Assessing American Eagle Outfitters (AEO) Valuation After Recent Share Price Momentum

American Eagle Outfitters, Inc. AEO | 0.00 |

Recent share performance and business snapshot

American Eagle Outfitters (AEO) has captured investor attention after a recent stretch where the stock gained about 13% over the past month, following a roughly flat move over the past 3 months.

At a last close of US$17.53 and a market value of about US$2.9b, the company sits at an interesting point for investors tracking apparel and specialty retail stocks tied to both in store and digital sales channels.

The past week’s 7.28% share price return and 30 day gain of 12.95% suggest short term momentum is building, even though the year to date share price return is down 33.50% while the 1 year total shareholder return is 79.03%.

If this mix of recent weakness and strong 1 year total shareholder return has you thinking about other consumer facing ideas, it could be a good time to scan 19 top founder-led companies.

With American Eagle Outfitters trading around US$17.53 and sitting about 12% below the average analyst price target, while recent annual revenue and net income growth are both positive, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 27% Undervalued

On the most followed narrative, American Eagle Outfitters’ fair value of about $23.89 sits well above the last close at $17.53, putting a spotlight on what is driving that gap.

American Eagle Outfitters is expanding brand awareness and strengthening customer engagement with targeted strategies, particularly for Aerie and OFFLINE. By increasing brand visibility and expanding collections, they aim to drive strong revenue growth.

Curious what turns that brand and channel story into a higher fair value estimate? The narrative focuses on revenue expansion, margin improvement, and a tighter share count as the key factors.

Result: Fair Value of $23.89 (UNDERVALUED)

However, softer early quarter sales and potential pressure from tariffs and currency moves could still weigh on revenue and squeeze margins if conditions worsen.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

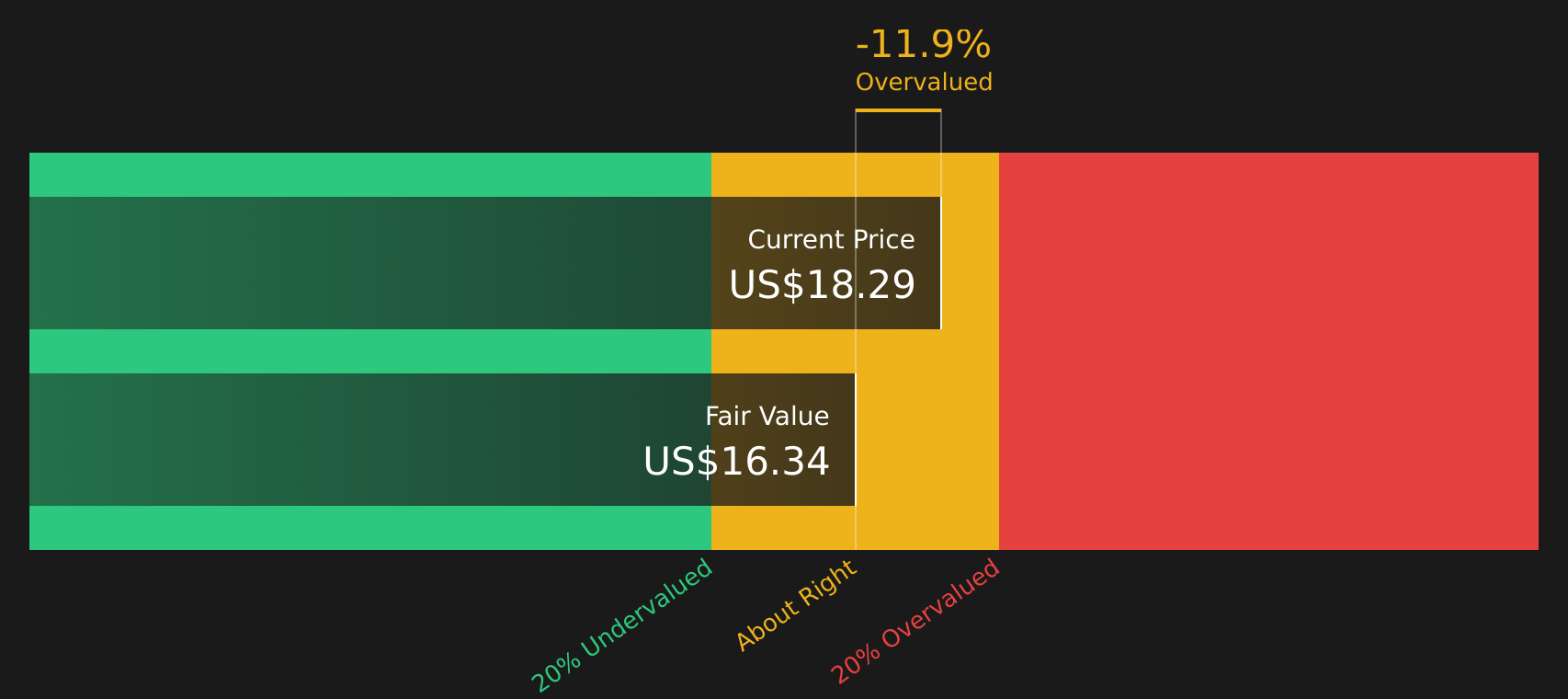

Another View on Valuation

The most followed narrative leans on future earnings assumptions, but the SWS DCF model points in a different direction. At $17.53, AEO is trading above an estimated future cash flow value of $16.24, which frames the stock as slightly overvalued on this measure and raises the question of how confident you are in long term cash flow forecasts.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out American Eagle Outfitters for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mix of optimism and caution across these valuation views makes it worth checking the underlying numbers yourself, then acting quickly if the story changes. To see both sides of the argument in one place, review the 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

If you stop here, you could miss other opportunities that fit your style, so use the tools available and keep pushing your research further.

- Target potential mispricings by scanning 47 high quality undervalued stocks that combine solid fundamentals with room for the market to reassess expectations.

- Focus on income by reviewing 9 dividend fortresses that pair higher yields with business profiles you can evaluate in detail.

- Reduce portfolio stress by checking 63 resilient stocks with low risk scores that show more resilient risk scores across a range of sectors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.