Assessing ADTRAN Holdings (ADTN) Valuation After Terabit Class Edge Router Expansion

ADTRAN Holdings, Inc. ADTN | 13.21 | +2.17% |

ADTRAN Holdings (ADTN) expanded its edge routing portfolio with new Terabit class routers featuring 400Gbit/s interfaces, giving operators compact, higher-capacity options at the network edge for fiber access, aggregation and mobile backhaul.

The launch of the new Terabit class edge routers lands at a time when ADTRAN Holdings' 30 day share price return of 28.03% and 90 day share price return of 48.39% suggest building momentum, even though the 5 year total shareholder return of 25.40% remains weak.

If this kind of networking upgrade has your attention, it could be a good moment to see what else is moving in the broader connectivity and infrastructure space through 28 power grid technology and infrastructure stocks

With shares up 73.35% over the past year and trading around an 8.70% discount to the US$14.00 analyst price target, the real question is whether ADTRAN is still mispriced or if the market already anticipates future growth.

Most Popular Narrative: 8% Undervalued

With ADTRAN Holdings last closing at $12.88 against a narrative fair value of $14.00, the current pricing gap rests on a detailed long term earnings story.

Expanding global demand for high speed broadband, particularly residential fiber upgrades and multi gigabit services, is fueling strong customer wins and backlog growth across both North America and Europe, supporting continued revenue acceleration over the coming quarters. Rising infrastructure investment for AI computing, cloud, and 5G densification is driving higher demand for ADTRAN's optical networking solutions and cross selling opportunities, which should boost both revenue and market share as these trends intensify.

If you want to see what sits behind that 8% gap, the narrative explains how revenue mix, margin rebuild and future earnings expectations all connect.

Result: Fair Value of $14 (UNDERVALUED)

However, there is still real downside risk if currency swings pressure already weak net income or if broadband buildouts in key US and European markets slow materially.

Another View: DCF Flips The Story

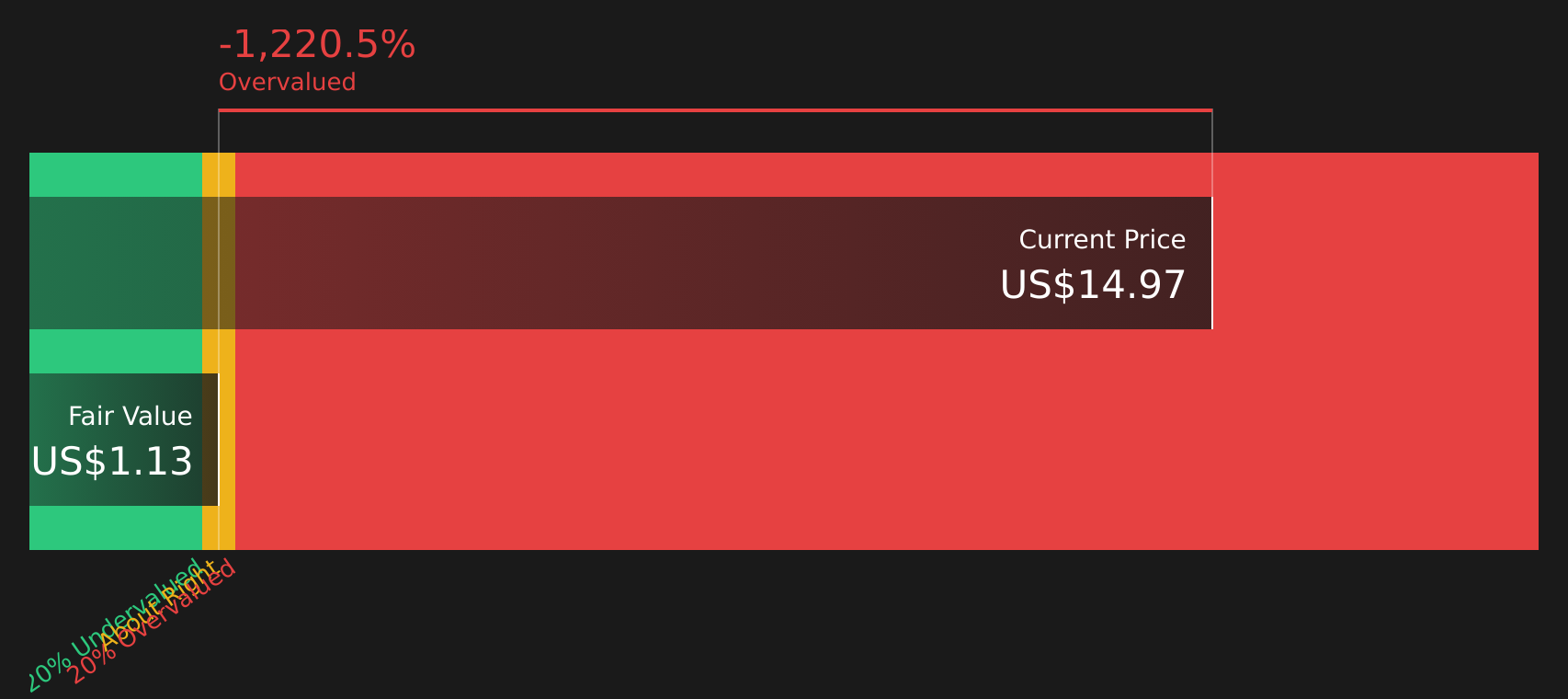

While the narrative fair value sits at $14 based on earnings potential, the SWS DCF model points the other way and puts ADTRAN's future cash flow value at just $1.13 per share. This frames the stock as meaningfully overvalued on that measure. Which story do you think fits your thesis?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ADTRAN Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 59 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals across price action and valuation models, the real edge comes from seeing the numbers for yourself and weighing both risks and rewards. To move quickly from headline impressions to your own conviction, start by reviewing the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If ADTRAN has sharpened your focus, do not stop here. The right stock idea at the right time can make a real difference to your portfolio.

- Spot potential value plays early by scanning 59 high quality undervalued stocks, which pairs strong fundamentals with prices that may not fully reflect their strengths.

- Build a sturdier portfolio core using the solid balance sheet and fundamentals stocks screener (40 results) to find companies with financial structures that can better handle pressure.

- Balance growth goals with stability by reviewing the 68 resilient stocks with low risk scores, which scores well on resilience while still offering room for upside.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.