Assessing Alliant Energy (LNT) Valuation As Battery Storage And Data Center Demand Shape Q4 Expectations

Alliant Energy Corporation LNT | 72.30 72.30 | -0.29% 0.00% Post |

Alliant Energy (LNT) is back in focus as investors look ahead to its fourth quarter 2025 earnings on February 19, with attention on the new 100 MW battery tied to its Grant County solar project.

The recent 2.2% 1 day share price return and 5.9% 90 day share price return to about $71, alongside a 1 year total shareholder return of 19.2%, suggest momentum has been building as investors react to the battery project and upcoming results.

If you are looking beyond utilities for other potential opportunities tied to the energy transition, it could be worth scanning 24 power grid technology and infrastructure stocks as a starting point for fresh ideas.

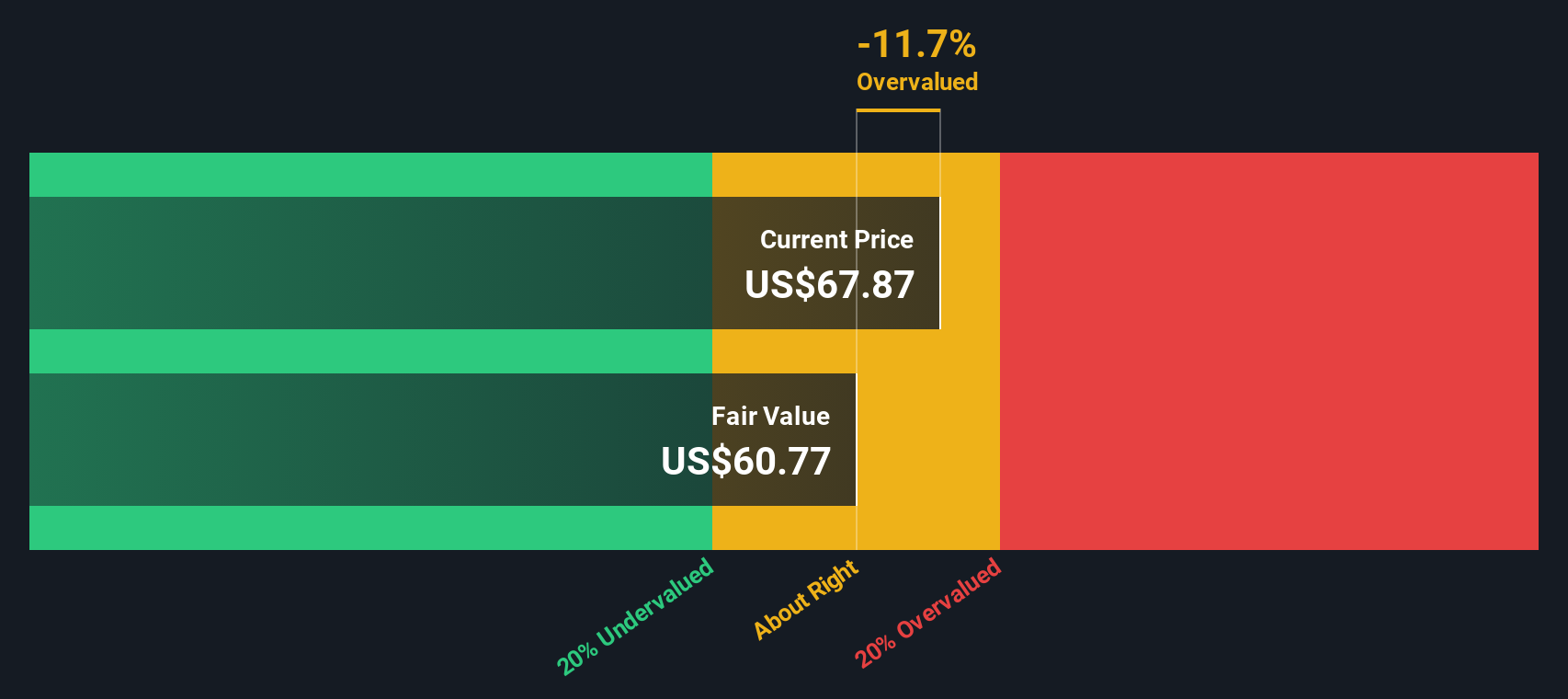

With Alliant Energy trading around $71, sitting only slightly below an average analyst target near $72 and with a value score of 2, you have to ask: is there real upside left here, or is the market already pricing in future growth?

Most Popular Narrative: 1.7% Undervalued

With Alliant Energy last closing at $71.19 against a narrative fair value of $72.45, the gap is quite small, which puts more weight on the underlying assumptions.

The accelerating construction and onboarding of large-scale data centers in Alliant's Midwest service areas highlight a strong, sustained uptick in electricity demand, directly linked to population and economic growth in the region, which is expected to drive significant increases in revenue and top-line growth over the next several years.

• The company's adaptive resource planning and regulatory flexibility in Iowa and Wisconsin allows rapid deployment of new generation capacity, positioning Alliant to capture higher allowed returns and efficiently expand its regulated asset base, supporting long-term earnings growth and margin expansion.

Curious how that demand story translates into the $72.45 fair value? The narrative leans heavily on steadier revenue, thicker margins and a premium earnings multiple. The exact mix might surprise you.

Result: Fair Value of $72.45 (UNDERVALUED)

However, that fair value story could shift quickly if large data center projects are delayed or regulators take a tougher line on rate approvals and returns.

Another View: DCF Points The Other Way

While the narrative fair value of $72.45 suggests Alliant Energy is 1.7% undervalued, our DCF model indicates a future cash flow value of $67.12. At a share price of $71.19, that implies the stock is trading above this estimate. Which perspective do you find more convincing?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Alliant Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of optimism and concern feels finely balanced, it is worth looking at the full picture yourself and deciding where you stand, including weighing up 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Alliant Energy has caught your attention, do not stop here. Broaden your watchlist now so you do not miss other opportunities lining up across the market.

- Target quality at a discount by scanning 55 high quality undervalued stocks that combine stronger fundamentals with prices that may not fully reflect their underlying strength.

- Build a steadier income stream by reviewing 13 dividend fortresses that focus on higher yields backed by more robust cash generation.

- Strengthen your core holdings with solid balance sheet and fundamentals stocks screener (44 results) featuring companies that pair healthier finances with more resilient business profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.