ASML (NasdaqGS:ASML) Valuation: Is the Chip Giant Fully Priced After Steady Recent Gains?

ASML Holding NV ADR ASML | 1317.23 | -3.13% |

ASML Holding’s momentum has really gathered pace this year, with the share price climbing over 48% year-to-date and delivering an impressive 1-year total shareholder return of 55%. This consistent upward movement suggests growing confidence in ASML’s long-term growth prospects, especially as demand in the semiconductor space increases.

If you’re looking for more compelling tech innovators making headlines, it’s a great time to check out See the full list for free.

But with ASML Holding’s impressive run so far, investors have to wonder whether the current stock price still offers upside potential, or if expectations for future growth are already fully reflected in the valuation.

Most Popular Narrative: 3.5% Overvalued

ASML Holding’s fair value, as seen by the most widely followed narrative authored by Investingwilly, sits below the company’s latest closing price, pointing to a modestly overvalued position. The narrative’s assumptions differ from broader market sentiment, so it’s essential to dig into the key drivers behind their calculation.

ASML is the only company in the world producing EUV lithography tools. These machines are essential for making the world’s most powerful semiconductors. This gives ASML a near-monopoly in a fast-growing market driven by AI, 5G, and high-performance computing.

Curious why a company dominating an industry could trade above fair value? The narrative’s bold assumptions rest on market-shifting technology, premium margins, and a future growth pace that’s the envy of the sector. Uncover the specific forecasts and financial levers driving this decisive fair value stance. One metric in particular could flip the whole story.

Result: Fair Value of $1002.53 (OVERVALUED)

However, risks remain, including potential export restrictions to China and macroeconomic uncertainty. Either of these factors could quickly change the valuation narrative.

Another View: Multiples Tell a Different Story

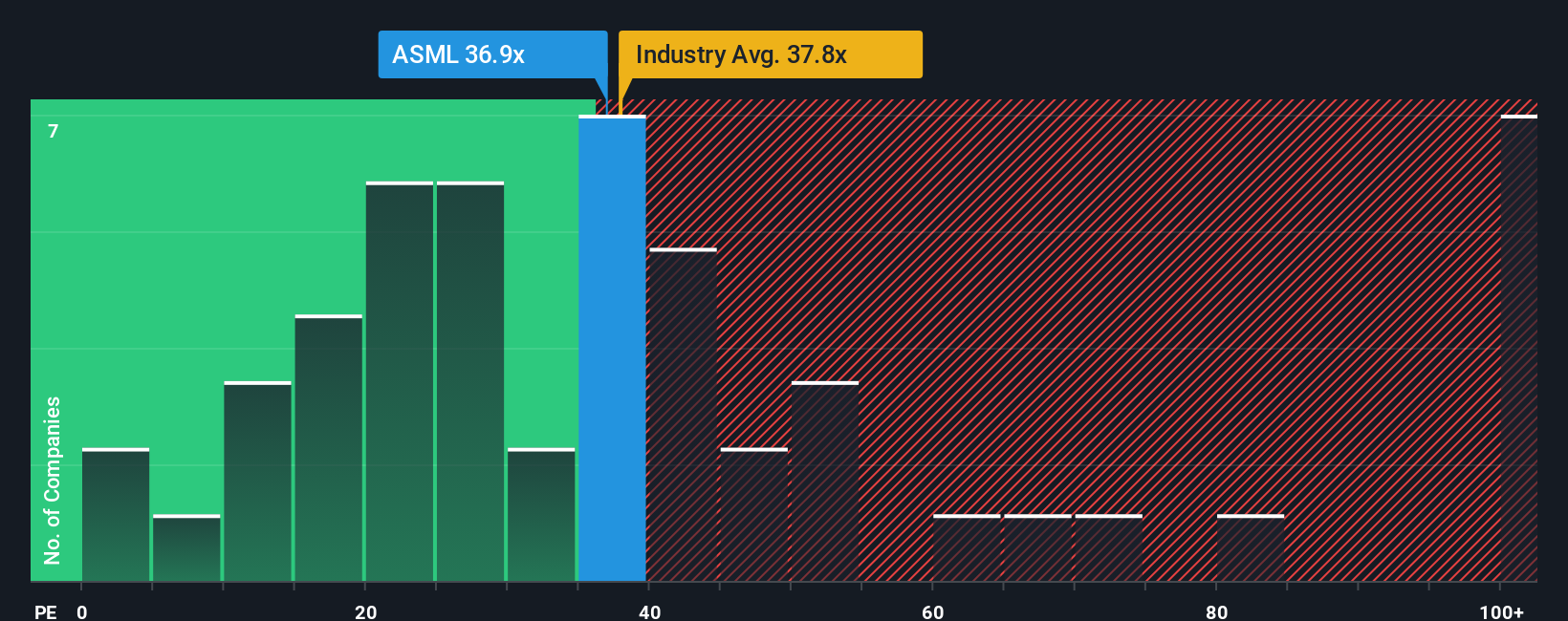

While one narrative pegs ASML as slightly overvalued, a look at its price-to-earnings ratio adds nuance. ASML trades at 36.5x earnings, slightly above the US semiconductor average of 35.9x but below the peer average of 40.6x. Interestingly, it is also under the estimated fair ratio of 38x, hinting at possible upside if the market shifts its expectations. Does this suggest the market may be underestimating ASML’s prospects, or is caution still warranted?

Build Your Own ASML Holding Narrative

If you want to test these assumptions for yourself or reach a different conclusion, you can dive into the numbers and put together your own narrative in just a few minutes. Do it your way

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding ASML Holding.

Looking for More Smart Investment Ideas?

Great strategies are just the start. The real winners are those who keep uncovering fresh opportunities before the crowd does. Don’t let your next potential game-changing stock slip away.

- Capture income by targeting these 14 dividend stocks with yields > 3% that consistently reward shareholders with yields above 3%.

- Jump ahead of the curve with these 27 AI penny stocks poised to benefit from the accelerating impact of artificial intelligence.

- Position your portfolio for bargains with these 882 undervalued stocks based on cash flows that show potential based on solid cash flow fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.