Ashland (ASH) Valuation Check After Q2 Earnings Miss And Softer Intermediates Pricing

Ashland Inc. ASH | 0.00 |

Ashland (ASH) stock is back in focus after the company posted weaker than expected Q2 earnings and sales, with pressure in Intermediates and pricing prompting investors to reassess profit expectations.

The recent Q2 miss comes after a mixed stretch for Ashland, with a 30 day share price return of 11.73% but a 90 day share price decline of 5.31%, while the 1 year total shareholder return of 19.54% contrasts with weaker 3 and 5 year total shareholder returns.

If Ashland’s recent volatility has you thinking about where else to put fresh capital to work, it can help to broaden your search and uncover 20 top founder-led companies

With Ashland stock recently up 11.73% over 30 days but still down 5.31% over 90 days and carrying weaker 3 and 5 year returns, the key question is whether this reset leaves undervaluation on the table or if the market is already pricing in future growth.

Most Popular Narrative: 13.7% Undervalued

Ashland's most followed narrative places fair value at $67.10 versus the last close at $57.90, framing the recent Q2 reset as a potential valuation gap rather than a permanent earnings downgrade.

The global shift toward sustainable and bio-based materials, driven by regulatory requirements and consumer preference, continues to gain momentum, benefiting Ashland's specialty chemicals portfolio that is now more focused on high-value, sustainable, and compliant solutions, this is expected to support top-line revenue growth and margin resilience over the long term.

Want to see what sits behind that confidence in future margins and cash flows? The narrative leans heavily on compound earnings, richer profitability and a re-rated future earnings multiple, all tied to detailed 3 year forecasts and a specific discount rate.

Result: Fair Value of $67.10 (UNDERVALUED)

However, this story can break if prolonged demand softness and competition continue to pressure Specialty Additives, or if consumer and customer shifts unsettle Ashland’s Personal Care and Life Sciences exposure.

Another View on Valuation

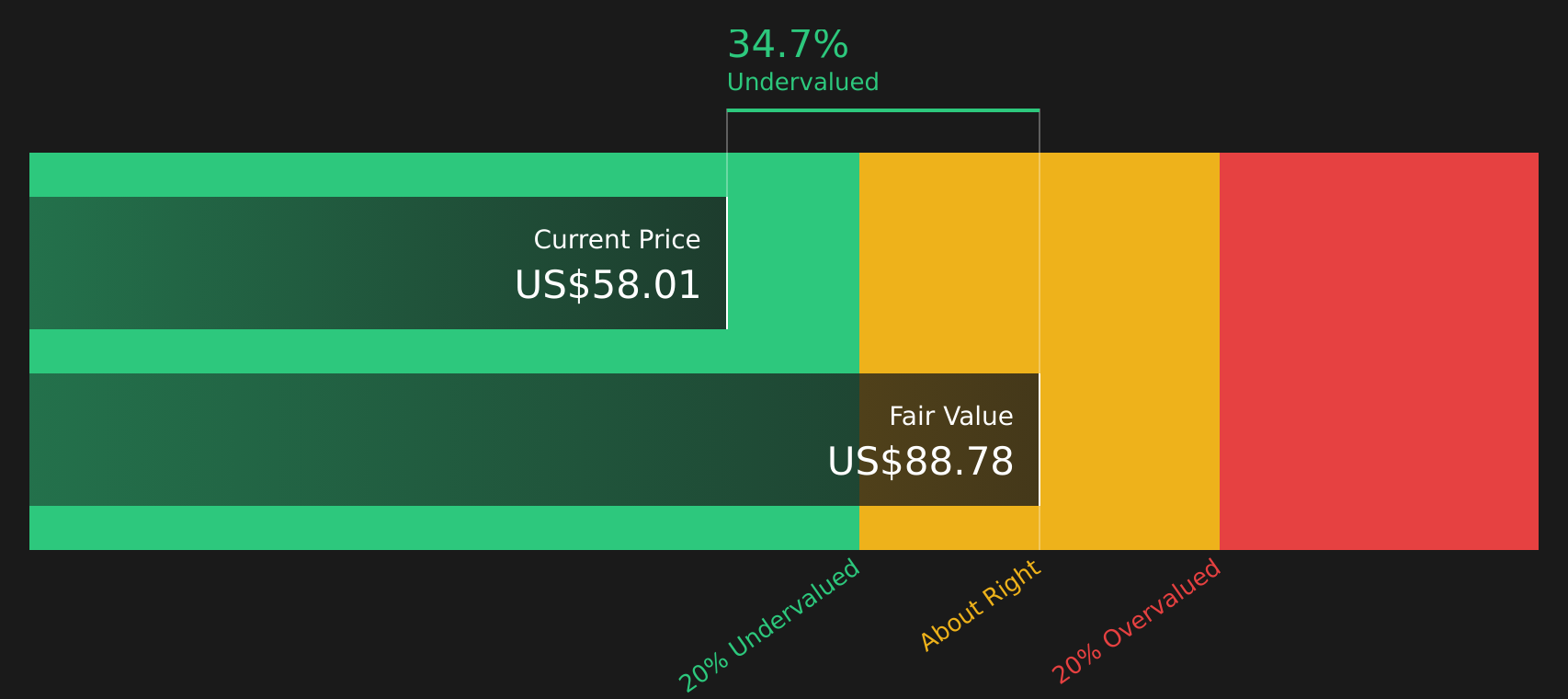

The narrative based on future cash flows suggests Ashland stock is trading at a discount, with our DCF model indicating a fair value of $88.77 versus the current $57.90, which points to undervaluation. The question is whether those long term cash flow assumptions feel realistic to you.

Next Steps

Mixed signals on valuation and earnings risk can be hard to weigh, so move quickly, review the data yourself, and weigh 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Ashland has sharpened your focus, do not stop here. Use the Simply Wall Street Screener to hunt for fresh opportunities before they move without you.

- Target resilient income by scanning for companies in the 10 dividend fortresses that may align with your dividend goals.

- Hunt for potential value opportunities by reviewing the screener containing 22 high quality undiscovered gems that could fit your watchlist before others pay attention.

- Prioritise downside protection by checking out 63 resilient stocks with low risk scores that might suit a more cautious approach to equity investing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.