American Tower (AMT) Stock Looks Below Fair Value After 30% Slide

American Tower Corporation AMT | 0.00 |

American Tower stock has declined about 30.2% over the past five years, yet the latest valuation work suggests the shares may now be trading at a meaningful discount to intrinsic value. With the Discounted Cash Flow (DCF) estimate and market based checks pointing in the same direction, the question for investors is whether recent weakness has already priced in the concerns.

- Over the past five years, American Tower is down roughly 30.2%, which sets a cautious backdrop for any claim that the stock now looks cheap.

- Analyst focus on data center and AI related demand can support revenue expectations, while any disappointment in that growth or execution around new infrastructure projects may weigh heavily on what investors are willing to pay.

- On Simply Wall St's broader valuation checks, American Tower screens as undervalued in 6 of 6 areas, which points to a stock that currently leans cheap rather than expensive.

The issue now is whether that apparent discount to intrinsic value gives American Tower enough margin of safety to interest investors who have watched the share price weaken in recent years.

Does American Tower Look Undervalued on Cash Flow?

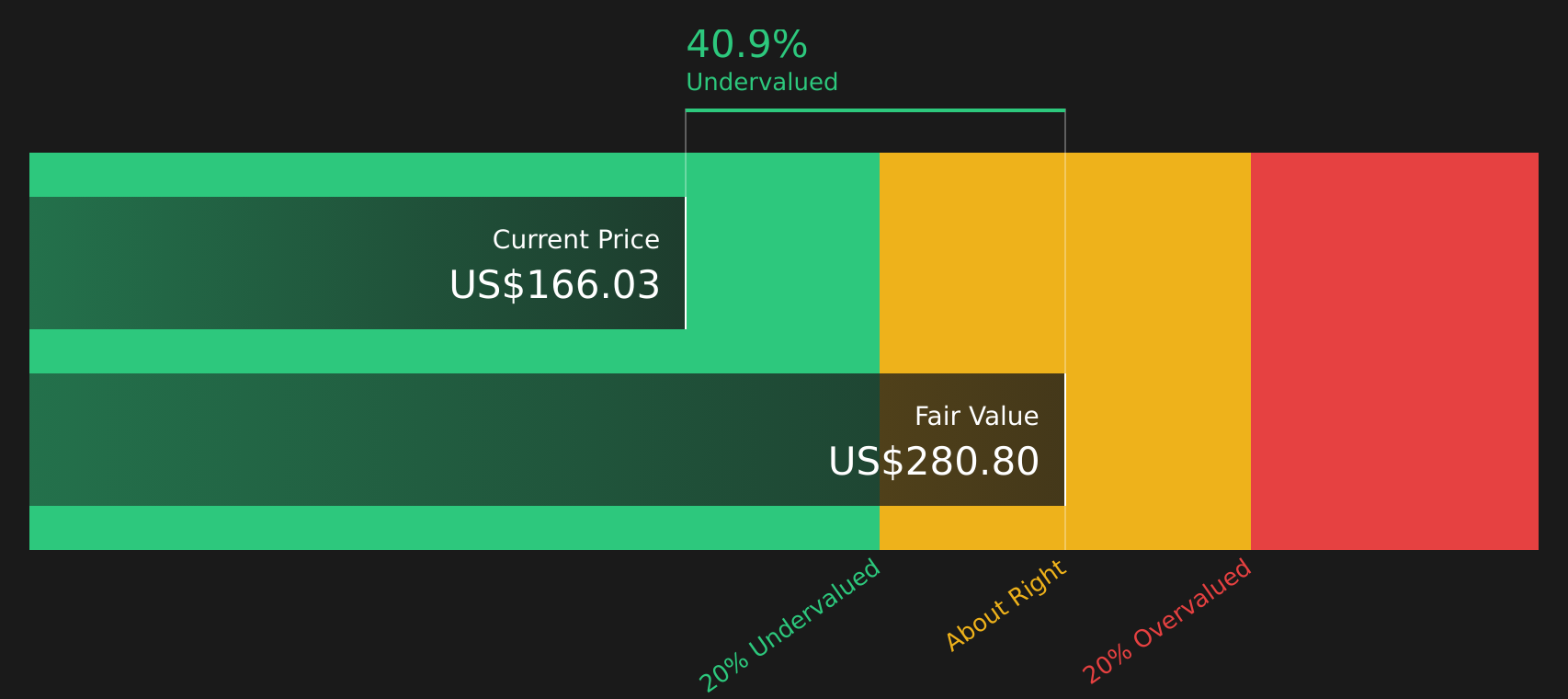

The Discounted Cash Flow (DCF) model here is built on American Tower’s adjusted funds from operations and long range cash flow projections. On this basis, the latest twelve month free cash flow of about $5.0b is treated as growing over time, then discounted back to today to estimate what those future dollars could be worth in the present.

That approach produces an intrinsic value estimate of about $279 per share, which sits well above the current share price and, on this basis, indicates that American Tower is trading at roughly a 40.5% discount to that cash flow based value. Because the recent RBC Capital Markets upgrade focuses on data center and AI related demand, the DCF result indicates that the market price may still be giving limited credit for the projected cash generation tied to those themes.

Taken together, the cash flow assumptions and DCF outcome indicate that, on this basis, American Tower stock currently appears undervalued.

Our Discounted Cash Flow (DCF) analysis suggests American Tower is undervalued by 40.5%. Track this in your watchlist or portfolio, or discover 41 more high quality undervalued stocks.

Is American Tower Still Cheap on Earnings?

The P/E ratio is a useful cross check for American Tower because earnings are a key anchor for how investors value mature real estate investment trusts. American Tower currently trades on a P/E of about 26.7x, which is higher than the Specialized REITs industry average of roughly 16.2x, but below a peer group average around 32.9x.

On Simply Wall St's fair P/E estimate of about 35.3x, which reflects the company’s mix of growth prospects, margins, size and risk profile, American Tower’s current multiple implies a discount to where this framework suggests it could trade. The gap between the fair ratio and the actual 26.7x indicates that the stock screens as undervalued on earnings, even after accounting for its premium to the broader REIT sector.

Putting this together, American Tower stock appears undervalued on its P/E multiple relative to the fair ratio implied by its fundamentals.

The American Tower Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for American Tower pick up where the valuation work leaves off by explaining which paths for American Tower's growth, margins and earnings would need to occur for the stock to be worth materially more or less than it trades for today on the market. Each narrative treats fair value as a thesis about how the business might develop over time, so you can see how that thesis holds up as new information arrives, and they are available on Simply Wall St's Community page.

If you have a number driven view on whether American Tower's data center diversification and AI related demand ultimately support today's valuation, add your Narrative to the Simply Wall St community and spell out the case in your own terms.

It is a chance to set out your thesis on American Tower now and then see how that call holds up over time as new results and analyst updates come through.

Do you think there's more to the story for American Tower? Head over to our Community to see what others are saying!

The Bottom Line

For investors looking at American Tower today, both the Discounted Cash Flow (DCF) intrinsic value estimate and the earnings multiple work point in the same direction, with the stock screening as undervalued on each framework. The key debate is whether the cash flows tied to data center and AI related demand ultimately materialise in line with expectations, and whether the current P/E can hold or improve if that story stumbles. The crux from here is whether the present discount reflects an opportunity, or whether the market is correctly building in execution and growth risks around American Tower's expansion plans.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.