Assessing Apollo Global Management (APO) Valuation After Epstein Related Class Action Lawsuits

Apollo Global Management Inc APO | 0.00 |

Recent class action lawsuits have put Apollo Global Management (APO) under scrutiny, with plaintiffs alleging the firm misled investors about past communications with Jeffrey Epstein. The cases are raising questions around governance, disclosure practices, and potential regulatory exposure.

The lawsuits and Epstein related headlines have arrived while Apollo’s 30 day share price return is 21.88%, even though the year to date share price return is an 11.02% decline and the 1 year total shareholder return is a 2.15% loss. Recent momentum is therefore improving off a weaker base.

If this kind of rebound has you thinking beyond a single stock, it could be a useful moment to broaden your search and check out 17 top founder-led companies

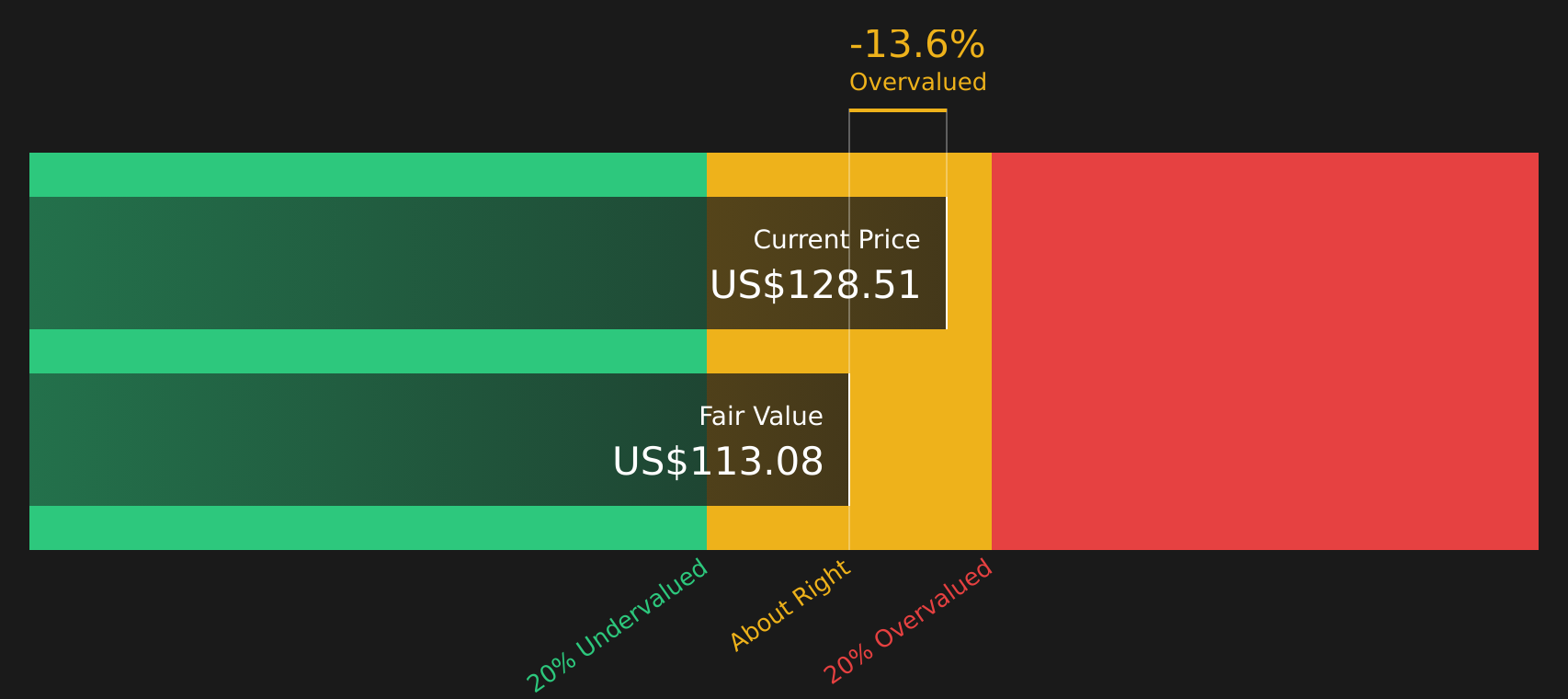

So with APO trading at about US$130.46, an indicated 22.7% intrinsic discount and only a small 6.6% gap to analyst targets, are you looking at a genuine value gap or a price that already reflects future growth?

Price to earnings of 21.5x: Is it justified?

Apollo Global Management is trading on a P/E of 21.5x, which screens as expensive relative to both the US diversified financials industry average of 17.5x and its own estimated fair P/E of 21.1x, despite the share price sitting below some intrinsic value estimates.

The P/E multiple reflects how much investors are currently willing to pay for each dollar of Apollo's earnings, which is a common yardstick for asset managers and alternative investment firms. At 21.5x, the market is assigning a premium to Apollo compared with the broader US diversified financials peer group and even relative to the peer average of 21.4x.

This premium suggests investors are paying up for expected earnings growth, with forecasts pointing to earnings growth of 18.4% per year. However, the current multiple is above the industry average and above the estimated fair P/E level that the SWS fair ratio model suggests the market could trend toward over time.

Result: Price to earnings of 21.5x (OVERVALUED)

However, this premium sits against risks such as ongoing Epstein related litigation and an 89.3% annual revenue decline, either of which could quickly challenge sentiment.

Another view on value

While the P/E of 21.5x appears expensive, the SWS DCF model presents a different perspective by indicating that Apollo Global Management’s shares at $130.46 are below an estimated future cash flow value of $168.75, which represents about a 23% difference. This raises the question of whether the market is underpricing cash flows or overpaying for near term earnings.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Apollo Global Management for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 50 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals like these can split opinion fast, so if you want to act with confidence, pressure test the story yourself by weighing up the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If APO has your attention, do not stop there. Casting a wider net now can reveal opportunities that might not stay mispriced for long.

- Target reliable cash generators backed by strong finances using the solid balance sheet and fundamentals stocks screener (44 results).

- Spot potential bargains before they get crowded by checking the 50 high quality undervalued stocks.

- Prioritize income and resilience by reviewing companies in the 13 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.