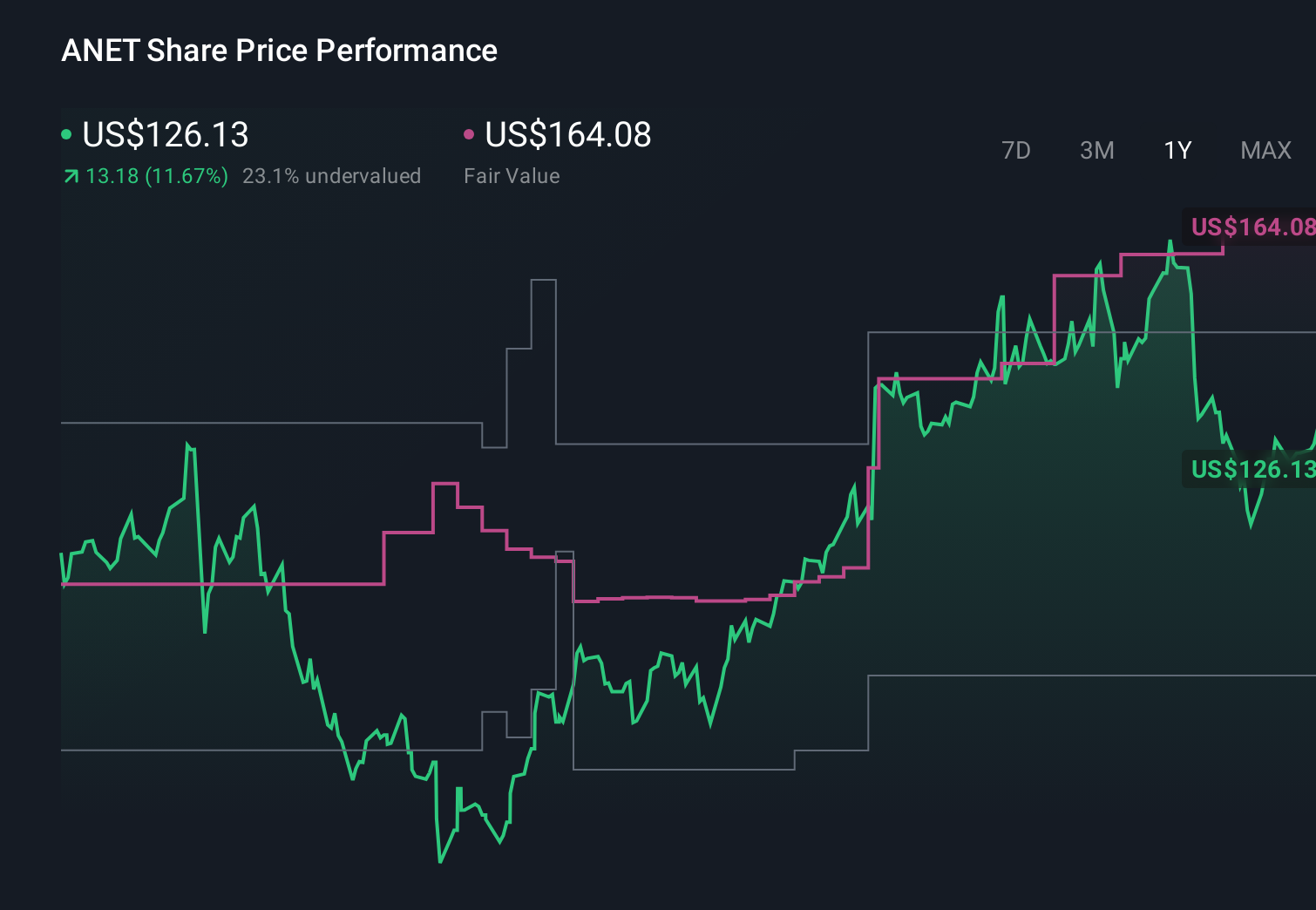

Arista Networks (ANET) Is Down 17.9% After Raising 2026 Revenue Outlook Amid AI-Driven Demand

Arista Networks, Inc. ANET | 0.00 |

- In early May 2026, Arista Networks reported first-quarter revenue of US$2,709 million and net income of US$1,022.9 million, and guided second-quarter revenue to about US$2.8 billion while raising its full-year 2026 revenue outlook to roughly US$11.5 billion despite industry-wide supply constraints pressuring margins.

- The results underscored how surging demand for Arista’s AI-focused networking platforms, including its 7800 AI spine and universal AI fabric offerings, is helping the company sustain growth even as shortages of wafers, silicon, and memory increase costs and operational complexity.

- Now we'll explore how this mix of strong AI-driven growth and margin pressure from supply shortages may influence Arista Networks’ investment narrative.

Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

Arista Networks Investment Narrative Recap

To own Arista Networks, you need to believe that AI data center buildouts will keep driving demand for its high-speed Ethernet platforms, while the company manages customer concentration and intensifying competition. The latest quarter’s strong US$2,709 million revenue and higher full year outlook reinforce the AI demand side of that thesis. At the same time, management’s warning about supply constraints and margin pressure highlights that the most immediate risk is execution under tight component availability.

The most relevant recent announcement is Arista’s raised 2026 revenue guidance to about US$11.5 billion, coupled with expectations that AI fabric sales will more than double to roughly US$3.5 billion. That outlook links directly to today’s results, underlining AI networking as the key short term catalyst while confirming that supply chain issues, including wafer and silicon shortages, could continue to pressure gross margins even as top line demand remains strong.

Yet behind the AI growth story, Arista’s heavy reliance on a handful of hyperscale and AI titan customers is a risk investors should be aware of, especially if...

Arista Networks' narrative projects $17.0 billion revenue and $6.2 billion earnings by 2029.

Uncover how Arista Networks' forecasts yield a $180.33 fair value, a 27% upside to its current price.

Exploring Other Perspectives

While consensus focuses on strong AI driven demand, the most cautious analysts remind you that their earlier forecasts of roughly US$15.5 billion revenue and US$6.0 billion earnings by 2029 already baked in significant concentration and margin risks, so this new supply constrained backdrop could push their narrative in a very different direction.

Explore 15 other fair value estimates on Arista Networks - why the stock might be worth just $135.94!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Arista Networks research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Arista Networks research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Arista Networks' overall financial health at a glance.

Contemplating Other Strategies?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Capitalize on the AI infrastructure supercycle with our selection of the 40 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 51 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.