Arista Networks (ANET) Is Up 8.5% After AI-Focused Beat, Guidance Hike And Gartner Leadership Gains

Arista Networks ANET | 0.00 |

- In recent weeks, Arista Networks has reported strong first-quarter 2026 results, raised its full-year growth and AI-centric revenue outlook, and been recognized as a Leader in Gartner’s 2026 Magic Quadrant for Enterprise Wired and Wireless LAN while launching new ruggedized switches and advanced AI-driven network operations tools.

- An interesting angle is how Arista is pairing its AI data center positioning with an expanding enterprise campus portfolio, potentially broadening its role from hyperscale backbone provider to end-to-end networking partner for a wider range of customers.

- We’ll now examine how Arista’s enhanced AI fabrics targets and Gartner-recognized campus expansion shape the company’s existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 46 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Arista Networks Investment Narrative Recap

To own Arista, you need to believe that AI data center buildouts and enterprise networking upgrades keep requiring its high performance switches and software, while it gradually reduces dependence on a handful of hyperscale and AI titan customers. The latest Q1 beat, higher full year and AI revenue outlook, and Gartner recognition support that thesis, but softer Q2 guidance and supply chain pressures keep near term demand volatility and margin pressure as the key risks rather than changing them.

The Gartner 2026 Magic Quadrant “Leader” rating for enterprise wired and wireless LAN, alongside ruggedized campus switches and new AI driven AIOps tools, looks especially relevant here. As Arista extends from AI data center fabrics into campus and industrial environments, it potentially broadens its customer base and revenue mix, which directly touches the concentration risk that more cautious analysts highlight around its top cloud and AI customers.

Yet, against all this optimism, growing insider selling and intense competition in AI networking are things investors should be aware of before they...

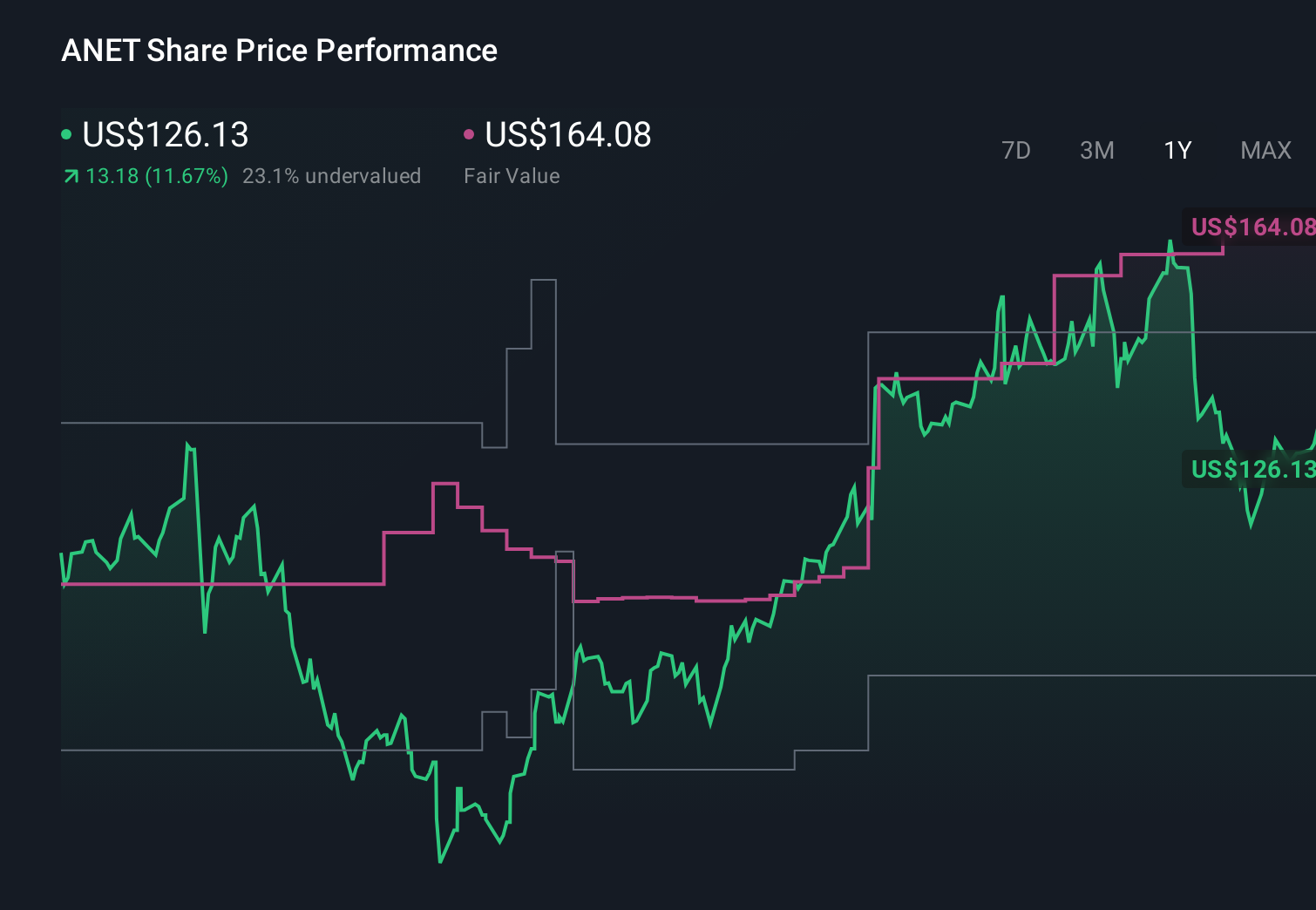

Arista Networks' narrative projects $18.1 billion revenue and $6.6 billion earnings by 2029. This requires 23.0% yearly revenue growth and an earnings increase of about $2.9 billion from $3.7 billion today.

Uncover how Arista Networks' forecasts yield a $188.20 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming revenue of about US$15.5 billion and earnings near US$6.0 billion by 2029, and you can see how their focus on hyperscaler dependence and margin pressure offers a much more pessimistic counterpoint to the recent upbeat AI and campus news.

Explore 13 other fair value estimates on Arista Networks - why the stock might be worth as much as 35% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Arista Networks research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Arista Networks research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Arista Networks' overall financial health at a glance.

Searching For A Fresh Perspective?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.