Assessing Amcor (AMCR) Valuation After Earnings Beat Berry Synergies And 2026 Guidance Reaffirmation

AMCOR PLC AMCR | 39.93 | -1.89% |

Amcor (AMCR) is back in focus after its latest quarterly update, where earnings came in ahead of expectations, revenue reflected the impact of the Berry acquisition, and management reaffirmed guidance for fiscal 2026.

The share price has reacted positively to this earnings beat and dividend increase, with a 1 day share price return of 2.97% and a 30 day share price return of 14.69%. The 1 year total shareholder return of 1.79% and 5 year total shareholder return of 6.03% show a more modest longer term picture, suggesting recent momentum has picked up after a relatively muted few years.

If Amcor's recent move has you thinking about where else capital is flowing in packaging related supply chains, it could be a good moment to check out 7 top copper producer stocks as a fresh set of ideas.

With earnings topping expectations, guidance reaffirmed and the Berry deal reshaping the business, the key question now is whether Amcor’s valuation still leaves upside on the table or if the market is already pricing in future growth.

Most Popular Narrative: 863.4% Overvalued

According to the most followed narrative, Amcor’s fair value of $5.00 sits far below the recent $48.17 close, creating a wide valuation gap to unpack.

Intrinsic Value (DCF) per share – Estimate: 4.85 dollars; Buffett’s preferred: Not applicable; Status: —; Explanation: A discounted cash flow model using TTM FCF of about 725 million dollars, 0% growth, 9% discount rate and 2.5% terminal growth yields intrinsic value around 4.85 dollars per share.

Want to see why such a low growth profile still supports that valuation gap? The tension between flat cash flows and a premium future earnings multiple sits at the heart of this narrative. The way it blends long run margins, payout assumptions and a richer profit multiple is where the real story lies.

Result: Fair Value of $5.00 (OVERVALUED)

However, if merger synergies, ROE recovery or deleveraging arrive faster than expected, this very large valuation gap could narrow sooner than the narrative implies.

Another View: Our DCF Model Flips the Script

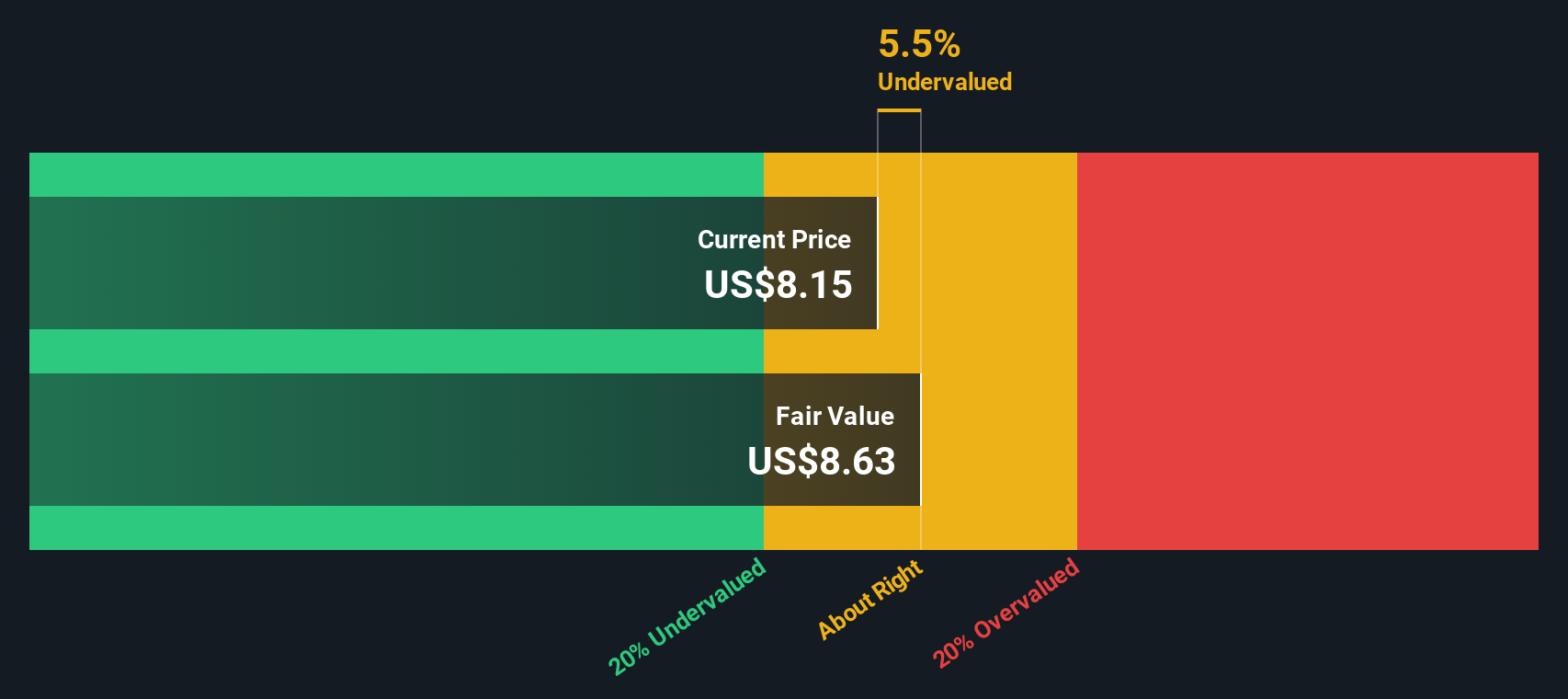

While the popular narrative leans on a low growth DCF and flags Amcor as heavily overvalued, our DCF model paints a very different picture. With a fair value estimate of $76.05 against the current $48.17 price, it suggests the shares trade at a sizeable discount. Which story do you think fits the business better?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Amcor for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Amcor Narrative

If this version of the story does not quite match your view, or you prefer to rely on your own work, you can build a custom thesis in just a few minutes with Do it your way.

A great starting point for your Amcor research is our analysis highlighting 2 key rewards and 5 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Once you have formed a view on Amcor, do not stop there. Broaden your watchlist with a few focused sets of stocks that fit clear themes.

- Target potential value opportunities by scanning companies that currently look mispriced using our list of 53 high quality undervalued stocks.

- Prioritise resilience by checking companies that score well on debt and liquidity using the solid balance sheet and fundamentals stocks screener (45 results) to stress test your ideas.

- Get ahead of the crowd by reviewing a screener containing 25 high quality undiscovered gems that most investors are not yet watching but already show solid fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.