Are Rising Earnings Estimates Reframing Bandwidth's (BAND) AI Platform From Story Stock To Profit Engine?

Bandwidth Inc. Class A BAND | 0.00 |

- Earlier this year, Bandwidth reported that analysts had increased their full-year earnings estimates and the company received an improved Zacks Rank of #2 (Buy), signaling stronger expectations for its near-term financial performance.

- This shift in analyst sentiment suggests growing confidence in Bandwidth’s ability to convert its AI-enabled communications platform and enterprise customer focus into improved profitability.

- Against this backdrop of upgraded earnings forecasts, we’ll examine how strengthening analyst expectations may influence Bandwidth’s existing investment narrative today.

AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Bandwidth Investment Narrative Recap

To own Bandwidth today, you need to believe its AI-enabled communications platform and enterprise focus can translate into durable, profitable growth despite a volatile share price and an evolving CPaaS market. The recent jump in full-year earnings estimates and Zacks Rank upgrade reinforces the near term profitability catalyst, but it does not remove key risks around customer concentration and potential pricing pressure if communications services continue to commoditize.

The most directly relevant update to this improving analyst sentiment is Bandwidth’s April 2026 decision to raise full year revenue guidance to US$880 million to US$900 million after Q1 results. That guidance lift sits alongside stronger earnings estimates and may be amplifying expectations that Bandwidth can scale its AI focused Maestro platform with better operating leverage, while still leaving open questions around how much investment will be required to sustain innovation and global expansion.

Yet beneath the optimism, investors should be aware that concentration among large enterprise customers could become a real problem if...

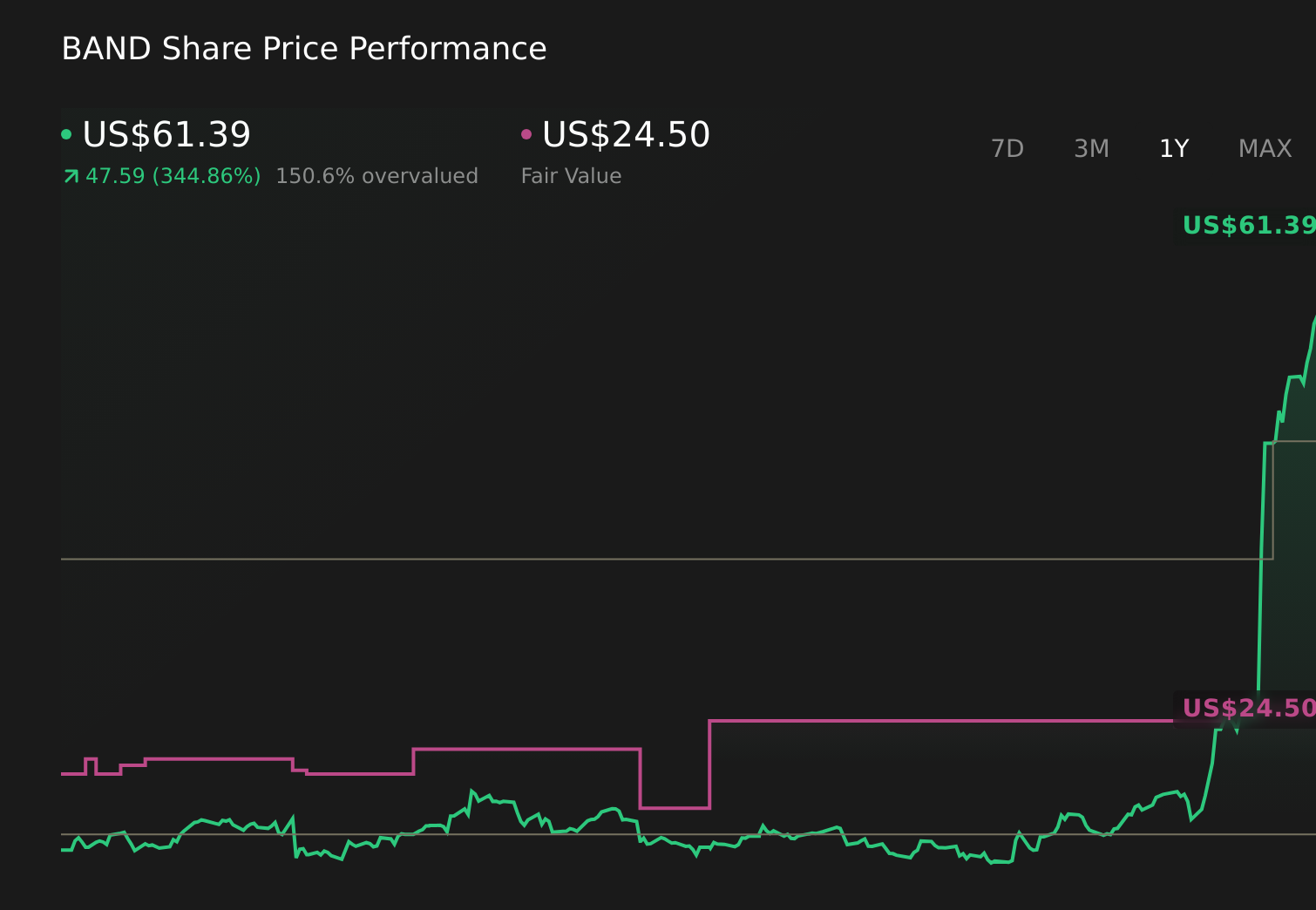

Bandwidth's narrative projects $987.7 million revenue and $17.8 million earnings by 2028. This requires 9.2% yearly revenue growth and a $27.8 million earnings increase from -$10.0 million today.

Uncover how Bandwidth's forecasts yield a $24.50 fair value, a 60% downside to its current price.

Exploring Other Perspectives

Before this upgrade, the most optimistic analysts were already modeling about US$1.2 billion of revenue and US$79.1 million of earnings by 2029, which is far more ambitious than the baseline view and leans heavily on AI driven growth. The latest surge in sentiment and guidance could support that story or expose where those expectations were too aggressive, so it is worth weighing how much faith you place in rapid AI monetization versus the risk of tighter pricing and slower adoption.

Explore 3 other fair value estimates on Bandwidth - why the stock might be worth over 2x more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Bandwidth research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Bandwidth research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bandwidth's overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.