Assessing Apellis Pharmaceuticals (APLS) Valuation After Recent Share Price Momentum And Contrasting Fair Value Views

Apellis Pharmaceuticals, Inc. APLS | 0.00 |

Event context and recent stock performance

Apellis Pharmaceuticals (APLS) has drawn fresh attention after recent trading data showed the stock flat over the past day, slightly higher over the past month, and sharply positive over the past 3 months and year.

The latest share price of $40.97 sits alongside a 90 day share price return of 76.98% and a 1 year total shareholder return of 114.28%. The 3 and 5 year total shareholder returns remain negative, which indicates that recent momentum has strengthened after a weaker longer term experience.

If this kind of shift in sentiment interests you, it could be a good moment to see what else is moving in healthcare related AI by checking 35 healthcare AI stocks

With Apellis shares now near analyst targets but still flagged with an intrinsic discount, the key question is whether recent momentum leaves more room for upside or if the market is already pricing in future growth.

Most Popular Narrative: 0% Overvalued

The most widely followed narrative pegs Apellis Pharmaceuticals' fair value at about $40.93, almost identical to the last close of $40.97. This puts the focus firmly on the assumptions behind that figure.

The analysts have a consensus price target of $40.93 for Apellis Pharmaceuticals based on their expectations of its future earnings growth, profit margins and other risk factors. In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.3 billion, earnings will come to $158.6 million, and it would be trading on a PE ratio of 42.9x, assuming you use a discount rate of 7.3%.

Curious what justifies a premium earnings multiple on a business that only recently turned profitable? The narrative leans heavily on compounding revenue, wider margins, and a specific path for earnings power that is anything but conservative.

Result: Fair Value of $40.93 (ABOUT RIGHT)

However, you also need to weigh the risk that heavier free drug use, tighter funding for co pays, or tougher competition could pressure revenue and margins.

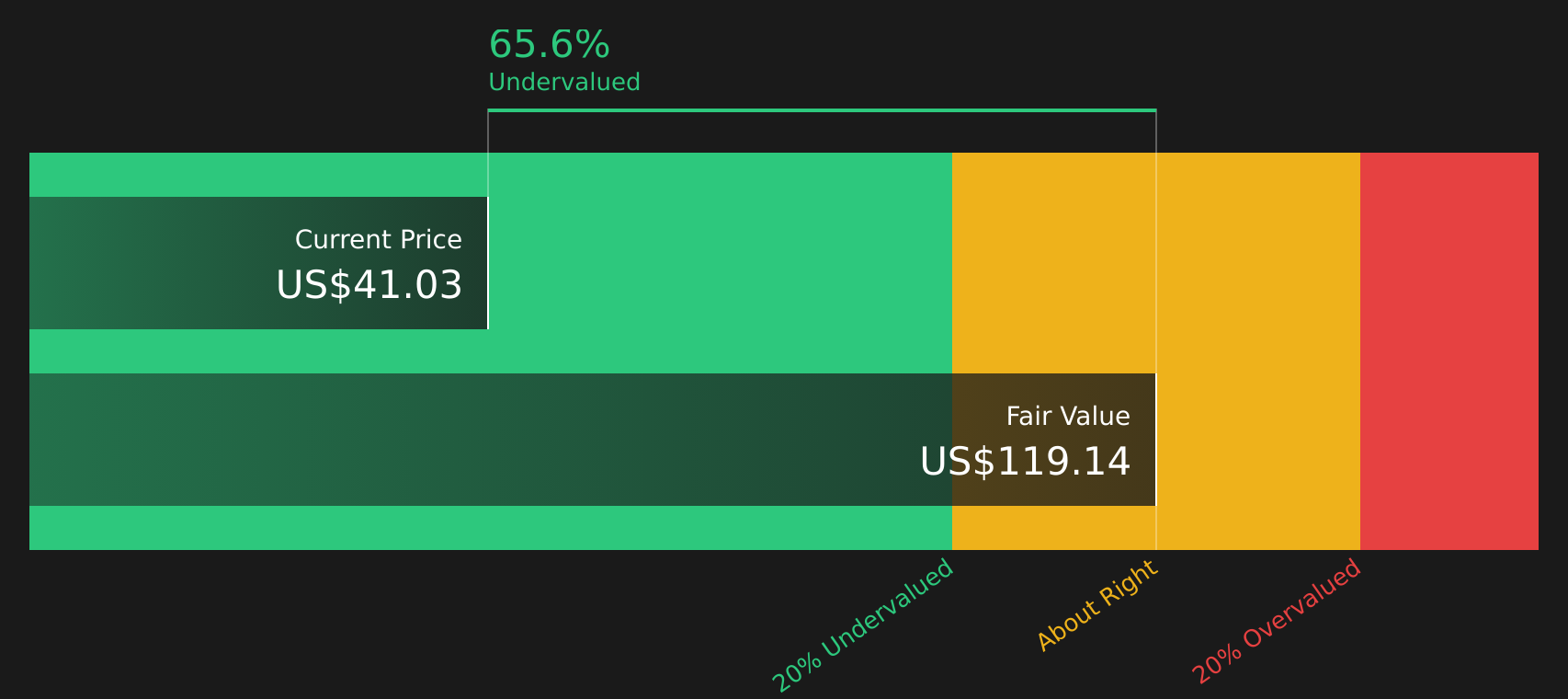

Another view: cash flow says something different

While the analyst target of $40.93 frames Apellis as fairly priced, the SWS DCF model points to a future cash flow value of $111.83 per share, which is far above the current $40.97. That gap raises a simple question: is the market underestimating what these drugs could earn over time?

Next Steps

With all this in mind, does the story so far feel balanced enough for you, or are you still on the fence? If you want to move quickly from headline moves to the underlying data, take a closer look at how analysts weigh both the upside and the potential downsides in the 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If Apellis has your attention, do not stop here. Broaden your watchlist with stocks that fit different roles in a portfolio, so you are not relying on a single story.

- Spot potential bargains early by scanning screener containing 25 high quality undiscovered gems, which pair solid fundamentals with less crowded investor attention.

- Strengthen the core of your portfolio by focusing on companies highlighted in the solid balance sheet and fundamentals stocks screener (46 results), which aim for resilience when conditions get tougher.

- Build a stream of potential income opportunities by reviewing the 13 dividend fortresses, which focus on higher yielding, established payers.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.