Are Shares of Pinduoduo Attractive After 6.6% Dip Despite Strong International Growth?

PINDUODUO INC. PDD | 101.78 | -0.39% |

- Curious if PDD Holdings could be a hidden gem or already fully priced in? Let’s dig into what’s driving the current buzz and whether this stock is offering value right now.

- Although the shares recently dipped 6.6% over the last week, they’re still up 33.2% year-to-date and have gained 10.0% over the past twelve months. This demonstrates both volatility and potential for growth.

- Much of this movement has come alongside headlines about aggressive expansion into international markets and intensifying competition with global e-commerce players. In addition, regulatory updates in China have kept investors on their toes. These news events are fueling both excitement and caution among shareholders.

- PDD Holdings scores a strong 5/6 on our valuation checks, signaling it is undervalued in most categories we track. We will break down how we got here using traditional valuation approaches. Be sure to stick around because we have an even better way to spot value at the end.

Approach 1: PDD Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's value by forecasting its future cash flows and discounting them back to today using a required rate of return. This approach tries to answer the question, "What are all of PDD Holdings' expected future earnings worth in today's money?"

PDD Holdings currently generates CN¥93.25 Billion in Free Cash Flow. According to analyst projections, this figure could reach CN¥162.04 Billion by the end of 2027. Looking further ahead, extrapolated estimates suggest Free Cash Flow could surpass CN¥290.72 Billion by 2035. These robust cash flow projections provide the foundation for the DCF valuation of PDD Holdings.

All cash flow estimates are in Chinese Renminbi (CN¥), which is PDD Holdings' reporting currency. This helps provide a consistent valuation perspective even though the shares are listed in US dollars.

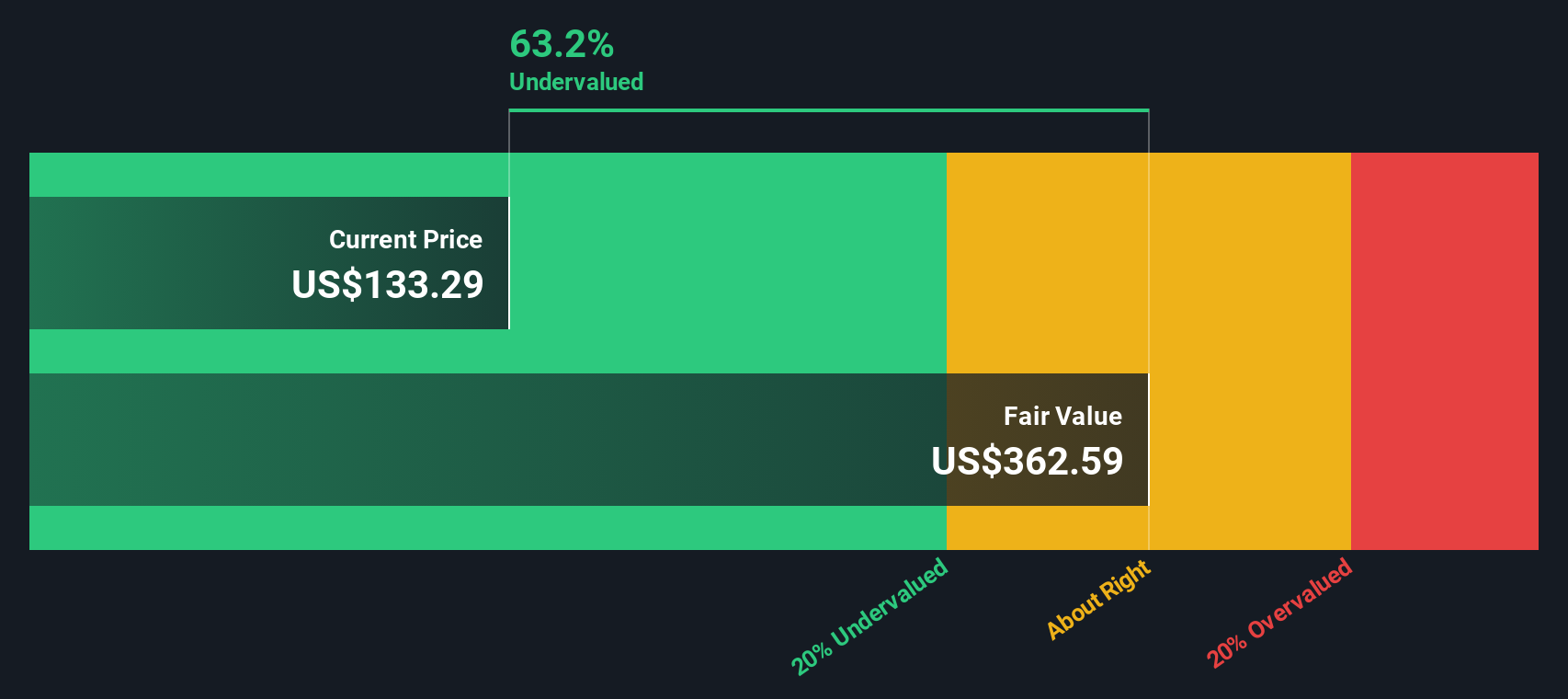

Based on these cash flow forecasts, the DCF model calculates an intrinsic value of $354.20 per share. With the current share price reflecting a 63.6% discount to this fair value, the stock appears significantly undervalued according to the model's methodology.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests PDD Holdings is undervalued by 63.6%. Track this in your watchlist or portfolio, or discover 899 more undervalued stocks based on cash flows.

Approach 2: PDD Holdings Price vs Earnings

The price-to-earnings (PE) ratio is widely recognized as the go-to valuation metric for profitable companies because it directly compares a company’s stock price with its actual earnings. This measure gives investors a way to see how much they’re paying for each dollar of profit, making it particularly relevant when net income is strong and consistent.

However, what counts as a “normal” or fair PE ratio depends on factors like the company’s expected future earnings growth, its risk level, and how it stacks up against competitors. Faster-growing or lower-risk companies can command higher PE multiples. In contrast, more uncertain prospects tend to trade at a discount.

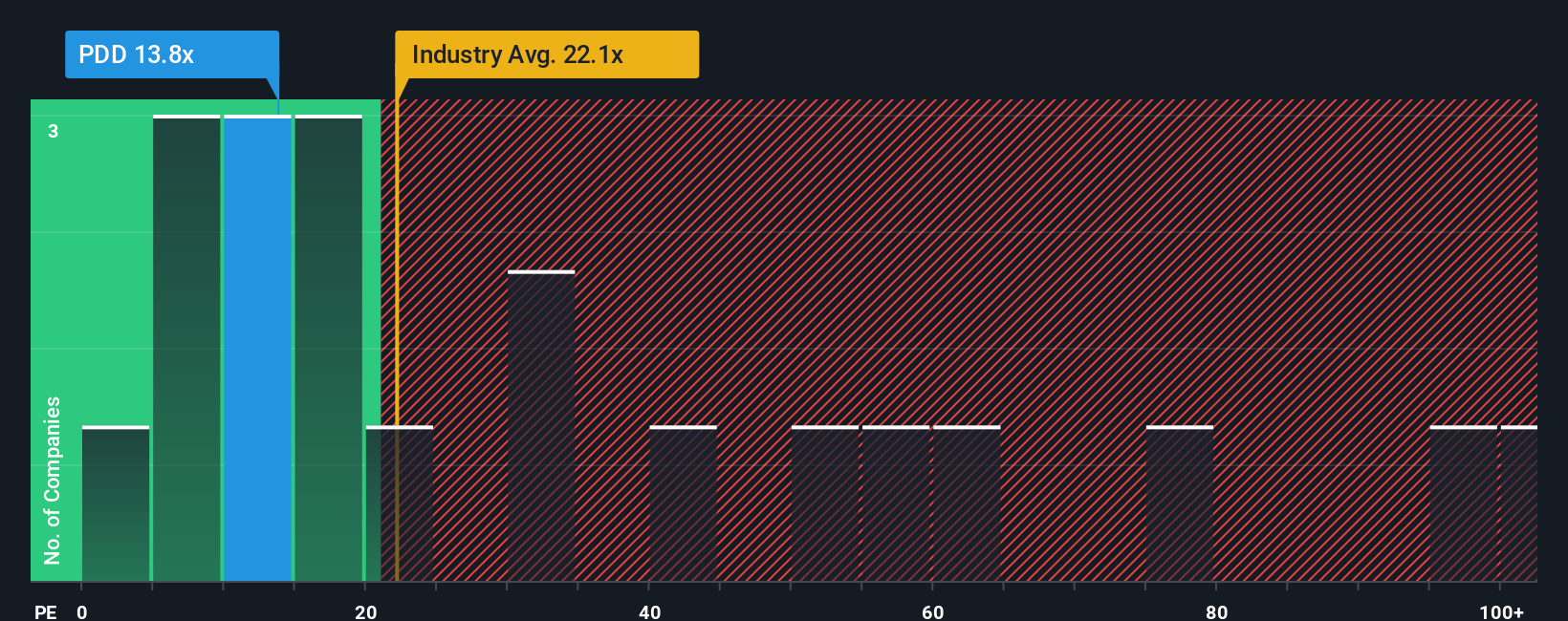

Currently, PDD Holdings trades at a PE ratio of 13.3x. For context, the Multiline Retail industry average sits at about 19.5x, while leading peers are at a much heftier 64.6x. On the surface, this suggests PDD Holdings is trading cheaply relative to both its sector and direct competitors.

To dig deeper, Simply Wall St’s “Fair Ratio” puts PDD Holdings' justified PE at 26.8x. This proprietary benchmark goes beyond simple peer or industry comparisons and considers the company’s growth prospects, risks, profit margin, market cap, and the entire industry context. By accounting for these factors, the Fair Ratio aims to give a more balanced view of where the stock’s multiple should reasonably be.

Comparing the actual PE of 13.3x to the Fair Ratio of 26.8x, PDD Holdings appears significantly undervalued on this metric. This underscores a potential value opportunity for investors.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1418 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your PDD Holdings Narrative

Earlier we mentioned that there's an even better way to understand valuation, so let's introduce you to Narratives, a more powerful, interactive approach now available to investors on Simply Wall St's Community page.

A Narrative is how you bring your own perspective to investing: it's the story you believe about a company, paired with a transparent set of financial assumptions including fair value, future revenue, earnings, and profit margins. Narratives link a company's real-world developments such as its leadership, risks, opportunities, and competitive advantages with a forecast of financial outcomes, and then translate those forecasts into a fair value for the stock.

Using Narratives, you can see how your outlook compares with other investors, helping you decide if now’s the time to buy or sell. If news breaks or earnings are released, Narratives update dynamically so your view always reflects the latest realities.

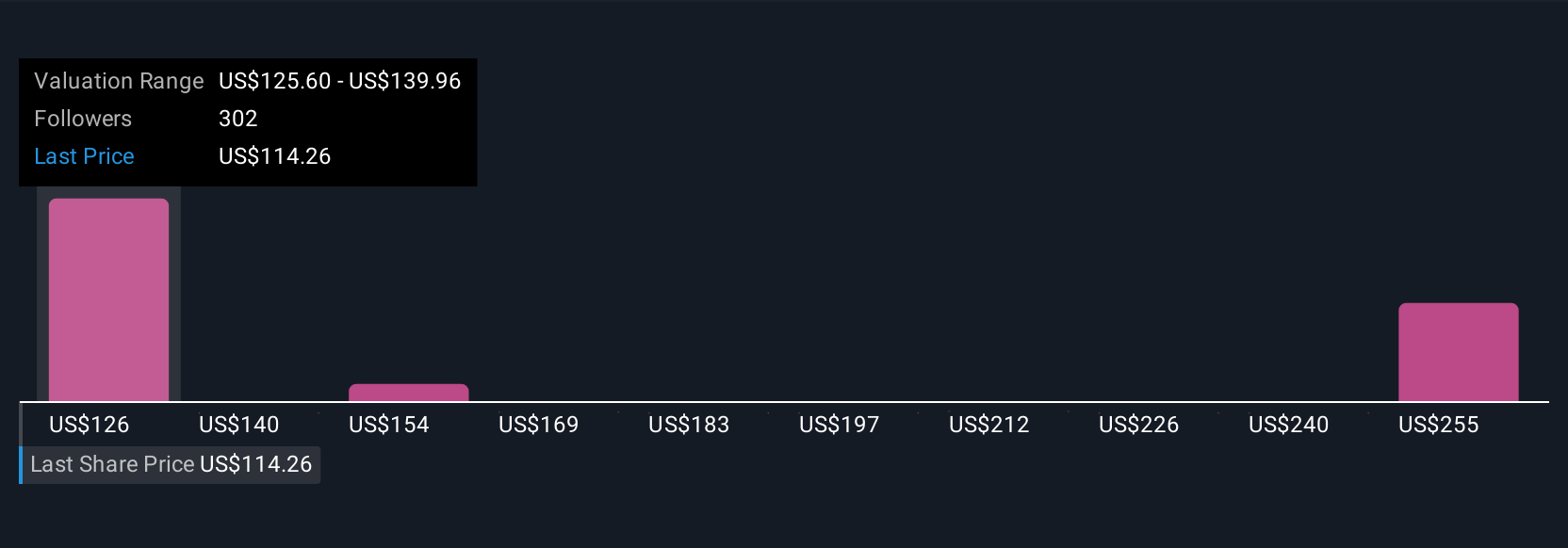

For example, some PDD Holdings Narratives on Simply Wall St see fair value as high as $165 per share based on accelerating international growth and expanding margins, while more cautious forecasts put it as low as $117, reflecting margin risks and regulatory headwinds. This allows you to quickly find a viewpoint that matches your own investment thesis.

Do you think there's more to the story for PDD Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.