Arlo (ARLO) Stock Could Be Cheap On Cash Flow Yet Rich On Earnings

ARLO TECHNOLOGIES, INC. ARLO | 0.00 |

Arlo Technologies stock has more than doubled over the past five years, yet today there is a clear split in what the valuation tools are saying. The Discounted Cash Flow (DCF) intrinsic value points to meaningful upside, while market multiples suggest the shares already trade at a premium.

- A roughly 111.1% return over five years puts Arlo Technologies among the stronger performers in its peer group, which raises the bar for what counts as good value at the current price.

- The push into AI powered connected care services, highlighted by the expanded Aloe Care and Home Helpers partnership, can support investor expectations for recurring revenue. However, the recent one year share price decline of 20.0% underlines the risk that growth or execution may fall short of what the market is pricing in.

- Arlo Technologies scores 3 out of 6 on the valuation checks, which points to a mixed picture rather than a clear bargain or clear overvaluation.

The issue now is whether the DCF based intrinsic value case or the richer market multiple view gives the better guide to where Arlo Technologies should trade from here.

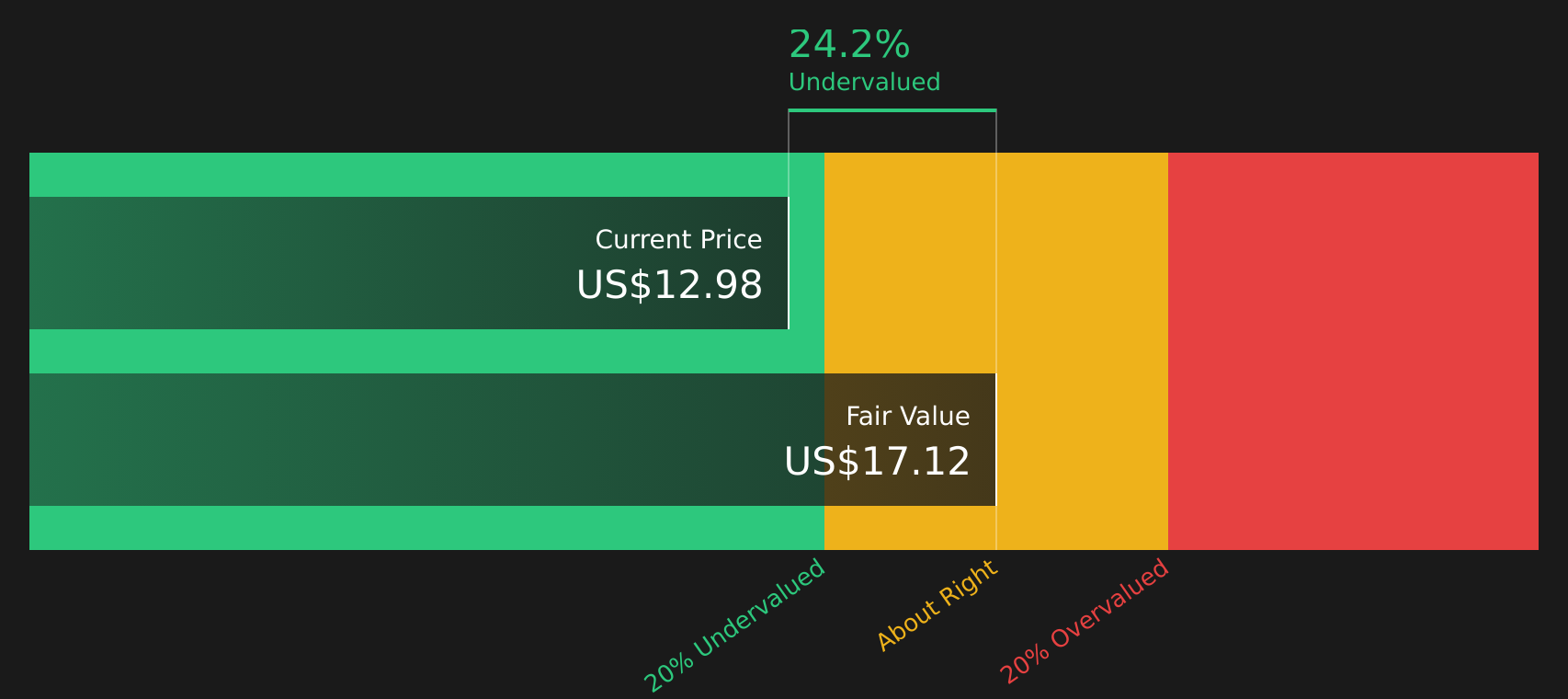

Is Arlo Technologies a Bargain on Cash Flow?

The Discounted Cash Flow (DCF) model values Arlo Technologies by projecting future free cash flows and discounting them back to today. In this view, Arlo’s latest twelve month free cash flow of about $68.9 million is treated as a base that grows over time rather than a one off spike. The model uses a 2 Stage Free Cash Flow to Equity approach to reflect an initial growth phase that then tapers.

Those cash flow projections translate into an estimated intrinsic value of about $17.10 per share, which compares to a current share price that implies a 20.7% discount. Because the expanded Aloe Care and Home Helpers partnership relates directly to subscription based, connected care services, the DCF emphasis on growing recurring cash flows helps explain why the intrinsic value is above the current Arlo Technologies share price.

On the DCF numbers alone, Arlo Technologies appears undervalued relative to the cash flows the model is pricing in.

Our Discounted Cash Flow (DCF) analysis suggests Arlo Technologies is undervalued by 20.7%. Track this in your watchlist or portfolio, or discover 41 more high quality undervalued stocks.

Does Arlo Technologies Look Pricey on Earnings?

The P/E ratio is a useful way to look at Arlo Technologies because the stock currently has positive earnings to compare against its price. Arlo trades on a P/E of 48.0x, which is well above the Electronic industry average of 32.8x and also ahead of the peer group average of 23.5x.

On Simply Wall St's fair P/E estimate of 30.4x, which reflects factors such as Arlo Technologies' growth profile, margins, size and risk, the current 48.0x multiple sits at a clear premium. That gap indicates investors are already paying a higher multiple for the company, even before considering what happens with future execution in areas like connected care and subscription services.

On the P/E multiple, Arlo Technologies stock currently appears overvalued relative to what the fair ratio model suggests.

The Arlo Technologies Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the Arlo Technologies valuation puzzle leaves off by spelling out which assumptions about Arlo Technologies' future growth, margins and earnings would need to hold for the stock to be worth materially more or less than today's price. They sit on Simply Wall St's Community page. Each Narrative ties a specific set of potential catalysts and risks to its own view of fair value, so you can watch over time which version of Arlo Technologies' story is actually unfolding.

If you have a clear view on whether Arlo Technologies' expanded AI powered Aloe Care wellness service with Home Helpers can support the current valuation, consider adding your own Narrative to the Simply Wall St community to set out the numbers behind your thesis. It is a chance to put your assumptions on growth, margins and execution on record and see how they hold up as new results and updates arrive.

Do you think there's more to the story for Arlo Technologies? Head over to our Community to see what others are saying!

The Bottom Line

For Arlo Technologies, the Discounted Cash Flow (DCF) estimate points to meaningful upside from intrinsic value, while the P/E based view flags the stock as overvalued relative to sector peers. That gap reflects two different focal points: cash flow and capital needs on one side, and market expectations and sentiment on the other. With the broader valuation checks landing in mixed territory, the key question is whether Arlo can turn its connected care and subscription push into durable cash flows strong enough to justify both the current multiple and any perceived discount on intrinsic value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.