An Early Sneak Peek At Wall Street's 2028 Outlook

Let's take a break from what's happening now or what could happen the rest of this year and consider where things could be farther out.

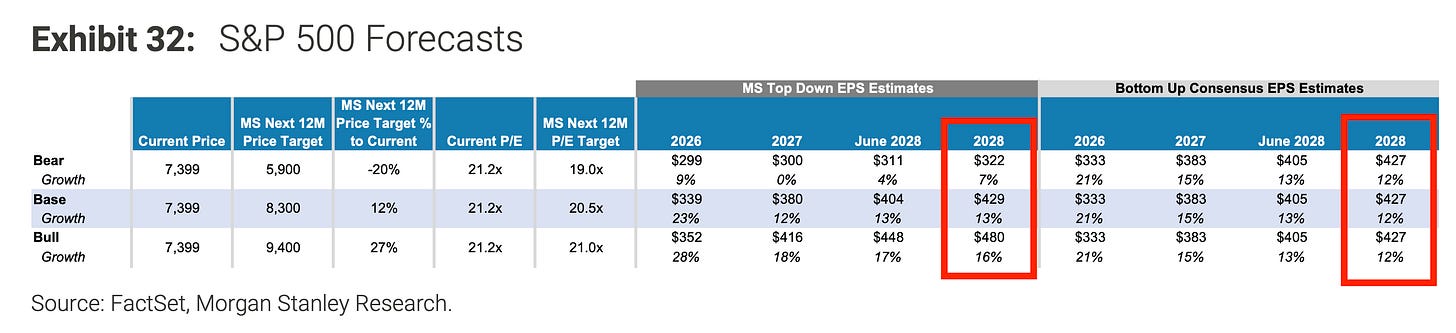

In his mid-year outlook note published earlier this month, Morgan Stanley's Mike Wilson offered a glimpse of what he's expecting in 2028.

"We see 2026 EPS of $339 (23% growth), 2027 EPS of $380 (12% growth), and 2028 EPS of $429 (13% growth)," Wilson wrote (emphasis added).

This is encouraging for investors because earnings are the most important long-term driver of stock prices.

Wilson's 2028 estimate isn't too far from the consensus, which calls for earnings to grow 12% year over year to $427 per share.

"Positive operating leverage, AI adoption/'run it lean,' improving pricing power, and an AI capex cycle that continues to show momentum are key drivers of our constructive view on earnings," Wilson said.

Admittedly, no one can be expected to nail what'll happen two to three years from now.

But it's worth giving it a shot, especially since so much of a stock's value comes from what the underlying company is expected to earn in the years ahead.

To his credit, Wilson has long been right about the positive operating leverage theme. Three years ago, he predicted that operating leverage — or the degree to which costs move with sales — would help drive profit margin expansion in the years to come. Indeed, profit margins have continued to trend higher through the years.

The AI adoption story is relatively new, but it's gaining traction.

Companies continue to prove they have pricing power as they have been making their customers help pay for inflation over the years.

And then there's the AI capex story. The megacap tech hyperscalers continue to commit massive amounts of cash toward building out the AI hardware infrastructure. Barclays analysts expect hyperscaler capex to peak at $1 trillion in 2028 before leveling off.

There's no guarantee that these will be the leading earnings narratives two years from now. Nevertheless, it's positive that we have tangible narratives that could realistically be the driving forces of earnings growth.

Decelerating somewhat 🐢

While earnings may continue to grow, the pace of growth isn't expected to remain as hot.

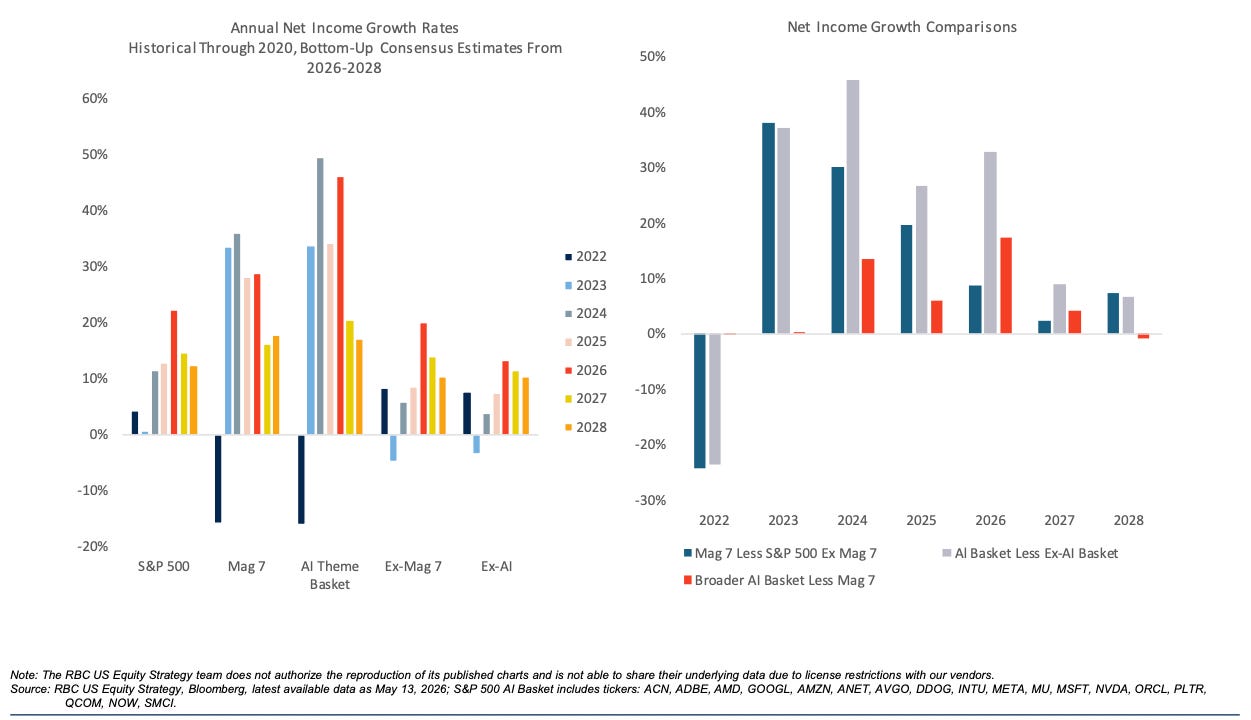

"S&P 500 net income is expected by consensus to peak in 2026, then decelerate in 2027 and 2028," RBC's Lori Calvasina wrote earlier this month. "The Mag 7 appears to have peaked in 2024, with deceleration expected through 2027 and some reacceleration anticipated in 2028. Meanwhile, a broader AI basket is anticipated to see far superior growth in 2026 to both the broader index and Mag 7, followed by deceleration in 2027 and 2028."

For those who've been nervous about growth being a little hot, these forecasts for decelerating growth might come as a relief.

But don't confuse decelerating growth with slow growth.

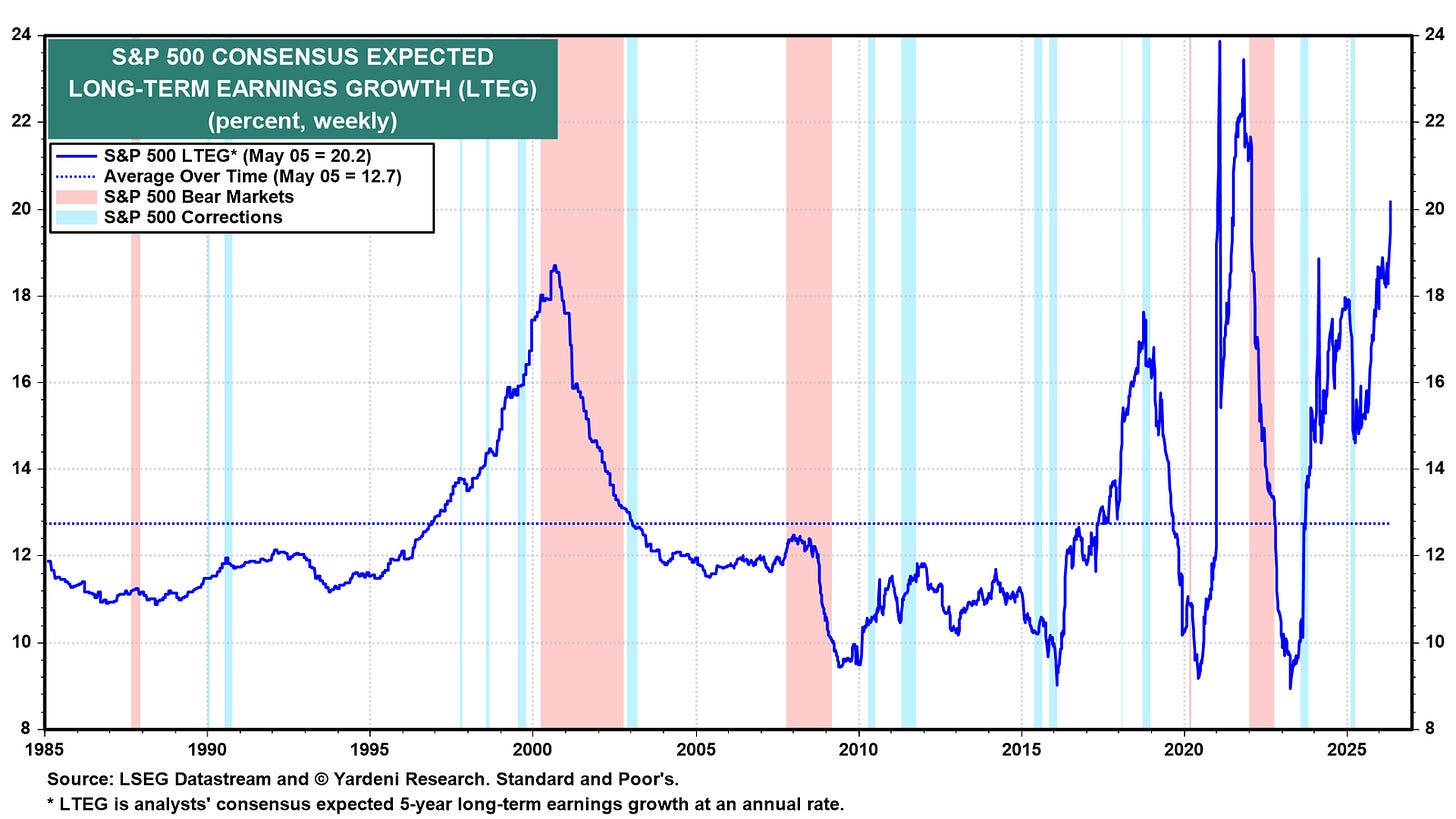

Ed Yardeni, founder of Yardeni Research, considered how the current five-year earnings growth estimate compares to historical levels.

"The analysts may be starting to get ‘Buzzed,' as their expected long-term earnings growth (LTEG) for the S&P 500 rose to 20.2% during the week of May 5," Yardeni observed. "It rose even higher during the pandemic, when fiscal and monetary policymakers both were slamming on the accelerator. But LTEG now exceeds the 18.6% peak of the 2000 tech bubble."

So even assuming deceleration in growth, the expected earnings growth rate remains very strong.

The big picture 🖼️

A lot of things could go wrong between now and 2028. And if we've learned anything over the past few years, unexpected things happen.

While we don't know for sure what the next couple of years will look like, we can at least be certain that the publicly traded companies in the stock market will do whatever they can to generate earnings growth.

Time and time again, Corporate America has proven it can adapt and evolve when challenged in its relentless pursuit of profits.

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.