Assessing Arbor Realty Trust (ABR) Valuation After Weak Q1 Earnings And Higher Nonperforming Assets

Arbor Realty Trust Inc ABR | 0.00 |

Debt moves and liquidity after a tough quarter

Arbor Realty Trust (ABR) has just paired a weak first quarter earnings update, marked by higher nonperforming assets and impairment losses, with a sizeable refinancing move involving its legacy CLO 17 structure.

The company redeemed US$787.0 million of outstanding notes from CLO 17 at par and shifted about US$1.21b of related assets into two existing repurchase facilities with JPMorgan Chase Bank. Management reports these facilities carry pricing below CLO 17 and support leverage of roughly 76%, compared with about 68% in the CLO vehicle.

According to Arbor, the transaction created around US$132.3 million of additional liquidity and increased returns on the affected assets through higher leverage and lower funding costs. For investors weighing the stock after a difficult quarter, this financing shift sits alongside the earnings picture, including the recent impairment charge on real estate owned.

At a share price of US$5.91, Arbor Realty Trust has seen its 1 month share price return fall 27.57% and its year to date share price return decline 25.66%, while the 1 year total shareholder return is down 24.98%. This suggests sentiment has weakened despite the recent debt refinancing and follows a sharp drop in quarterly net income and an impairment on real estate owned.

If this kind of volatility has you looking at different opportunities in real estate related and income focused areas, it can help to see how other businesses are positioned. One useful next step is to scan a curated list of 20 top founder-led companies

With Arbor Realty Trust now trading at a discount to both recent analyst targets and some intrinsic value estimates after a weak quarter, investors face a key question: is this punishing sell off an opening, or is the market already factoring in future growth?

Price-to-earnings of 14.6x: Is it justified?

Arbor Realty Trust trades on a P/E of 14.6x, which screens as slightly cheap versus a fair P/E estimate of 15x, while still sitting above the wider US Mortgage REITs average of 12x.

The P/E multiple compares the current share price with earnings per share, so it effectively tells you how many dollars investors are paying today for each dollar of recent earnings. For a mortgage REIT like Arbor, this is a quick way to see how the market is weighing its income profile against peers that face similar interest rate and credit conditions.

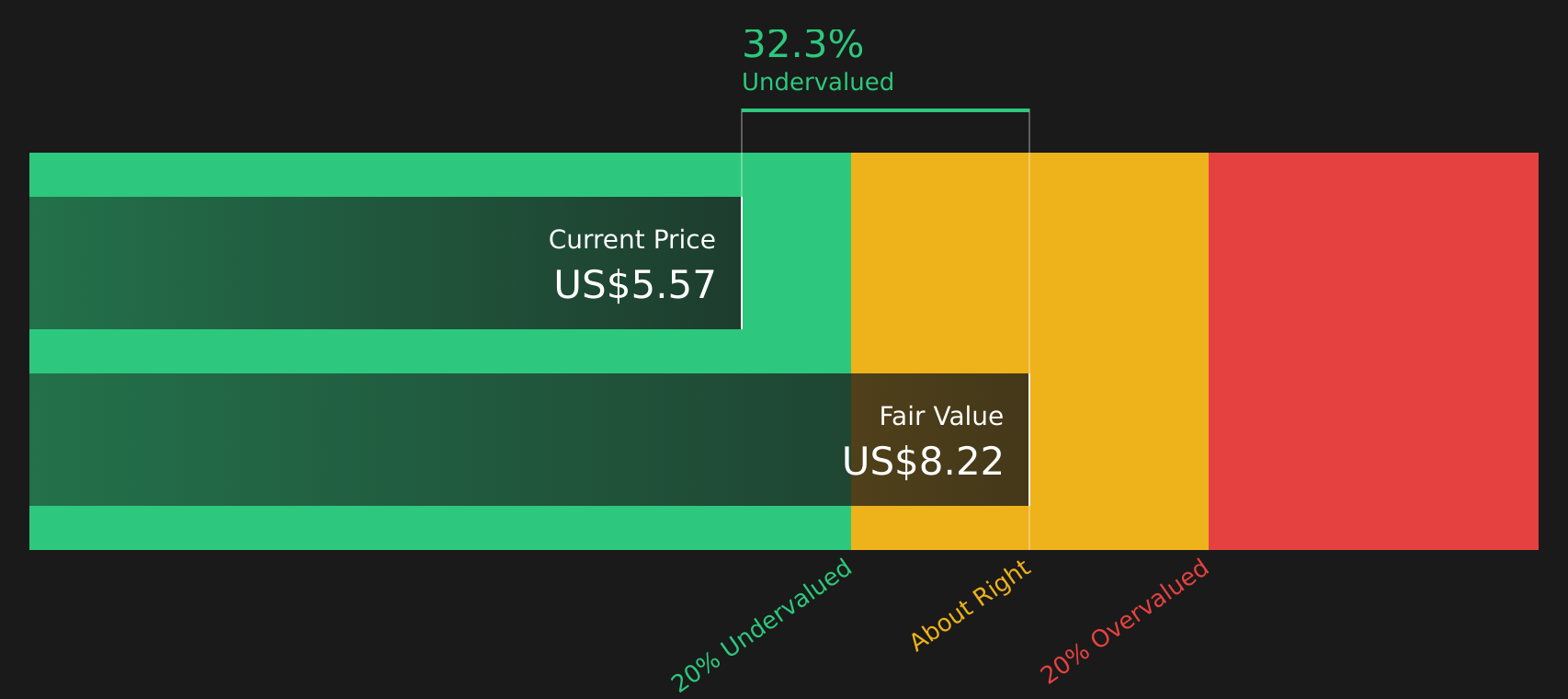

On one hand, Arbor is flagged as good value against fair value models, with the share price trading 28% below an internal fair value estimate and below an $8.21 future cash flow value from the SWS DCF model. On the other hand, its P/E of 14.6x is above the 12x industry average, which suggests the current price embeds higher earnings expectations than the typical US Mortgage REIT and could move closer to the estimated fair P/E of 15x if those assumptions hold.

Against its peer group, Arbor’s higher 14.6x P/E is a clear premium to the sector’s 12x average, while still a shade below the 15.3x peer average implied fair ratio. This implies the market is pricing in relatively stronger earnings than the broader industry but not at the top end of peer valuations that fair ratio work suggests could be possible.

Result: Price-to-earnings of 14.6x (ABOUT RIGHT)

However, the picture still carries clear risks, including revenue falling 47.69% annually and multi year total returns that have declined sharply, which could keep pressure on sentiment.

Another view: DCF points to a larger gap

While the 14.6x P/E looks roughly in line with the 15x fair ratio, the SWS DCF model tells a different story. With the stock at US$5.91 and future cash flow value estimated at US$8.21, the model suggests Arbor Realty Trust trades at a clear discount that investors will need to interpret for themselves.

For a closer look at how this cash flow view is built and what assumptions sit under it, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Arbor Realty Trust for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the mix of weaker recent results, refinancing moves, and a share price that screens below some valuation models, sentiment around Arbor Realty Trust is clearly divided. It makes sense to review the data for yourself and weigh the trade off between potential upside and the risks that concern other investors. To get a balanced view of both sides of the story, start with these 3 key rewards and 4 important warning signs.

Looking for more investment ideas?

If Arbor Realty Trust has your attention, do not stop here. Broaden your watchlist with a few focused stock ideas that could sharpen your next move.

- Target potential mispricing by scanning a curated list of 53 high quality undervalued stocks that pair solid fundamentals with attractive entry points.

- Strengthen your income stream by reviewing 10 dividend fortresses built around companies offering higher yields with an eye on durability.

- Reduce portfolio stress by checking 66 resilient stocks with low risk scores that prioritize resilient balance sheets and more defensive risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.