Apollo Global Management (APO) Following A Pullback And Rich Valuation Questions

Apollo Global Management Inc APO | 0.00 |

Recent Returns Put Apollo Global Management in Focus

Apollo Global Management (APO) has drawn investor attention after its stock declined around 6% over the past month, despite a gain of roughly 12% over the past 3 months and a 3 year total return above 600%.

This performance sits alongside a reported revenue figure of US$31,287 million and net income of US$1,155 million. This combination is prompting closer scrutiny of how the company’s diversified asset management and retirement services operations may be influencing sentiment.

Over the past year, Apollo Global Management’s share price has fallen year to date and over the last week, while its 3 year and 5 year total shareholder returns remain strongly positive. This suggests that recent momentum has cooled after a longer period of gains.

If you are weighing Apollo Global Management against other opportunities, this could be a useful moment to broaden your watchlist with 20 top founder-led companies

So with Apollo Global Management’s share price down year to date but its multi year returns still very strong and the stock trading below some analyst targets, is this a genuine buying opportunity, or is the market already pricing in future growth?

Preferred Price-to-Earnings Multiple: Is it justified?

Apollo Global Management currently trades on a P/E of 60.7x, and that sits against the last close price of $121.51 and a discount to the average analyst price target of 23.8%.

The P/E multiple compares the company’s share price to its earnings per share, so a higher P/E usually means the market is paying more today for each dollar of current earnings. For an asset manager like Apollo Global Management, that often reflects expectations around future fee income, performance fees and profitability across its asset management, principal investing and retirement services segments.

Here, the 60.7x P/E is significantly higher than both the peer average of 31.9x and the US Diversified Financial industry average of 15x. This indicates the stock is priced well above sector norms. It is also above an estimated fair P/E of 24.6x. The market could move towards this level if pricing starts to align more closely with that fair ratio estimate.

Result: Price-to-Earnings of 60.7x (OVERVALUED)

However, Apollo Global Management’s revenue declined sharply on an annual basis, and the stock is down year to date, which could signal pressure on its current valuation.

Another View on Apollo Global Management’s Valuation

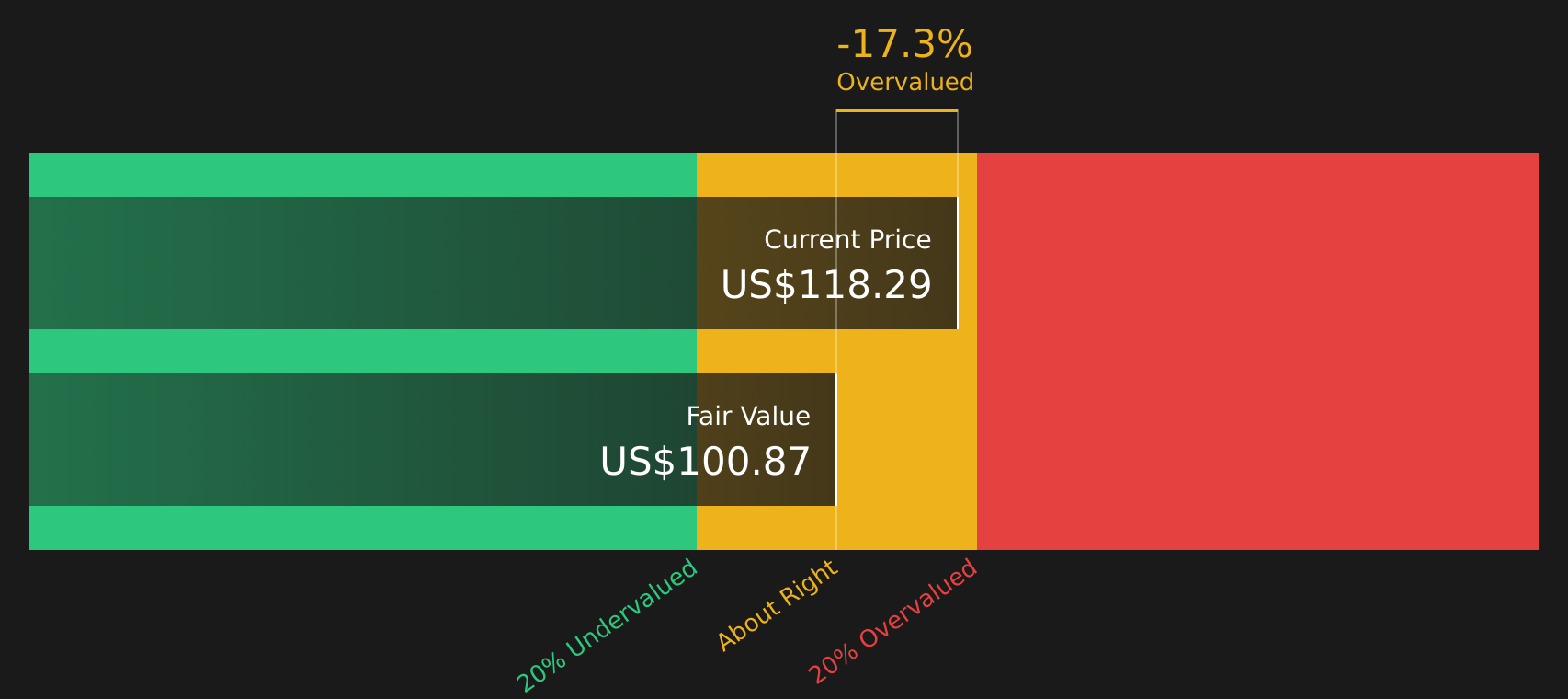

While the P/E of 60.7x suggests Apollo Global Management is priced well above peers and the estimated fair ratio of 24.6x, our DCF model also points to a rich valuation, with the stock around $121.51 versus an estimated value of about $101. That raises a simple question: how much upside is left if expectations slip?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Apollo Global Management for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 43 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of caution and optimism around Apollo Global Management feels hard to balance, consider reviewing the data directly and weighing both sides, starting with its 2 key rewards and 3 important warning signs

Looking for more investment ideas beyond Apollo Global Management?

If Apollo Global Management has you thinking more broadly about your portfolio, this can be a useful time to widen your search and stress test your next moves.

- Target resilience by scanning companies with robust finances using the solid balance sheet and fundamentals stocks screener (48 results).

- Hunt for mispriced opportunities by reviewing the 43 high quality undervalued stocks.

- Strengthen your income stream by assessing stocks in the 9 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.