Arrow Electronics (ARW): Assessing Valuation After Expanding with AirBorn’s Aerospace and Defense Portfolio

Arrow Electronics, Inc. ARW | 0.00 |

Most Popular Narrative: 8% Overvalued

The most widely followed narrative sees Arrow Electronics as trading above its estimated fair value, despite solid growth drivers and resilient margins in the forecast.

Accelerating adoption of cloud, infrastructure software, cybersecurity, and mid-market as-a-service offerings, notably through ArrowSphere, is increasing Arrow's exposure to higher-margin, recurring revenue streams. This is expected to support both revenue growth and margin stability in future quarters.

Is this valuation too hot to handle? Arrow's future is pegged on strategic bets in recurring revenue and digital expansion. Get ready for bold projections, aggressive financial moves, and assumptions that could surprise even the most seasoned investors. The real question: what numbers are underpinning this price premium?

Result: Fair Value of $116.75 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, accelerating digitalization and supply chain shifts could challenge Arrow’s distribution model and margins. This could potentially test the resilience of its current growth trajectory.

Find out about the key risks to this Arrow Electronics narrative.Another View: What Do Valuation Ratios Suggest?

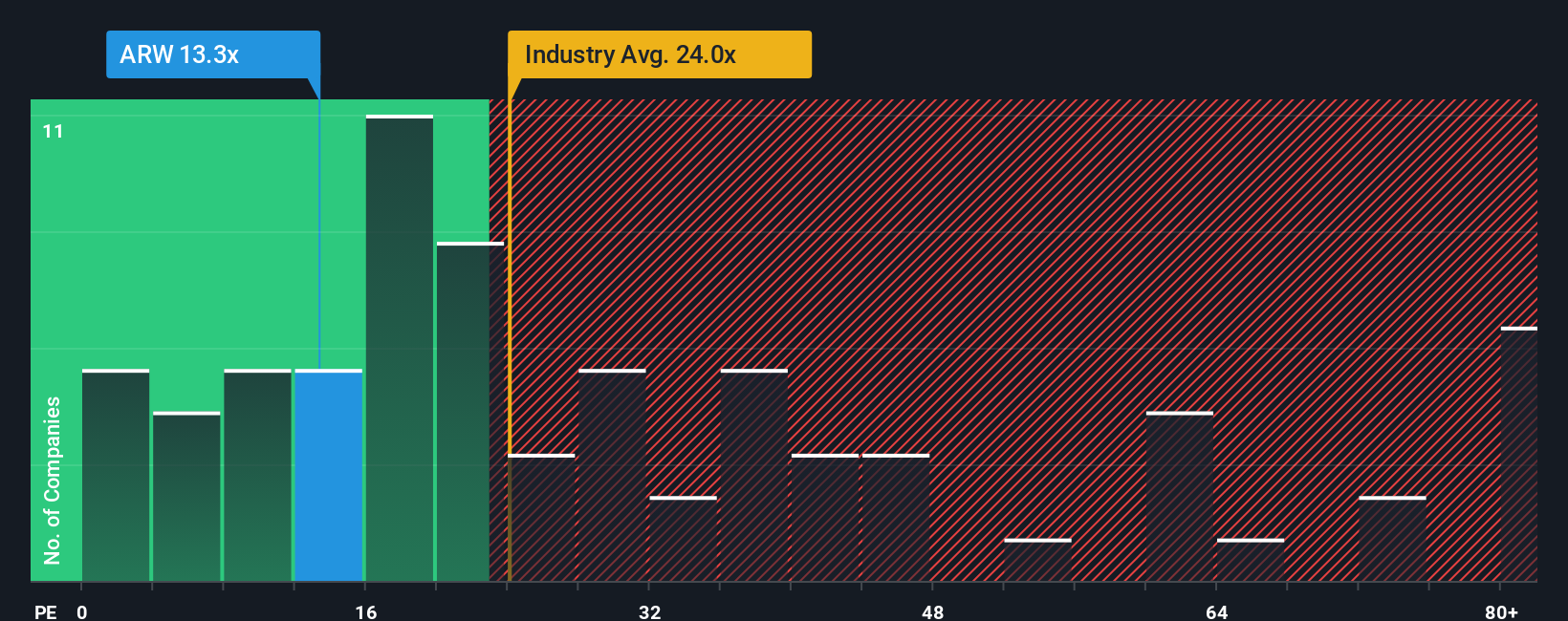

Looking from another angle, Arrow’s current valuation appears more appealing when compared to sector averages. Its market multiple is lower than the broader industry, which raises a new question: is the crowd overlooking something?

Build Your Own Arrow Electronics Narrative

If you see things differently or want to dig into the numbers your way, you can craft a custom narrative of your own in just a few minutes. Do it your way

A great starting point for your Arrow Electronics research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Opportunities?

Expand your horizons and unlock new possibilities by harnessing the power of unique stock screeners. Don't let potential winners slip by while others act first. Seize smarter investment ideas below:

- Capture future gains with undervalued stocks based on cash flows that spotlight companies trading below intrinsic value and primed for a turnaround.

- Ride the next innovation wave by scouting AI penny stocks shaping tomorrow through intelligent automation, data analytics, and breakthrough tech.

- Grow your portfolio with steady income by researching dividend stocks with yields > 3% offering exceptional yields and a powerful track record for payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.