Arm Holdings (NasdaqGS:ARM) Valuation in Focus After Nvidia-Intel Alliance Raises Competitive Stakes

ARM Holdings PLC Sponsored ADR ARM | 153.25 | +1.31% |

Arm Holdings Faces New Headwinds as Nvidia Lines Up with Intel

Arm Holdings (NasdaqGS:ARM) investors woke up to a jolt after Nvidia announced a $5 billion partnership with Intel, a move that might reshape dynamics in the chip sector. Nvidia and Intel are joining forces to develop custom data center and PC chips, including offerings targeting the x86 space. For anyone holding Arm or considering a position, this event hits squarely at the company's ambitions, especially with Arm transitioning from simply licensing chip architecture to designing its own. This development now places it in more direct competition with Nvidia.

This backdrop helps explain the recent wobble in Arm’s stock price. The shares have slipped just over 6% in the past week, even after a modest 1% gain yesterday, though they’re still up around 13% for the year. The shift toward chip design has brought new excitement and risk, with annual revenue and net income up by double digits. However, the competitive field is growing more complex. If momentum is uncertain in the near term, it is likely because investors are recalibrating expectations around Arm’s evolving business and the impact of heavyweight rivals teaming up.

So as Arm pivots into direct rivalry with its largest customers and partners, is the current price an opportunity, or is the market already baking in all of its future growth?

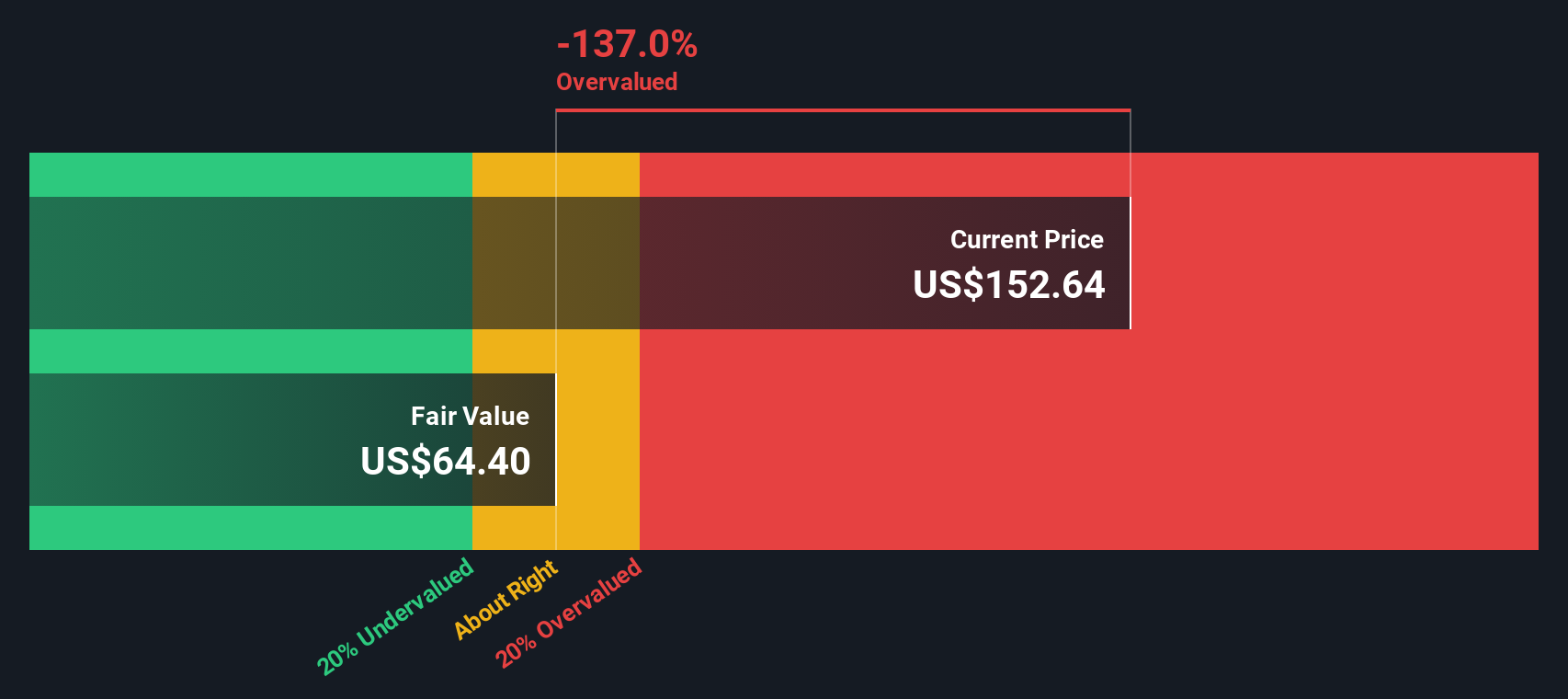

Most Popular Narrative: 5.3% Undervalued

According to the most-followed valuation narrative, Arm Holdings is seen as modestly undervalued relative to its projected future growth, supported by robust expectations for AI and data center expansion.

“Arm's accelerating penetration in AI data centers, driven by hyperscalers shifting to custom silicon featuring Arm Neoverse CPUs, positions the company to capture significant royalty revenue growth. Especially as their market share soars from about 18% to nearly 50% in a year, a surge in demand for connected devices and intelligent edge computing (IoT, automotive, wearables) continues to expand Arm's addressable market.”

Want to understand how Arm’s future rests on bold projections and premium technology monetization? The hidden ingredients fueling this price target range from ambitious revenue climbs to aggressive profit assumptions, all backed by industry-shaking shifts in data center and AI adoption. Curious what underpins the bullish outlook behind this undervaluation? The full narrative unpacks all the game-changing metrics that analysts believe will define Arm’s value.

Result: Fair Value of $152.59 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, rising R&D costs and reliance on premium smartphones could pose real challenges if diversification or new chip initiatives underperform expectations.

Find out about the key risks to this Arm Holdings narrative.Another View: What Do Other Methods Say?

Looking from a different perspective, our DCF model currently suggests Arm is trading above its intrinsic worth. This indicates the market might be overestimating future cash flow potential. Does this cast doubt on the recent optimism?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Arm Holdings Narrative

If you would rather dig deeper and draw your own conclusions, you can quickly assemble a personalized narrative and analysis in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Arm Holdings.

Looking for More Investment Ideas?

Why stop at just one opportunity? Give yourself an edge by tapping into handpicked stock screens built for today’s most ambitious investors. If you want to get ahead of the next market move, don’t let these strategies pass you by.

- Accelerate your search for tomorrow’s tech trailblazers by targeting the hottest companies innovating with AI penny stocks.

- Uncover potential bargains in the market by focusing on businesses that stand out as undervalued stocks based on cash flows.

- Boost your steady income potential by finding reliable, high-yield picks through dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.