Assessing Align Technology (ALGN) Valuation After Recent Share Weakness And Mixed Fair Value Signals

Align Technology, Inc. ALGN | 0.00 |

Recent share performance and business snapshot

Align Technology (ALGN) has drawn fresh attention after a daily share decline of about 3%, adding to pressure over the past month and past 3 months for the Tempe based dental device company.

The stock closed at US$161.71, with year to date performance still positive, while total return over the past year and past 3 years has declined. Over 5 years, shareholders have also experienced a pronounced decline in total return.

Behind the share price, Align generates US$4,095.789m in annual revenue and US$429.892m in net income, with reported annual growth in both revenue and net income. The business is anchored by its Clear Aligner segment, which contributes US$3,304.585m in revenue.

Systems and Services adds a further US$791.204m, reflecting the role of iTero scanners and related software and services in the overall model. The company reports a value score of 4, which some investors may use as one input when thinking about how the stock is currently priced.

Geographically, revenue is spread across the United States at US$1,642.355m, Switzerland at US$941.604m, and other international markets at US$1,511.83m. This mix gives Align exposure to both domestic and international dental and orthodontic demand.

The recent 1 day share price decline of about 3%, alongside a 30 day share price return down 5.9% and a 12 month total shareholder return down 10.2%, suggests momentum has been fading even as the business reports growth in revenue and net income.

If this kind of mixed performance has you thinking about diversification, it could be a good moment to scan other healthcare related opportunities, including 39 healthcare AI stocks.

With Align reporting annual growth in both revenue and net income while the share price has struggled over 1, 3 and 5 years, the key question is whether the current valuation offers a buying opportunity or if the market is already pricing in future growth.

Most Popular Narrative: 4.6% Overvalued

According to the most followed narrative, Align Technology's fair value is tagged at $154.62 compared with the last close at $161.71, which frames the stock as slightly ahead of that estimate and puts more focus on the reasoning behind the premium orthodontics thesis.

Align Technology is no longer proving that clear aligners work. It is proving that premium orthodontics can endure in a cost-sensitive world. For investors, ALGN represents a business built on medical credibility as much as consumer appeal. If Align continues to align innovation with clinical rigor, it may retain its leadership not through price competition, but through outcomes that justify the premium.

Curious what sits behind that premium story and a fair value just below today’s price? The narrative leans heavily on orthodontic margins, disciplined investment and a valuation multiple that assumes patients keep choosing Align for medically driven outcomes rather than discounts.

Result: Fair Value of $154.62 (OVERVALUED)

However, this premium story could be challenged if lower cost competitors win share faster than expected, or if orthodontists slow adoption of Align’s wider software ecosystem.

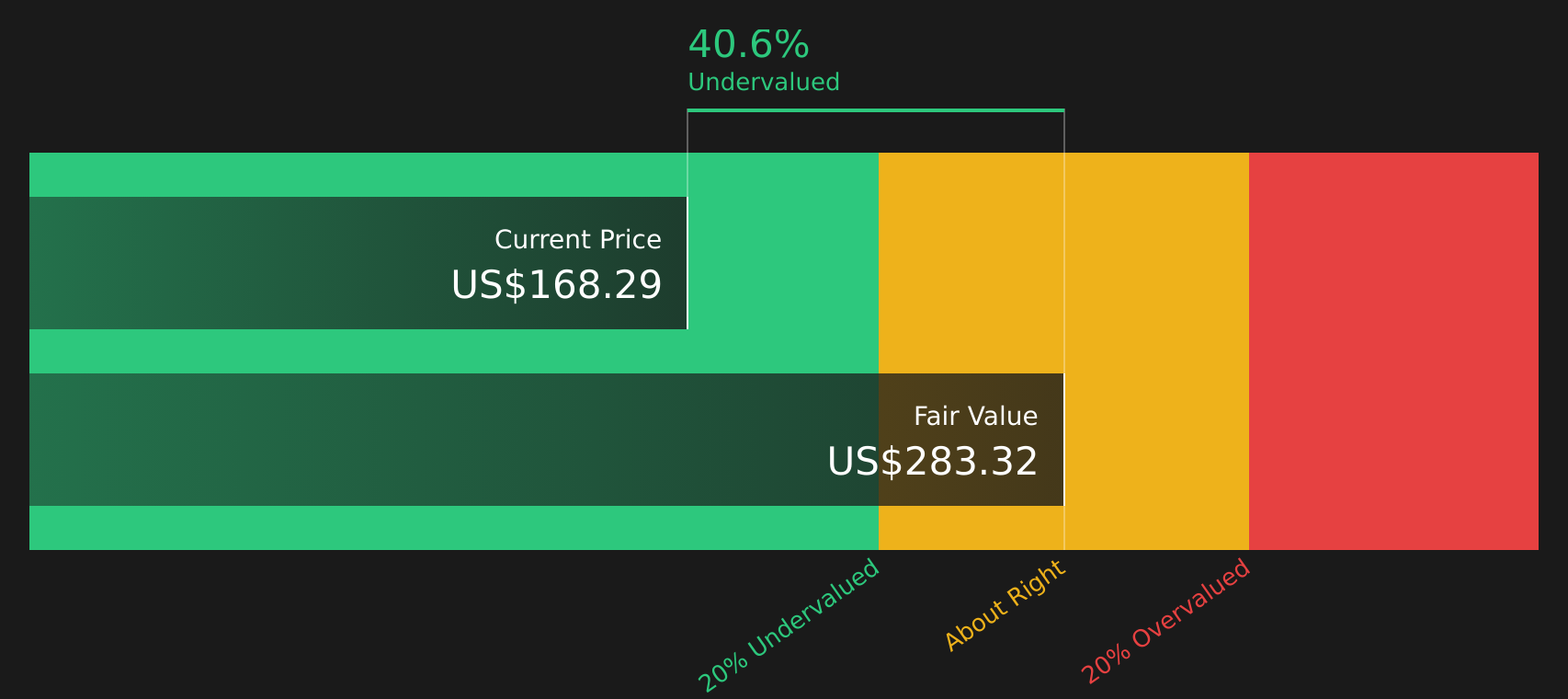

Another View: Cash Flows Point to a Different Story

That 4.6% overvaluation call sits awkwardly next to our DCF model, which puts Align's fair value at US$277.52 per share versus the current US$161.71. On this view, the stock trades at a steep discount. The key question is whether the cash flow assumptions are too generous or the market is being too cautious.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Align Technology for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on valuation and sentiment, it makes sense to look under the hood yourself and move quickly while views are still split, starting with the 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Align has you thinking harder about where to put your next dollar, do not stop here. Widen your search and give yourself more options.

- Spot potential bargains early by scanning for companies that look mispriced on quality and fundamentals with the 46 high quality undervalued stocks.

- Strengthen your income stream by reviewing companies with higher yields using the 10 dividend fortresses.

- Prioritise resilience by focusing on companies with solid finances through the solid balance sheet and fundamentals stocks screener (47 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.