Assessing Amcor (AMCR) Valuation After Analyst Upgrades Berry Deal Synergies And Insider Share Purchases

AMCOR PLC AMCR | 39.93 | -1.89% |

Amcor (AMCR) is back in focus after a series of upbeat analyst views, reaffirmed fiscal 2026 guidance and fresh insider share purchases tied to its Berry Global acquisition and planned synergy gains.

Against this backdrop, Amcor’s share price has moved to US$8.65, with a 90 day share price return of 9.08% and a 30 day gain of 5.49%. This suggests momentum has been building, even as the 1 year total shareholder return of 2.68% decline and 3 year total shareholder return of 16.64% decline point to a weaker longer term record.

If the Berry Global deal and insider buying have your attention, it could be a good moment to scan the market for packaging peers and other fast growing stocks with high insider ownership.

With the shares at US$8.65, trading at what looks like a steep implied discount to some valuation estimates yet coming off weaker multi year returns, you have to ask: is there real upside here, or is the market already baking in future growth?

Most Popular Narrative: 16.9% Undervalued

Simply Wall St's most followed narrative puts Amcor's fair value at US$10.41 per share versus the current US$8.65. This frames the stock as trading at a discount that leans heavily on execution of the Berry deal and cash generation.

The integration of Berry Global with Amcor is expected to yield $650 million in synergies by fiscal 2028 (with $260 million in fiscal 2026), primarily through cost reduction, procurement optimization, and operational efficiencies, which should support sustained EPS and margin expansion.

This raises questions about what sits behind that synergy number and the projected shift in profitability and valuation multiples. The narrative hinges on a very specific earnings, margin and cash flow trajectory. Investors may want to see exactly which assumptions have to align for that US$10.41 fair value to make sense.

Result: Fair Value of $10.41 (UNDERVALUED)

However, there are clear pressure points, including high leverage at 3.5x and ongoing portfolio reviews that could result in asset sales or restructuring costs if conditions do not cooperate.

Another Take On Value

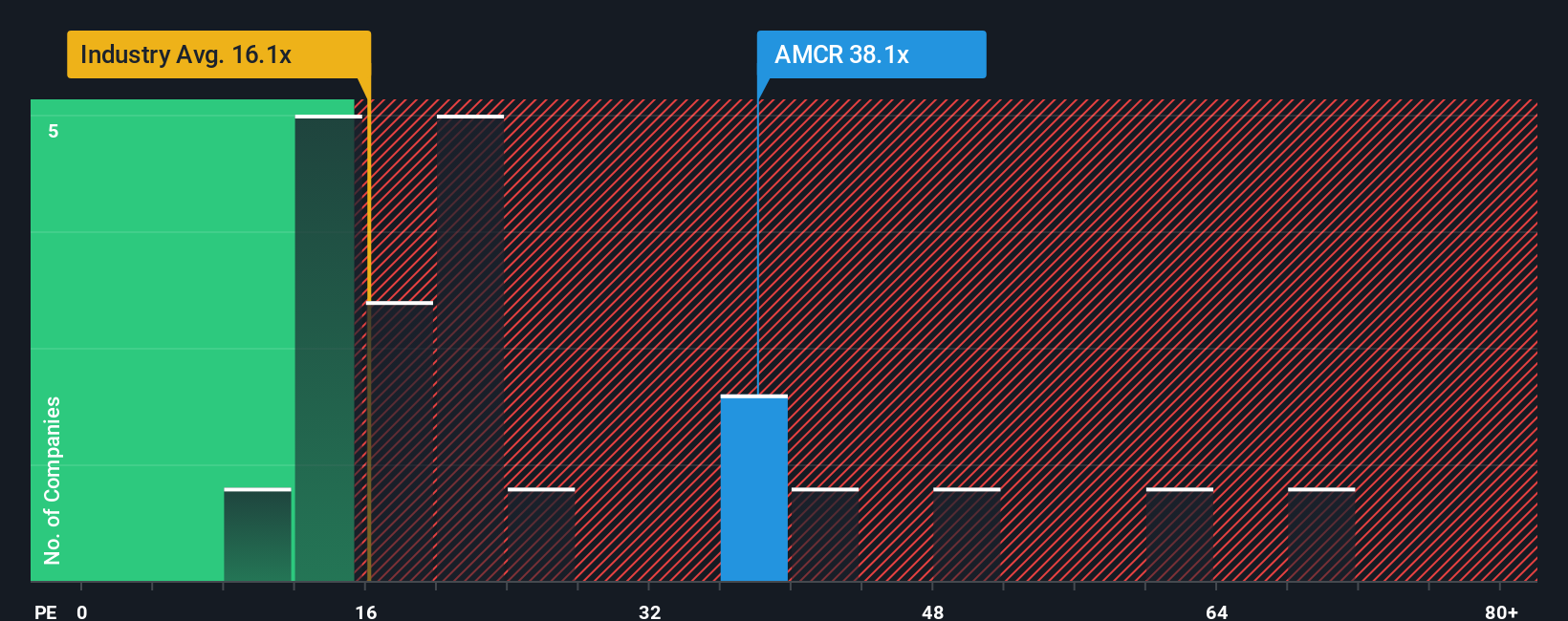

Those fair value estimates pointing to upside sit alongside a very different signal from the market multiple. Amcor trades on a P/E of 34.3x, compared with 20.9x for the North American packaging group, 22.1x for peers and a fair ratio of 25.2x. This suggests investors are already paying up for execution on Berry and profit recovery. The question is whether this is an opportunity that the cash flow work captures better, or a warning that expectations are already stretched.

Build Your Own Amcor Narrative

If you see the numbers differently, or prefer to evaluate the assumptions yourself, you can build a custom view in minutes with Do it your way.

A great starting point for your Amcor research is our analysis highlighting 3 key rewards and 5 important warning signs that could impact your investment decision.

Ready For Your Next Investing Idea?

Before you move on, take a moment to line up your next watchlist candidates with a few targeted screeners that surface ideas you might otherwise miss.

- Spot potential deep value by running the numbers across these 879 undervalued stocks based on cash flows that are flagging a discount based on cash flows.

- Explore the growth story in artificial intelligence through these 28 AI penny stocks that are tied to this fast evolving theme.

- Identify potential income ideas with these 12 dividend stocks with yields > 3% that already offer yields above 3% on current prices.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.