Assessing 10x Genomics (TXG) Valuation After Q1 2026 Results And Rising AI Trading Interest

10x Genomics TXG | 0.00 |

Q1 earnings spark fresh interest in 10x Genomics

10x Genomics (TXG) has drawn renewed attention after reporting first quarter 2026 results that paired lower year-on-year revenue with a sharply smaller net loss, alongside increasingly discussed AI-driven and institutional trading activity.

The share price is US$21.20 after a 1-month share price return that is down 18.71%, although the 90-day share price return is up 17.00%. The 1-year total shareholder return of 125.77% contrasts sharply with the 3-year and 5-year total shareholder returns, which remain deeply negative. This suggests sentiment has improved recently despite a weak longer-term record.

If the mix of genomics, tools and AI interest has your attention, this could be a good moment to scan other healthcare-focused AI opportunities using the 32 healthcare AI stocks

With revenue growth, a smaller loss, and AI-fueled trading interest on the table, the key question now is simple: Is 10x Genomics still undervalued, or is the stock already pricing in future growth?

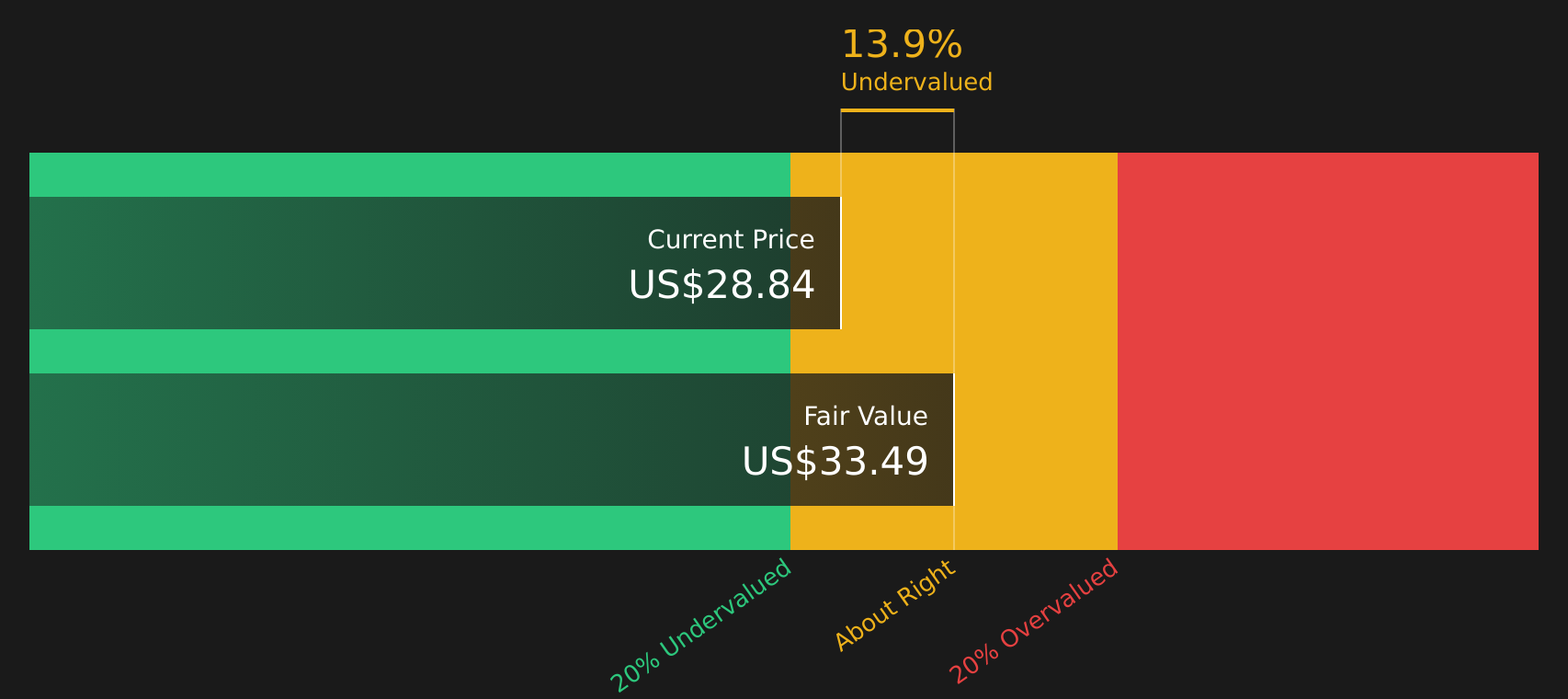

Most Popular Narrative: 5.2% Overvalued

The most followed valuation narrative puts 10x Genomics' fair value at $20.14, slightly below the last close at $21.20, framing a modest premium at current levels.

The acquisition of Scale Biosciences broadens 10x Genomics' technical capabilities in single-cell analysis, allowing integration of foundational innovations like combinatorial indexing and quantum barcoding, which may accelerate innovation, reduce costs, and open up new high-value markets, positively impacting future revenue growth and margins.

Curious what kind of revenue path, margin lift, and future earnings multiple are baked into that fair value line? The full narrative spells out the financial blueprint in detail.

Result: Fair Value of $20.14 (OVERVALUED)

However, these assumptions could be challenged if academic funding remains tight or if lower pricing on single cell and instrument platforms weighs more heavily on revenue and margins.

Another angle on value: DCF vs market multiples

The analyst narrative points to 10x Genomics trading at about a 5.2% premium to an estimated fair value of $20.14. In contrast, our DCF model suggests the stock is trading about 38% below a future cash flow value of $34.20. When two methods disagree this much, which one do you trust more, and why?

Next Steps

With the mixed signals in this story, now is the time to look at the data yourself and decide what really matters for you. To round out your view, check the balance between potential upside and downside with the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If 10x Genomics is on your radar, do not stop here. Use the tools available to scout other stocks that could fit your goals just as well.

- Target potential bargains by checking out companies flagged as having attractive valuations in the 51 high quality undervalued stocks.

- Prioritise resilience by scanning the 65 resilient stocks with low risk scores for stocks that score well on stability and downside protection.

- Hunt for fresh opportunities that the crowd may be overlooking with the screener containing 21 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.