Applied Materials (AMAT) Valuation in Focus After UBS Upgrade on AI-Driven DRAM and Data Center Growth

Applied Materials, Inc. AMAT | 353.80 | +3.51% |

Applied Materials (AMAT) stock gained momentum after UBS upgraded its outlook, citing an expected increase in DRAM spending driven by growth in AI and data centers. The company’s expanded R&D efforts and advanced chip technology position it well for future demand.

Applied Materials has notched an impressive run, with momentum building after fresh highs in AI and semiconductor demand. The 12.6% seven-day share price return and a striking 56.9% gain over the past three months show investor optimism is growing. The 45.8% total shareholder return for the last year confirms broad-based rewards for longer-term holders.

If you’re interested in finding the next standout in the tech and AI world, now’s a great time to explore See the full list for free.

But after such an impressive run, is Applied Materials still trading at an attractive valuation, or has the market already priced in the next wave of growth, leaving investors little room for upside?

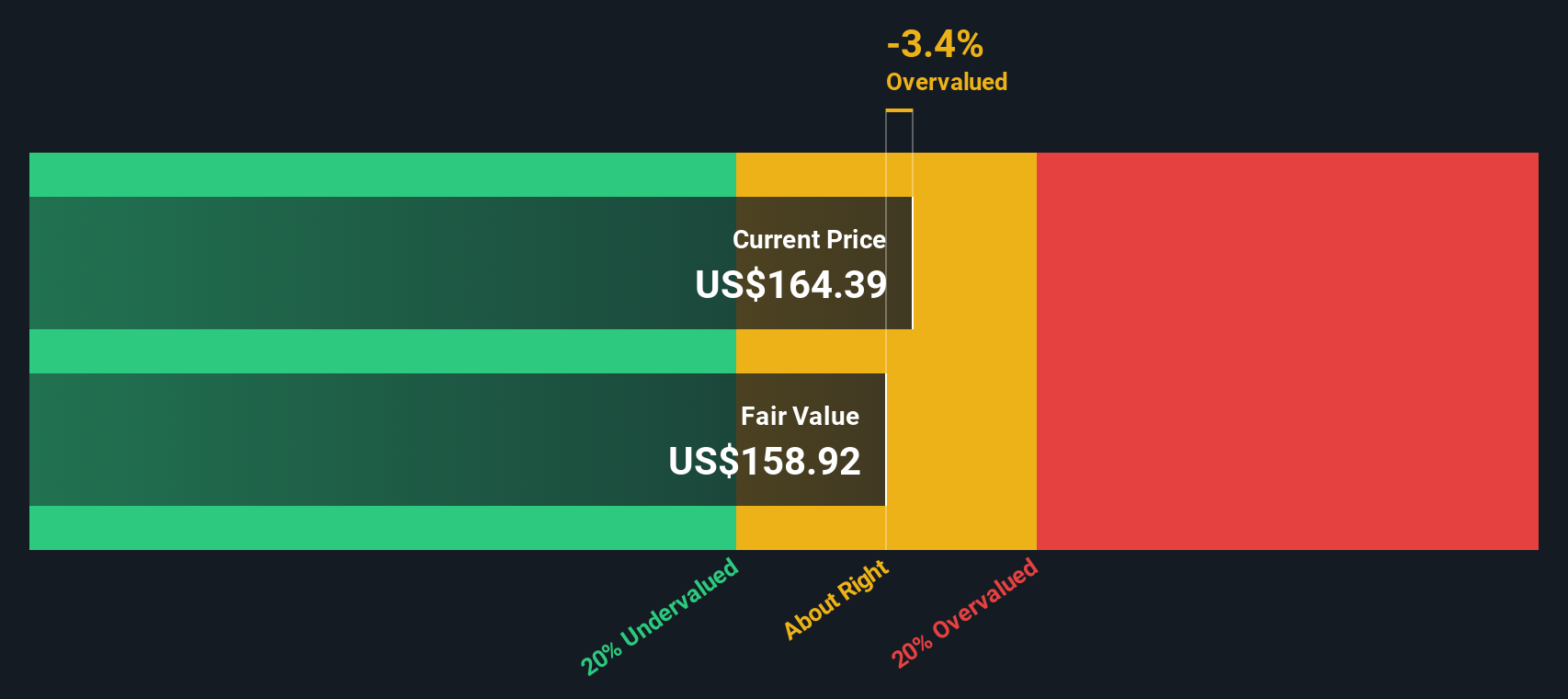

Most Popular Narrative: 4% Overvalued

The prevailing narrative places Applied Materials’ fair value just below the current price, with a small but noticeable premium. This sets the scene for a closer look at the factors driving analyst outlooks and future expectations.

The ongoing explosion in data creation and rapid adoption of digital transformation (IoT, automotive, industrial automation) continue to accelerate wafer fab buildouts globally, with Governments incentivizing regional manufacturing. Applied's broad portfolio and investments in local manufacturing infrastructure (for example, new Arizona and EPIC centers) position it to capture a greater share of this growing and more geographically diverse capital expenditure, supporting both revenue growth and margin resilience.

Curious what bold assumptions underpin this tightly priced stock? Hidden in the narrative are forward-looking profit margins and crucial revenue upgrades. Unlock the financial logic that could justify or challenge Applied Materials’ premium valuation.

Result: Fair Value of $241.69 (OVERVALUED)

However, there are real risks, including heightened competition from China and ongoing geopolitical uncertainty, that could quickly shift Applied Materials’ outlook.

Another View: Comparing Value Against the Market

While narrative-driven models suggest Applied Materials trades at a premium, our DCF model paints a starker picture. It estimates fair value closer to $158.08, which is well below today's share price. This challenges the idea that recent growth and optimism are fully justified by future cash flows. Could the risk now be on the downside?

Build Your Own Applied Materials Narrative

If you think the story here doesn't quite fit your view, or if you'd rather dig into the details and chart your own course, you can easily craft your own narrative in just a few minutes. Do it your way

A great starting point for your Applied Materials research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Don’t let opportunity pass you by. Savvy investors are already uncovering compelling stocks with the potential for serious upside. Let Simply Wall Street’s powerful screeners guide your next move.

- Supercharge your portfolio with these 25 AI penny stocks that are powering breakthroughs in artificial intelligence and reshaping entire industries.

- Take advantage of potential hidden gems by targeting these 921 undervalued stocks based on cash flows favored for their attractive prices based on robust cash flows.

- Cement steady returns by checking out these 15 dividend stocks with yields > 3% that consistently pay healthy yields over 3%, rewarding patient investors with reliable income.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.