Assessing Akamai Technologies (AKAM) Valuation After A Strong 1 Year Share Price Run

Akamai Technologies, Inc. AKAM | 0.00 |

Recent performance snapshot for Akamai Technologies (AKAM)

Akamai Technologies (AKAM) has drawn investor attention after a strong run, with the stock up about 68% year to date and roughly 88% over the past year based on total return.

Over shorter windows, performance has been mixed, with the stock down around 0.9% on the day and about 2.1% over the past week, while showing an increase of roughly 50% over the past month and 45% over the past 3 months.

The company reports annual revenue of about US$4.27b and net income of roughly US$435.18m, with both revenue and net income growth rates in the single to mid teens based on the figures provided.

For investors, the key takeaway is that Akamai’s 1-year total shareholder return of 88.11% and share price gains over the past quarter indicate that momentum has been building despite a recent pullback from the US$143.13 level.

If Akamai’s recent run has you reassessing your exposure to digital infrastructure and security, it can be useful to scan for other AI infrastructure beneficiaries using the Simply Wall St screener for 47 AI infrastructure stocks

After a 68% gain year to date and a 1 year total return of 88.11%, plus an intrinsic value estimate that sits above the current US$143.13 share price, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 9% Undervalued

The most followed valuation narrative pegs Akamai Technologies' fair value at about $157.16, above the recent $143.13 close, and ties that gap tightly to AI driven infrastructure demand and heavier investment.

Akamai's continued investment and go to market transformation in security and compute, including expanded sales capacity and channel partnerships, should enable it to tap further into the expanding addressable market for cloud and edge security, likely contributing to both top line growth and long term earnings leverage as these businesses scale.

Read the complete narrative. Read the complete narrative.

Want to see what kind of revenue mix and profit margins would justify that higher fair value? The narrative leans on faster growth in security and compute, richer earnings power, and a future earnings multiple that sits well above broad US IT peers. Curious which assumptions need to hold for that price target to stack up over time? The full story joins those moving parts into one valuation roadmap.

Result: Fair Value of $157.16 (UNDERVALUED)

However, this AI and security focused narrative could be challenged if core CDN revenues weaken faster than expected, or if heavier CIS and compute investment keeps margins under pressure.

Another View on Akamai’s Valuation

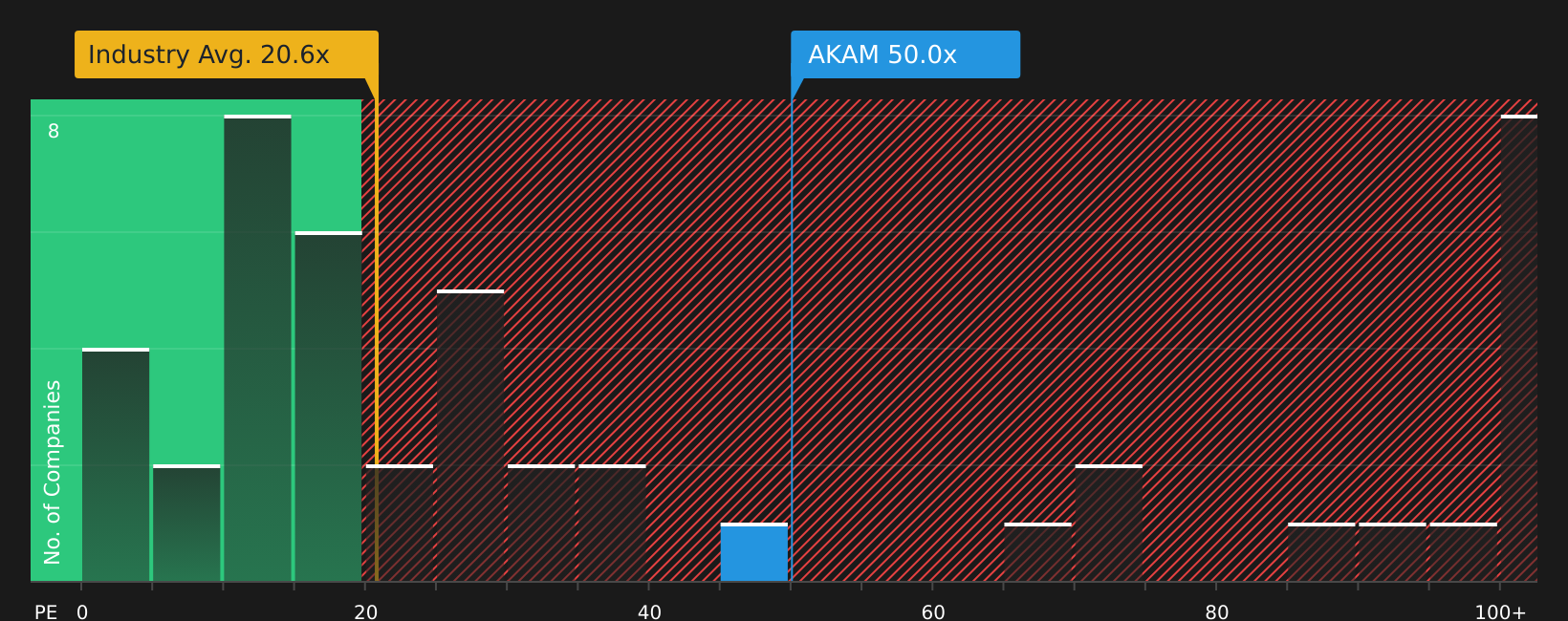

The most popular narrative leans on a fair value of $157.16, but the current P/E of 47.8x tells a different story. It sits above both the US IT industry at 20.4x and the estimated fair ratio of 35x, which points to richer pricing and less margin for error if expectations soften.

Next Steps

The mixed signals on valuation and momentum set a clear challenge, so act while the data is fresh and stress test your own thesis with the 1 key reward and 3 important warning signs.

Looking for more investment ideas?

If Akamai has sharpened your interest in tech and infrastructure, do not stop there. Broaden your watchlist with a few focused stock ideas that fit different playbooks.

- Target potential mispricings by scanning 46 high quality undervalued stocks that pair solid fundamentals with room for sentiment to catch up.

- Prioritize resilience and sleep better at night by checking 64 resilient stocks with low risk scores built around companies with steadier risk profiles.

- Add staying power to your portfolio by researching 10 dividend fortresses that combine higher yields with an emphasis on sustainability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.