Assessing Alcoa (AA) Valuation After Bull Flag Breakout And Shifts In Trading Sentiment

Alcoa Corporation AA | 71.53 | -0.74% |

Alcoa (AA) has caught traders' attention after a bull flag breakout, a move accompanied by heavier options trading and lower short interest. This is signaling a shift in how the market is positioning around the stock.

Those technical moves sit on top of a share price that has climbed to US$63.15, with a 90 day share price return of 65.36% and a 1 year total shareholder return of 76.05%. This suggests momentum has been building, even though the 30 day share price return of 3.84% signals a recent pause.

If Alcoa’s surge has you looking at the broader materials space, you might want to see what else screens well among 8 top copper producer stocks as another way to find metal producers on investors’ radar.

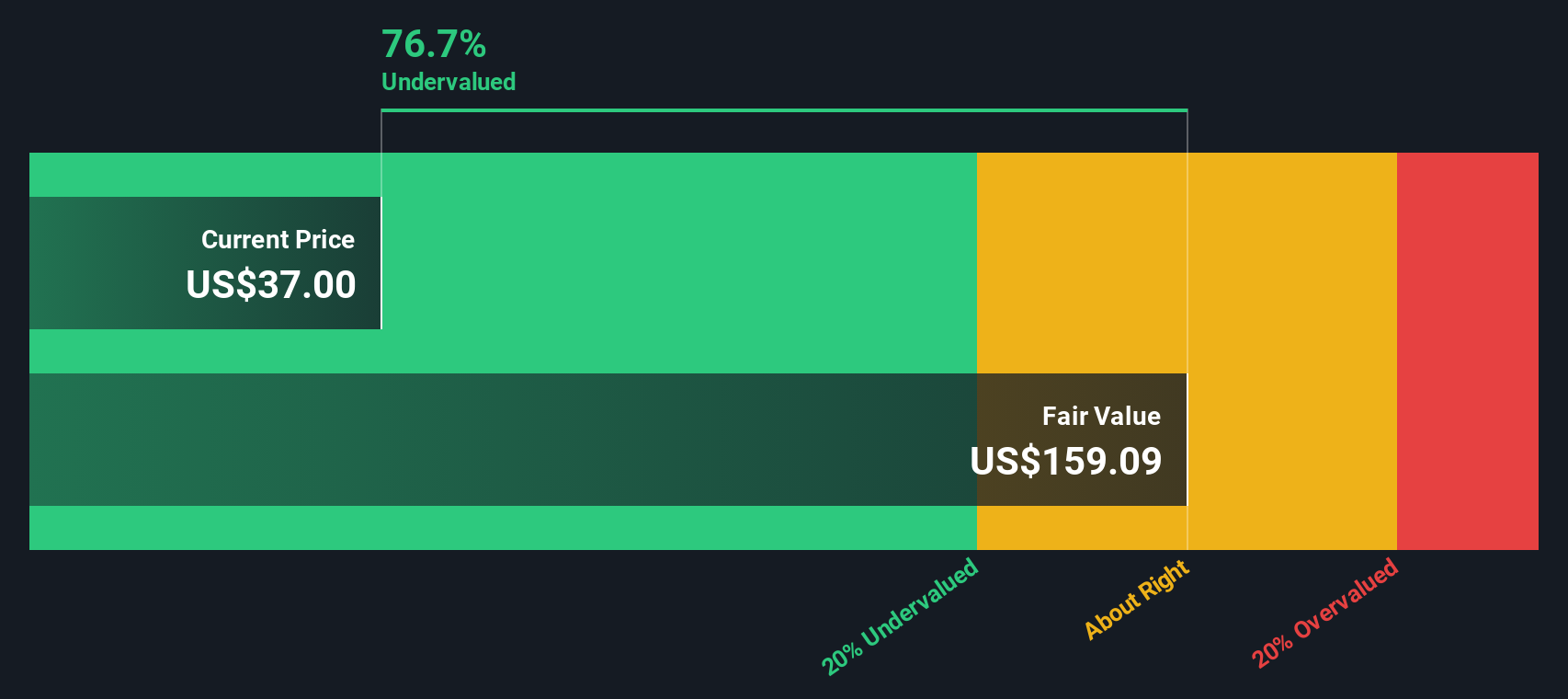

With Alcoa trading near US$63 and a long term intrinsic value estimate implying a 73% discount, yet sitting slightly above the average analyst price target, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 3.4% Overvalued

Alcoa’s last close at $63.15 sits slightly above the most followed fair value estimate of $61.08, which is built on detailed revenue and margin forecasts discounted at 8.53%.

Decarbonization trends, supply constraints, and sustainable product innovation are cited as factors that may support stronger pricing, improved margins, and resilient long-term growth amid shifting global demand.

This narrative is based on specific growth, profitability, and valuation multiple assumptions that could materially reshape Alcoa’s earnings profile over the next few years.

Result: Fair Value of $61.08 (OVERVALUED)

However, there is still a chance that stronger long term aluminum demand linked to decarbonization and wider adoption of low carbon products could support a higher earnings path.

Another Way to Look at Alcoa’s Valuation

The fair value narrative pegs Alcoa as 3.4% overvalued at $63.15 versus $61.08, but our DCF model points in a very different direction. On that view, the shares trade about 73% below an estimated future cash flow value of $237.67. When two frameworks are this far apart, which one do you trust more?

Build Your Own Alcoa Narrative

If you see the numbers differently or simply prefer to test your own assumptions, you can build a full Alcoa view in just a few minutes: Do it your way.

A great starting point for your Alcoa research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Alcoa is already on your radar, do not stop there. Fresh ideas across sectors can sharpen your watchlist and help you compare opportunities more effectively.

- Target value focused opportunities by checking out 51 high quality undervalued stocks that combine strong fundamentals with potentially attractive pricing.

- Prioritise resilience by reviewing 85 resilient stocks with low risk scores that score well on stability and lower risk metrics.

- Spot future contenders early with our screener containing 24 high quality undiscovered gems that many investors may not be watching yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.