ArcBest (ARCB) Valuation Check As ArcBest View Digital Logistics Platform Rolls Out

ArcBest ARCB | 0.00 |

Why ArcBest View matters for ArcBest (ARCB) shareholders

ArcBest (ARCB) has launched ArcBest View, a digital logistics platform that centralizes shipment visibility, booking, management, and reporting. This gives investors a fresh operational development to consider when assessing the stock.

The launch of ArcBest View comes as momentum builds in the stock, with a 1-month share price return of 8.64%, a 90-day share price return of 30.73%, and a 1-year total shareholder return of 120.32% from a last close of US$136.69.

If this kind of logistics driven story has your attention, it may also be worth scanning for other transport related opportunities through Simply Wall St's 20 top founder-led companies

With ArcBest View now in the spotlight, the key question is whether ArcBest at US$136.69 and an estimated 35% intrinsic discount still offers genuine value or if the market is already pricing in future growth.

Most Popular Narrative: 40.3% Overvalued

Against the Simply Wall St narrative fair value of $97.42, ArcBest's last close at $136.69 reflects a clear premium, which that narrative links to a detailed set of earnings, margin, and multiple assumptions.

Broad deployment of AI-driven optimization tools, such as real-time route and dock management systems, are driving measurable productivity gains and cost savings, which are expected to translate into improved net margins and operational earnings as automation and technology adoption intensify across the industry.

Curious how a logistics platform, modest revenue growth, and shifting margins can still support a higher long term earnings profile and richer multiple assumptions? The narrative hinges on how technology and asset light services reshape cash generation and justify that gap between fair value and current price.

Result: Fair Value of $97.42 (OVERVALUED)

However, softer freight demand and ongoing rate pressure across both Asset-Based and Asset-Light operations could still undercut the margin and earnings profile that supports this richer valuation.

Another View: Cash Flows Point in a Different Direction

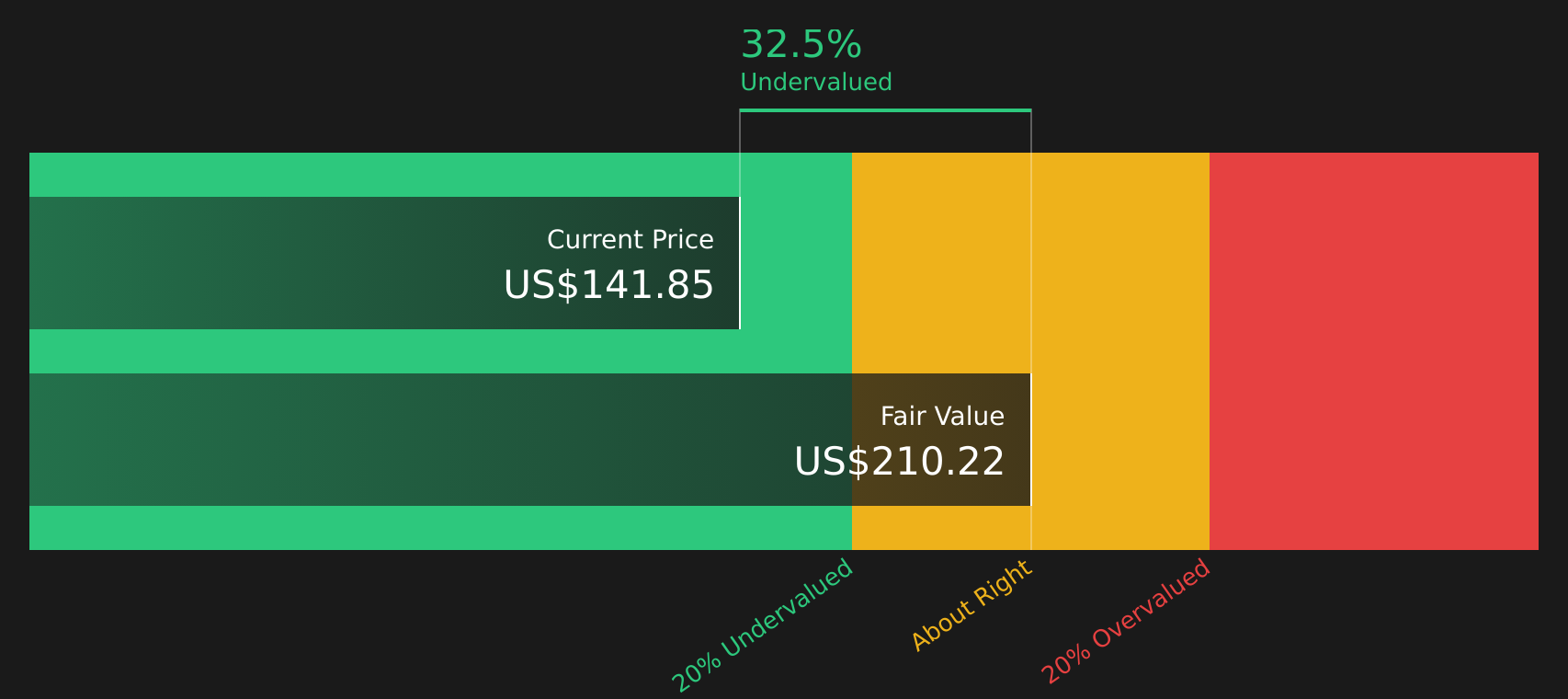

While the narrative based fair value of $97.42 frames ArcBest as 40.3% overvalued, the SWS DCF model tells a very different story. On that measure, ArcBest at $136.69 sits below an estimated future cash flow value of $209.69, which points to potential upside instead of downside risk. For you, the tension is simple: do earnings based assumptions or cash flow based assumptions feel more reliable here?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ArcBest for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the balance between upside potential and valuation risk feels delicate, it helps to move quickly, review the underlying numbers, and decide where you stand. To consider both sides in one place, take a look at the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If ArcBest has you thinking harder about where to put your money next, casting a wider net with focused stock ideas can help sharpen your watchlist.

- Spot potential value opportunities early by reviewing 46 high quality undervalued stocks that combine quality fundamentals with appealing pricing signals.

- Prioritize resilience by scanning 64 resilient stocks with low risk scores that score well on financial strength and downside protection.

- Get ahead of the crowd by checking a screener containing 22 high quality undiscovered gems before they attract wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.