Archer Daniels Midland (ADM) Valuation Check After Insider Buying And Mixed Earnings Results

Archer-Daniels-Midland Company ADM | 68.68 68.68 | +2.58% 0.00% Post |

Archer-Daniels-Midland (ADM) is back in focus after director David R. McAtee II bought 7,500 shares shortly after the company reported adjusted fourth quarter EPS above consensus but fell short on revenue with mixed segment results.

Despite softer earnings for 2025, investors have pushed Archer-Daniels-Midland’s share price up, with a 30 day share price return of 7.6% and a 1 year total shareholder return of 56.66%. This shows renewed momentum supported by dividend growth and recent joint venture news.

If ADM’s recent move has you thinking about other opportunities in essential resources, it could be a good moment to scan our 21 elite gold producer stocks as a starting point for further ideas.

With ADM now trading near its 52-week high after a tough earnings year, but with ongoing dividend increases and insider buying, should you view this as undervalued resilience, or has the market already fully reflected future growth in the share price?

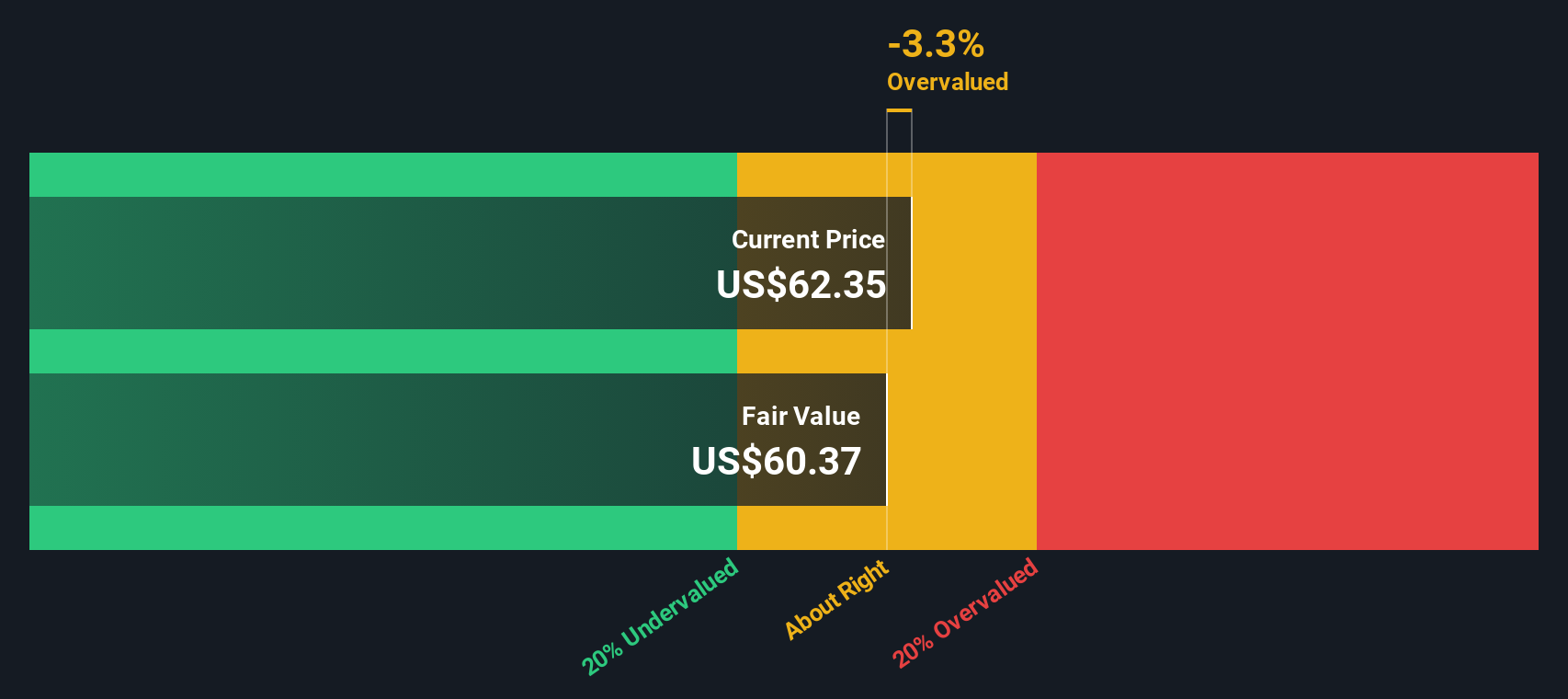

Most Popular Narrative: 16.6% Overvalued

Archer-Daniels-Midland’s most followed narrative places fair value at about $59.64, compared with the last close of $69.51, which frames the current optimism in a different light.

Policy clarity and ongoing government support for biofuels, including the extension of the 45Z tax credit, favorable RVOs, and domestic feedstock incentives, are expected to drive increased soybean oil demand and improved crush margins, directly supporting ADM's revenue and net margins from late 2025 into 2026.

Read the complete narrative. Read the complete narrative.

Curious what kind of revenue lift, margin rebuild, and future earnings multiple are built into that fair value line? The full narrative spells out those assumptions in detail.

Result: Fair Value of $59.64 (OVERVALUED)

However, this narrative could be knocked off course if biofuel policies remain uncertain or if margins and volumes weaken further in core commodity processing segments.

Another View: Cash Flows Point to Undervaluation

While one common view is that Archer-Daniels-Midland is about 16.6% overvalued at a fair value of $59.64, our DCF model suggests a different picture. It indicates an estimate of future cash flow value of $83.09, which places the current $69.51 share price at a 16.3% discount. Which perspective do you think reflects the business more accurately?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Archer-Daniels-Midland for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Archer-Daniels-Midland Narrative

If you see the story differently or prefer to work from the raw numbers yourself, you can build a custom view in just a few minutes. Do it your way

A great starting point for your Archer-Daniels-Midland research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If ADM has sharpened your interest, do not stop here. The next smart move is lining up a few more candidates that fit your style.

- Target strong value potential by scanning companies trading on appealing metrics with our 53 high quality undervalued stocks, then compare how they stack up against ADM in your watchlist.

- Prioritize resilience and capital preservation by checking out 85 resilient stocks with low risk scores, so you are not missing companies that might better match your comfort with volatility.

- Spot lesser known opportunities early by running through our screener containing 23 high quality undiscovered gems, before others start paying attention to the same names.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.