Analyst Downgrade Amid Biofuels Competition Might Change The Case For Investing In Green Plains (GPRE)

Green Plains Inc. GPRE | 15.68 | +2.95% |

- Recently, investment analysts downgraded Green Plains from Buy to Hold, citing increased competition in the biofuels sector and uncertainty around future regulations despite the company’s ongoing diversification into renewable fuels and higher-value products.

- What stands out is that skepticism is growing even as Green Plains invests in expanding low-carbon fuel operations, highlighting how sensitive its outlook remains to policy and industry conditions.

- We’ll now explore how this fresh analyst caution around competition and regulation could reshape Green Plains’ existing investment narrative.

Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

Green Plains Investment Narrative Recap

To own Green Plains, you have to believe that low carbon fuels, carbon credits and higher value coproducts can eventually offset today’s unprofitable core ethanol business. The recent downgrade to Hold speaks directly to that belief, since it amplifies near term concerns around competition and regulation, which already sit at the heart of the key catalyst of policy support and the biggest risk of policy or execution setbacks. I see this caution as directionally consistent, not a material reset.

The most relevant recent announcement here is Green Plains’ 2025 results, where the company remained loss making with a full year net loss of US$121.28 million despite stronger Q4 profitability. This backdrop matters because the investment case leans heavily on future monetization of tax credits and carbon projects, so any external skepticism around policy durability or industry competition lands on a business that has yet to convert its transformation into consistent earnings.

Yet beneath the policy tailwinds, you should be aware of how exposed Green Plains still is if government support for carbon credits were to...

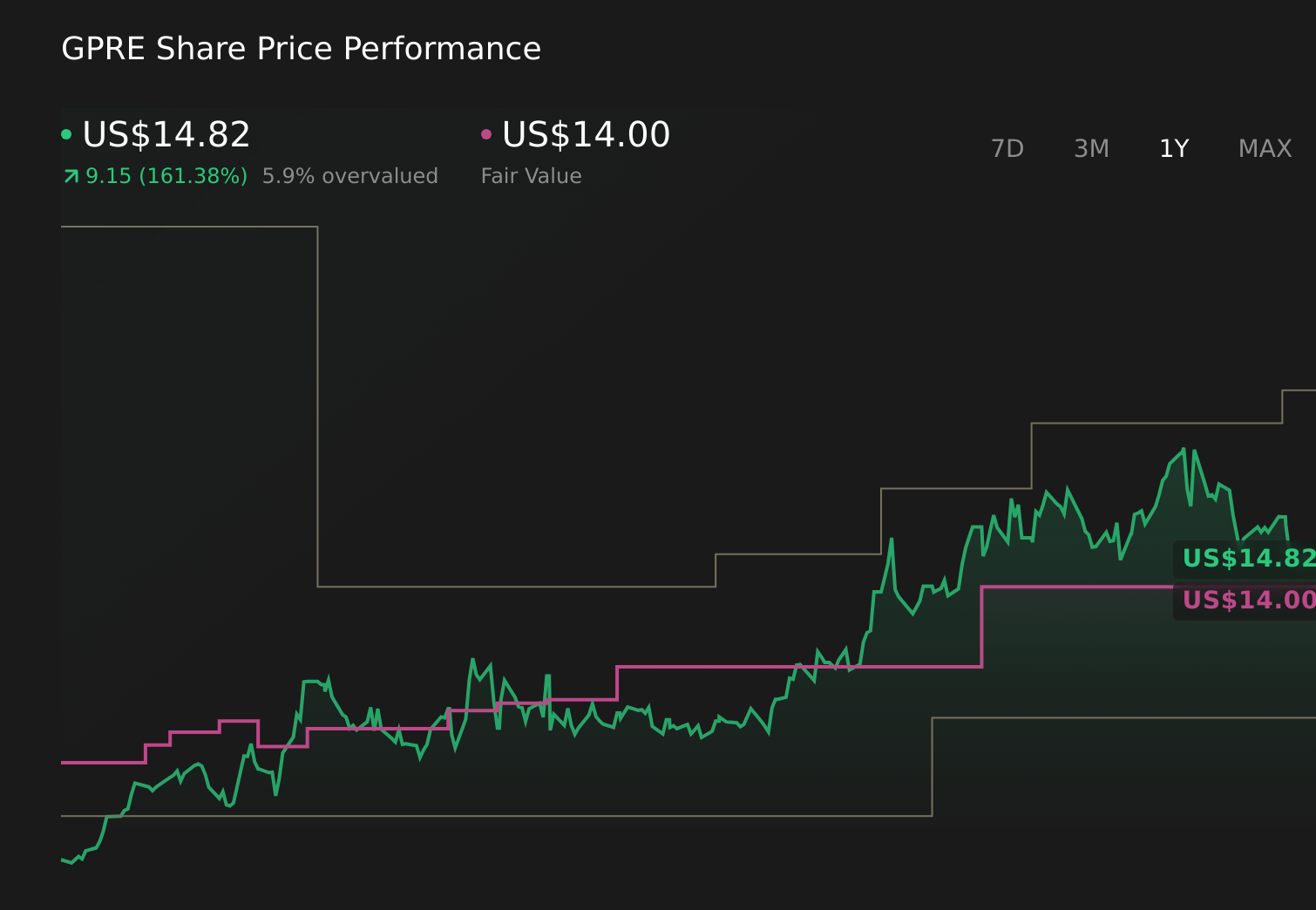

Green Plains’ narrative projects $3.4 billion revenue and $116.3 million earnings by 2028.

Uncover how Green Plains' forecasts yield a $14.00 fair value, a 17% downside to its current price.

Exploring Other Perspectives

Contrast this with the lowest analysts, who already worry that heavy capital spending could disappoint, even as they model revenue hitting about US$3.7 billion and earnings near US$171 million by 2029. These more pessimistic views might shift again after the downgrade, so it helps to look at several scenarios before you decide what story you believe.

Explore 3 other fair value estimates on Green Plains - why the stock might be worth 17% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Green Plains research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Green Plains research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Green Plains' overall financial health at a glance.

Searching For A Fresh Perspective?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.