Aptiv (APTV) Expands Kyndryl Tie Up, Is The Stock Still Undervalued?

Aptiv PLC APTV | 0.00 |

Kyndryl’s new collaboration with Aptiv (APTV) highlights how the company is using its Wind River software portfolio to support mission-critical systems and edge AI in complex customer environments.

Despite the Kyndryl alliance spotlighting Aptiv’s software capabilities, the stock has faced selling pressure, with the 30-day share price return down 14.68% and the year-to-date share price return down 25.98%, while the 1-year total shareholder return is down 1.10%. This suggests near term momentum has softened compared with the longer record.

If this kind of edge AI story has your attention, it can be useful to scan other robotics and automation plays through the 33 robotics and automation stocks

Aptiv’s shares have already absorbed a sharp reset, yet the Kyndryl tie-up puts fresh attention on its software ambitions. Is more of the valuation upside still in front of investors, or has the recent slide simply caught up with the story?

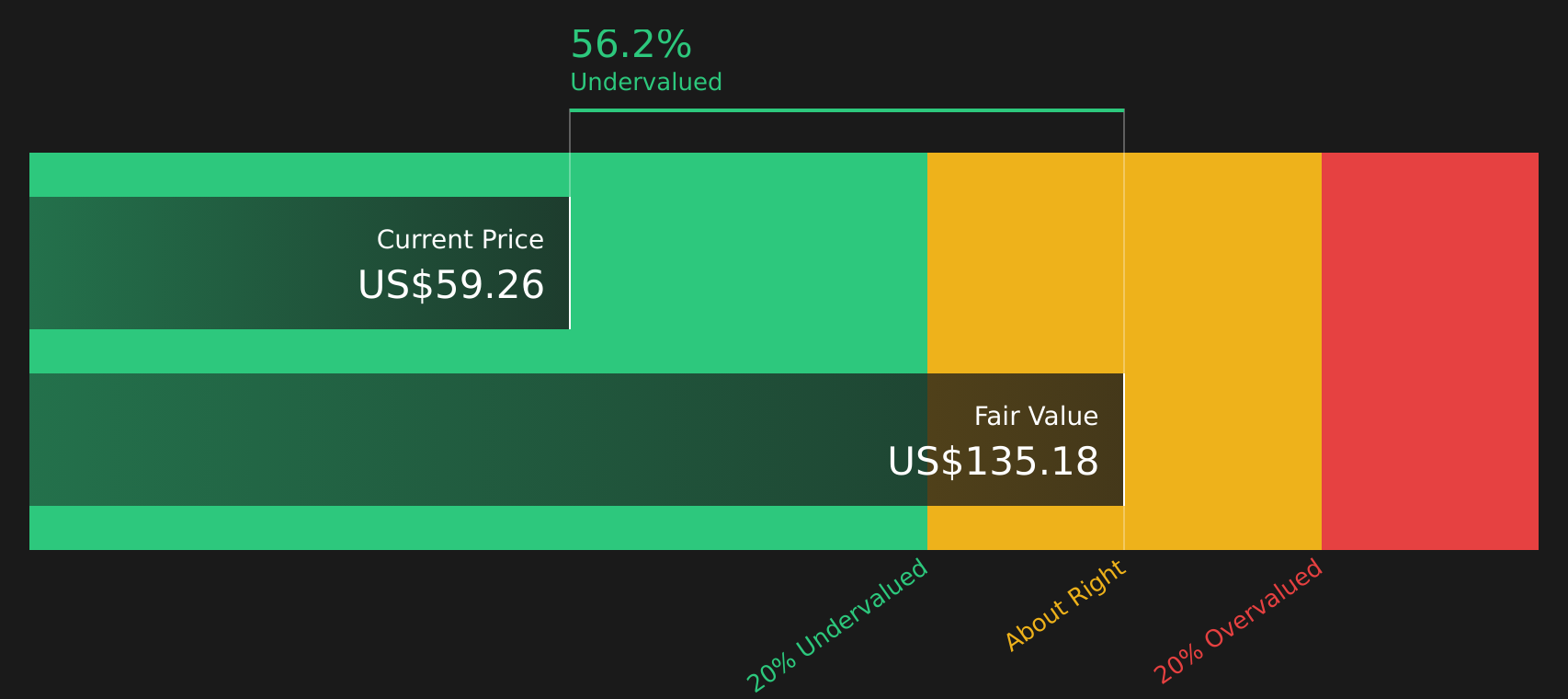

Most Popular Narrative: 26% Undervalued

Aptiv’s most followed narrative anchors on a fair value of $78.21 versus a last close of $58.06, framing the Kyndryl collaboration within a wider valuation reset and a software heavy future.

Strong demand for Aptiv's advanced electrical/electronic architectures (including high-voltage and high-speed data connectivity products), driven by the global shift toward electric vehicles and increasingly complex vehicle electrical systems, is supporting robust new business bookings and growth in content per vehicle. This is a positive catalyst for revenue growth and, as volume scales, for operating leverage and margins.

Read the complete narrative. Read the complete narrative.

Want to see how this EV wiring and ADAS thesis translates into future earnings, margins, and valuation multiples for Aptiv, including the assumptions behind that fair value number?

According to this widely followed view, the story behind Aptiv is less about recent share price weakness and more about how high margin software, ADAS platforms, and non auto exposure could reshape its earnings mix over time. The same narrative also bakes in lower revenue, a sharply higher profit margin, and a future valuation multiple that differs from where the broader auto components group sits today, all discounted at 9.82% to reach that $78.21 figure.

Result: Fair Value of $78.21 (UNDERVALUED)

However, Aptiv’s narrative could be tested if auto production slows further in key regions, or if competition in ADAS and edge AI crimps pricing power.

Another View on Aptiv’s Valuation

The first narrative leans on a discounted cash flow approach that suggests Aptiv is trading well below an estimate of its future cash flow value of $135.93 per share, so the SWS DCF model points to an undervalued stock. But what if those long range cash flow and margin assumptions prove too optimistic?

Next Steps

If this mix of pressure and potential around Aptiv has you thinking, take a closer look at the underlying data today and weigh both sides of the story with the 3 key rewards and 3 important warning signs

Looking for more investment ideas beyond Aptiv?

If Aptiv has sharpened your thinking, do not stop here. Broaden your watchlist with other stocks that line up with your risk appetite and return goals.

- Target potential mispricing by scanning companies that screen as quality plus value through the 44 high quality undervalued stocks.

- Strengthen your focus on balance sheets by zeroing in on companies highlighted in the solid balance sheet and fundamentals stocks screener (48 results).

- Hunt for under the radar opportunities with the screener containing 20 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.