Ametek (AME) Stock Valuation Check After Recent Momentum And Mixed Fair Value Signals

AMETEK, Inc. AME | 0.00 |

Why AMETEK (AME) is on investors’ radar today

AMETEK (AME) is drawing fresh attention after its recent trading session, with the stock closing at US$230.45. That price reflects the market’s current view of a company generating US$7.60b in revenue and US$1.53b in net income.

The current share price sits on the back of a 6.9% 90 day share price return and a 10.2% year to date share price return. The 1 year total shareholder return of 29.8% points to momentum that extends beyond short term moves.

If you are looking for other opportunities in industrial and automation themes, it may be worth scanning the 33 robotics and automation stocks.

With AMETEK trading around US$230 and carrying an intrinsic value estimate at a premium to that level, the key question is whether the recent 1 year, 3 year, and 5 year returns leave much upside, or if the market is already pricing in future growth.

Most Popular Narrative: 11.1% Undervalued

With AMETEK trading at $230.45 against a narrative fair value of $259.16, the current setup reflects a modest implied upside based on analyst forecasts and cash flow assumptions using a 9.58% discount rate.

EMG and Automation segments are inflecting upwards, with destocking now complete and record orders translating to accelerating organic growth and strong core margin expansion. This shift is poised to further enhance operating leverage and group EBITDA growth in coming quarters.

Want to see what is sitting behind that margin story and revenue outlook? The narrative leans on measured growth, steady profitability and a richer earnings multiple. Curious how those moving parts line up to reach that fair value figure.

Result: Fair Value of $259.16 (UNDERVALUED)

However, this upside narrative can be challenged if weakness lingers in semiconductor and research exposed segments, or if acquisition heavy growth fails to deliver expected returns.

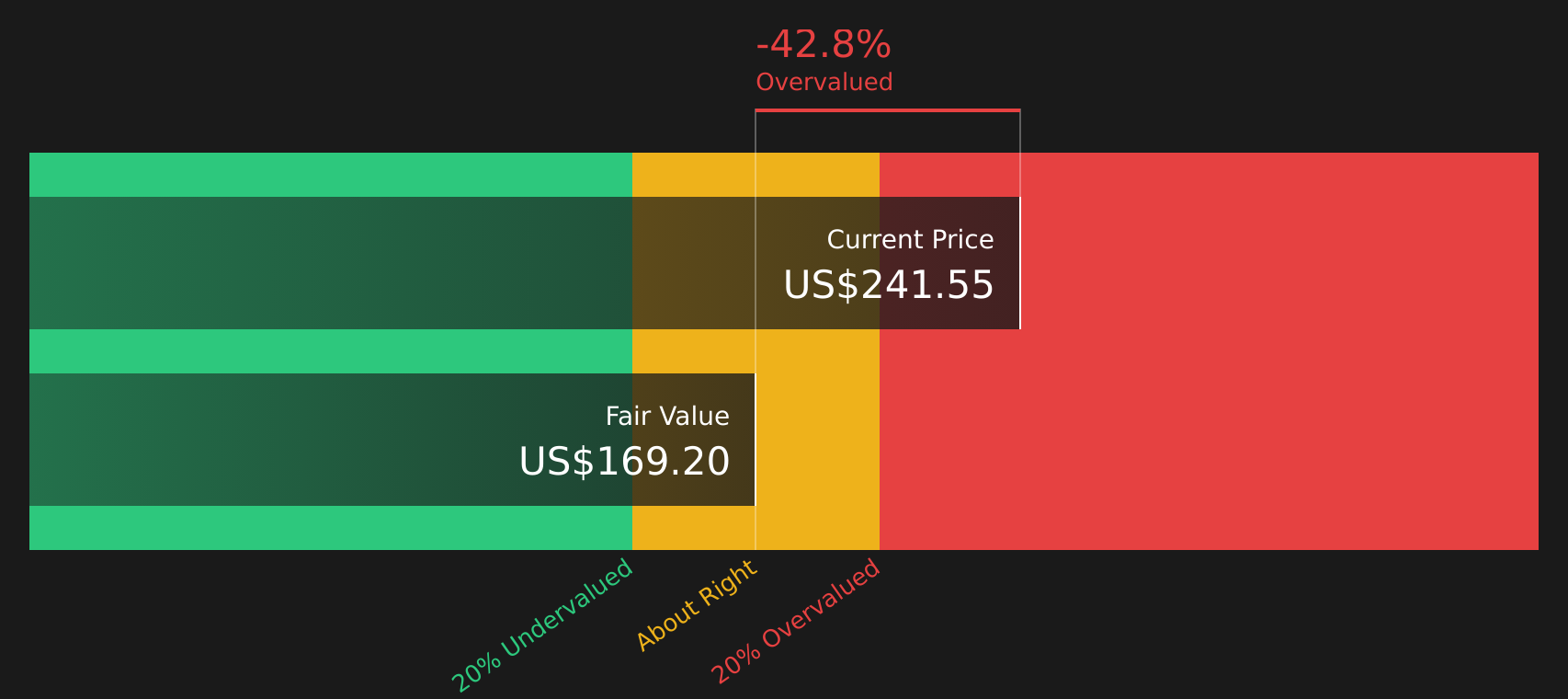

Another View: Cash Flows Point To A Richer Price

While the narrative fair value of US$259.16 suggests upside, the SWS DCF model paints a different picture. On that cash flow view, AMETEK’s estimated value sits around US$160.75, which would put the current US$230.45 share price well above that level and raise questions about how much optimism is already in the stock.

For anyone weighing these two signals side by side, it can be useful to see how the cash flow assumptions stack up against the narrative and analyst targets, and what would need to change for the DCF view to move closer to today’s price. Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out AMETEK for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment mixed between upside potential and a full valuation, it makes sense to move quickly, review the numbers yourself, and shape your own stance by checking the 3 key rewards.

Looking for more investment ideas?

If AMETEK has your attention, do not stop here. Some of the most useful opportunities show up when you compare this stock against others with strong fundamentals.

- Start by scanning companies that combine quality with attractive prices using the 47 high quality undervalued stocks.

- Focus on resilience and sleep easier at night by checking the 68 resilient stocks with low risk scores.

- Hunt for lesser known opportunities with solid metrics through the screener containing 20 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.