Are OFG Bancorp's (OFG) Margin Pressures Quietly Rewriting Its Valuation Story?

OFG Bancorp OFG | 0.00 |

- OFG Bancorp has already reported its second-quarter 2026 results, followed by a conference call and webcast that provided management’s latest commentary and financial disclosures.

- At the same time, analysts are highlighting ongoing pressure on net interest income and margin compression, even as the bank trades at a relatively low forward price-to-book ratio versus peers.

- Now, we’ll examine how concerns over muted net interest income growth and margin pressure could reshape OFG Bancorp’s investment narrative.

AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

OFG Bancorp Investment Narrative Recap

To own OFG Bancorp, you need to be comfortable with a Puerto Rico focused bank where the core story rests on loan growth, digital adoption, and disciplined capital return. The latest commentary on muted net interest income and ongoing margin compression speaks directly to the main near term catalyst and risk: how effectively OFG can protect profitability while competing for loans and deposits. If margins stabilize, the near term impact of this news may be limited; if not, it could pressure earnings.

Against this backdrop, the recently announced US$200,000,000 share repurchase authorization and ongoing buybacks stand out, particularly with OFG trading on a relatively low forward price to book multiple versus peers. For investors, this capital return program interacts directly with the margin debate: if earnings growth slows under continued net interest income pressure, the sustainability and effectiveness of repurchases in supporting per share metrics become more important to watch.

Yet while capital returns draw attention, investors should also be aware of how persistent competition could affect OFG's funding costs and...

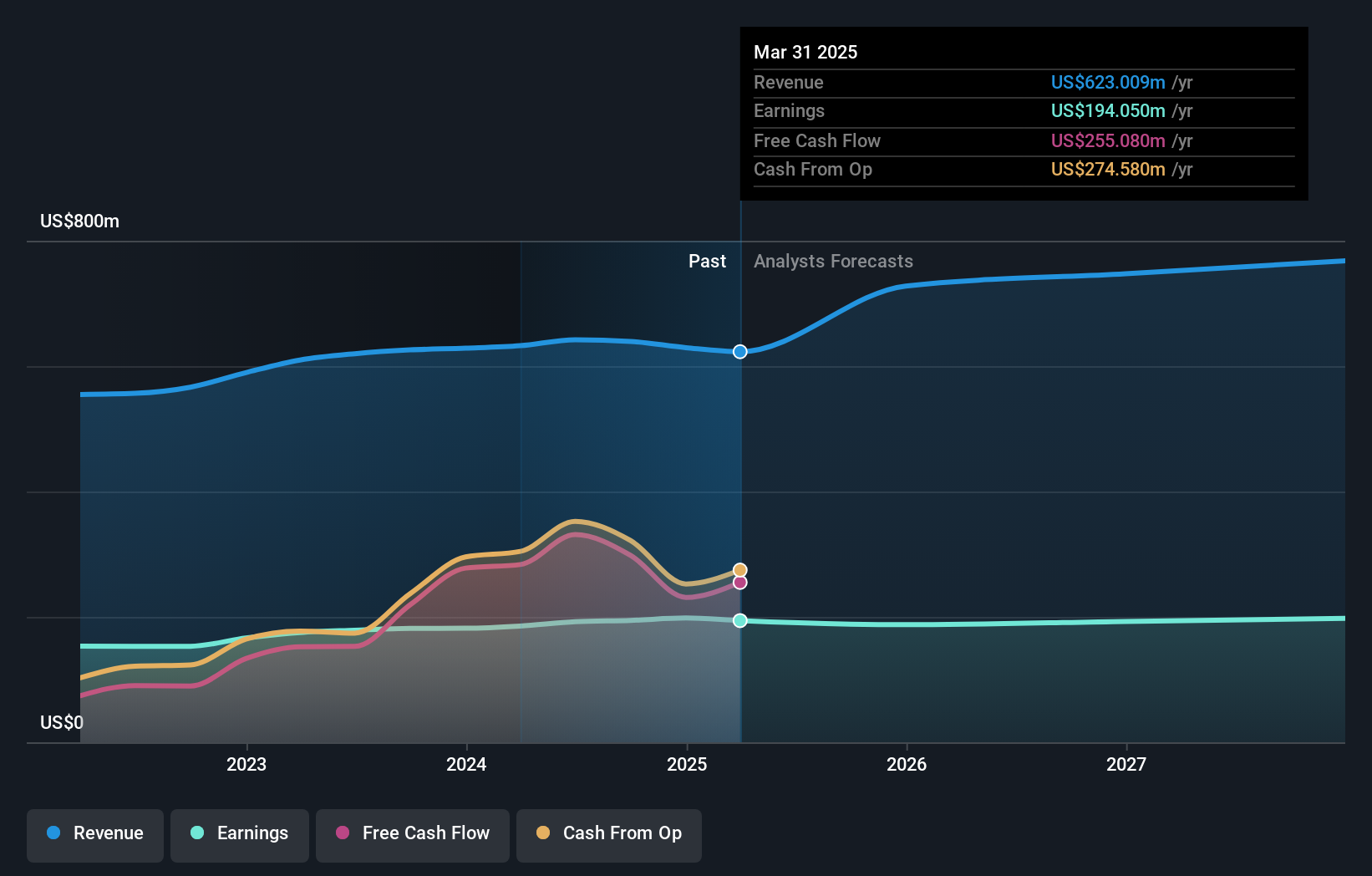

OFG Bancorp's narrative projects $780.4 million revenue and $177.9 million earnings by 2029. This requires 7.1% yearly revenue growth and a $35.6 million earnings decrease from $213.5 million.

Uncover how OFG Bancorp's forecasts yield a $47.75 fair value, a 3% downside to its current price.

Exploring Other Perspectives

Simply Wall St Community members currently place OFG Bancorp’s fair value between US$47.75 and about US$108.38, based on just 2 individual assessments. Against that wide spread, concerns about ongoing margin pressure and muted net interest income growth highlight why you may want to compare several of these viewpoints before forming expectations about the bank’s performance.

Explore 2 other fair value estimates on OFG Bancorp - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your OFG Bancorp research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free OFG Bancorp research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate OFG Bancorp's overall financial health at a glance.

Searching For A Fresh Perspective?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Uncover the next big thing with 22 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.