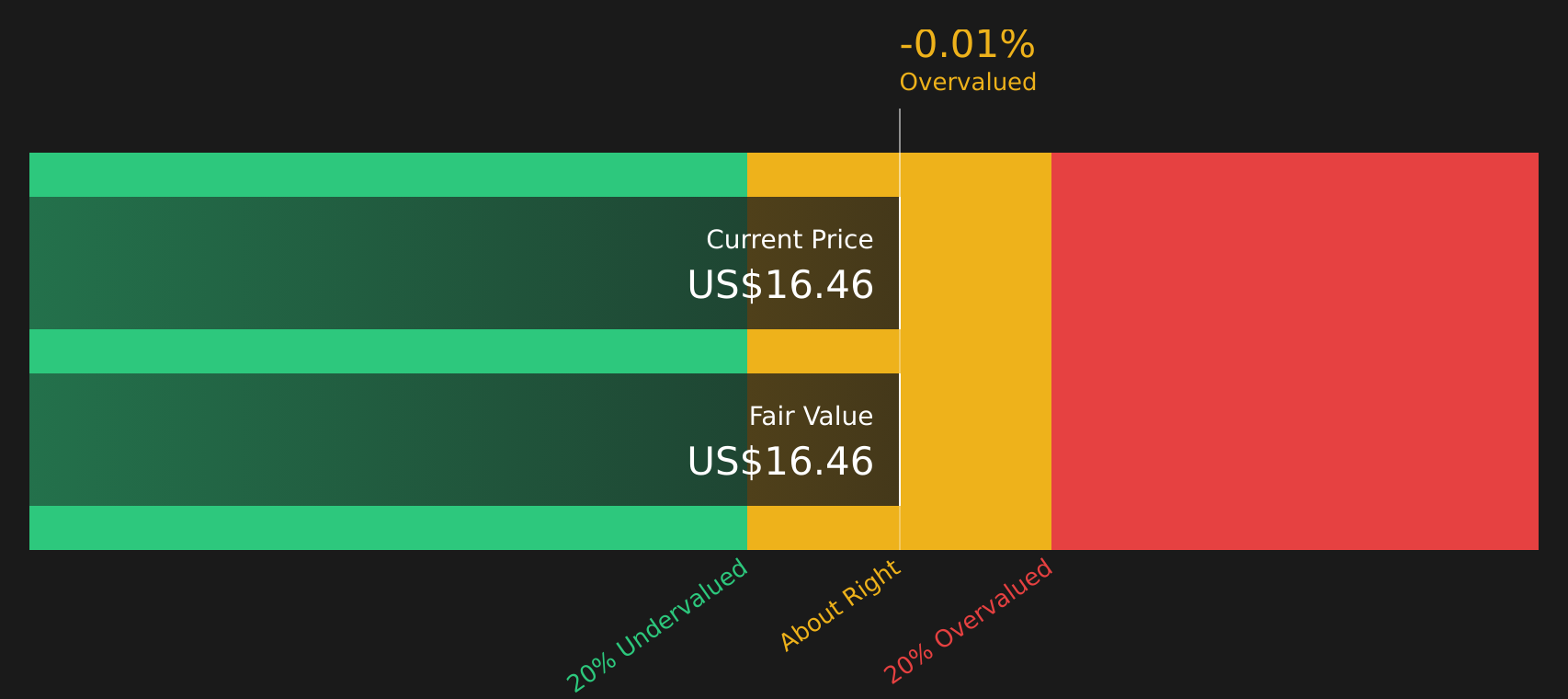

Another View: American Eagle Outfitters Through Cash Flows

While the popular narrative has American Eagle Outfitters looking 27.6% undervalued against a $23.89 fair value, the SWS DCF model points in a different direction. On that measure, AEO at $17.29 sits above an estimated future cash flow value of $16.49, which implies the stock screens as slightly overvalued. For anyone weighing these signals, the key question is which set of assumptions feels closer to how the business will actually perform.

For a closer look at how those assumptions are wired into projected cash flows and discount rates, take a moment to review the full SWS DCF model view on AEO, starting with Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out American Eagle Outfitters for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on value and expectations around American Eagle Outfitters, consider moving quickly and stress testing the full picture yourself using the 4 key rewards and 1 important warning sign

Looking for more investment ideas beyond American Eagle Outfitters?

Once you have formed a view on American Eagle Outfitters, do not stop there. Broaden your watchlist with other stocks that fit clear, disciplined criteria.

- Pressure test your value focus by scanning companies that currently look mispriced relative to their fundamentals through the 41 high quality undervalued stocks.

- Strengthen your income stream by hunting for companies offering robust yields using the 8 dividend fortresses.

- Prioritise resilience by filtering for companies with healthier balance sheets and stronger foundations through the solid balance sheet and fundamentals stocks screener (47 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.