American International Group (AIG) Could Be 8% Undervalued Following Executive Appointments

American International Group, Inc. AIG | 0.00 |

American International Group (AIG) has drawn fresh attention after appointing Christine Williams as Head of Global Client and Broker Relationships and Nancy Bewlay as Executive Vice President, Global Chief Underwriting Officer, both joining from major insurance peers.

Alongside the leadership changes, American International Group’s recent share price performance has been mixed. The share price is down 5.52% year to date, despite a 7.45% 1 month share price return and a 92.22% 5 year total shareholder return. This suggests that long term momentum contrasts with shorter term volatility and shifting risk perceptions following recent index reclassifications.

If you are comparing AIG’s profile with other opportunities in the market, it can help to widen the lens beyond large insurers and review 19 top founder-led companies

American International Group appears to be a solid insurance business with rising revenue and net income. However, after the recent index reshuffle and leadership changes, investors may question whether the stock still offers sensible value at around $79.62 a share.

Most Popular Narrative: 7.9% Undervalued

On the latest numbers, the most followed narrative sees American International Group’s fair value at $86.45, compared with the recent $79.62 share price. This frames a modest valuation gap driven by execution on underwriting and capital deployment.

The acceleration of digitalization and artificial intelligence initiatives, such as the Gen AI deployment across underwriting and claims, positions AIG to improve operational efficiency and risk selection while also enabling better pricing segmentation and product customization. In turn, this is expected to support improved margins, a more resilient earnings profile, and a more competitive offering in high growth and specialty lines over time.

Curious what underpins that fair value for American International Group. The narrative leans heavily on compounding revenue, expanding margins, and a future earnings multiple that assumes disciplined execution without stretching expectations.

Result: Fair Value of $86.45 (UNDERVALUED)

However, this American International Group narrative still hinges on key uncertainties, including climate related catastrophe losses and sector wide legal pressures that could weigh on underwriting results.

Another View on American International Group’s Valuation

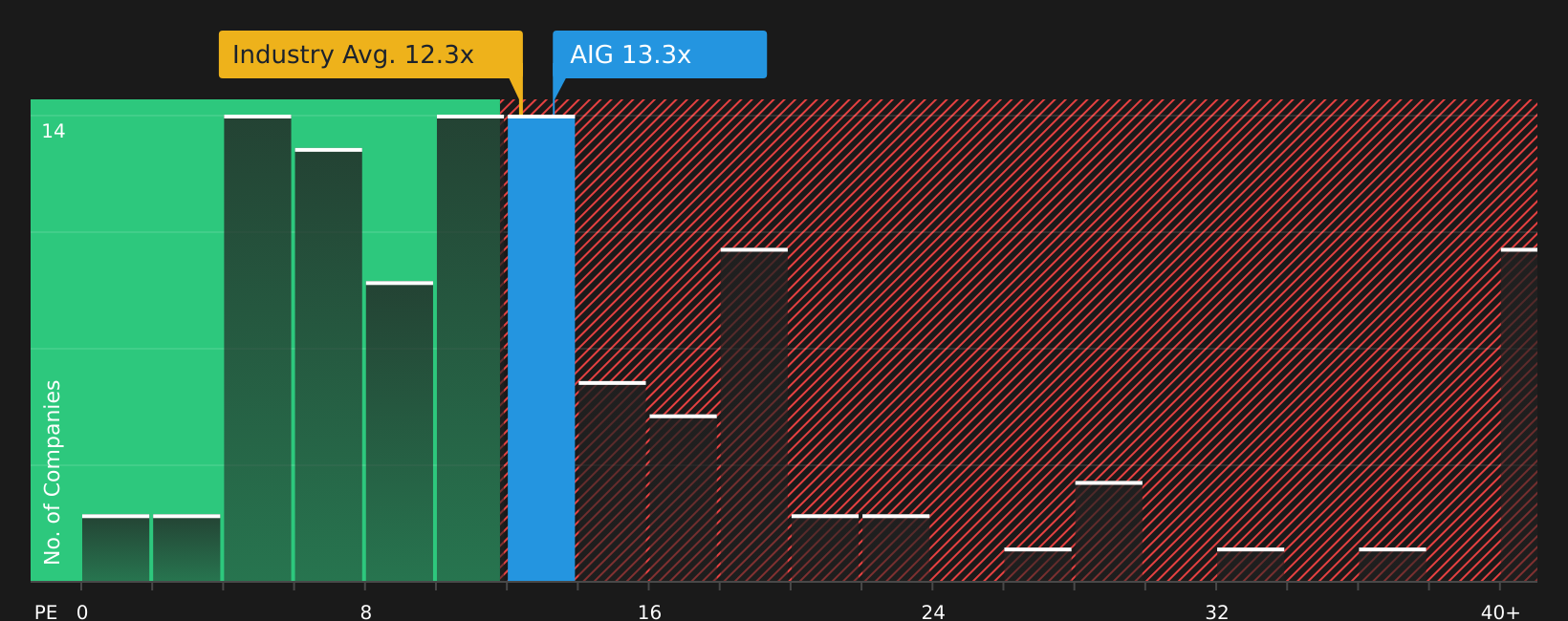

While the fair value narrative for American International Group points to around 7.9% undervaluation, the current P/E ratio of 13.4x tells a different story. It sits above both the US Insurance industry average of 12.3x and peer average of 10.9x, as well as a fair ratio of 12.7x, which implies some valuation stretch. That gap can signal less room for error if earnings or sentiment soften, so how comfortable are you paying a premium multiple for this earnings profile?

Next Steps

If this mix of optimism and caution around American International Group leaves you unsure, take a closer look at the data and stress test your own thesis. Then weigh those findings against the 3 key rewards

Looking for more investment ideas beyond American International Group?

If American International Group has sharpened your focus on quality, do not stop here. Use the Simply Wall St Screener to quickly surface fresh, data backed stock ideas.

- Target potential upside in companies that combine quality fundamentals with attractive pricing by reviewing the 44 high quality undervalued stocks.

- Prioritize resilience and capital protection by checking the 72 resilient stocks with low risk scores that filters for stocks with stronger risk profiles.

- Spot opportunities the crowd might be missing by using the screener containing 19 high quality undiscovered gems that highlights lesser known companies with solid metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.