Assessing Archrock (AROC) Valuation After A Higher Dividend Signals Management Confidence

Archrock Inc. AROC | 36.10 | -0.58% |

Dividend increase puts Archrock in focus

Archrock (AROC) is back on income investors’ radar after its Board approved a higher quarterly dividend of $0.22 per share, or $0.88 on an annualized basis, for the fourth quarter of 2025.

That higher dividend comes on top of a strong run in the share price, with the stock at US$30.74 after a 1 month share price return of 18.87% and a 3 year total shareholder return of about 3.7x. Investors may weigh that recent momentum against income and risk.

If Archrock’s recent move has you thinking about other energy linked ideas, it could be a good moment to scan our list of 22 power grid technology and infrastructure stocks for more potential candidates.

With Archrock’s share price up strongly and the dividend reset higher, the key question now is whether the current valuation still leaves a margin of safety or if the market is already pricing in future growth.

Most Popular Narrative: 3.3% Undervalued

Archrock’s most followed valuation narrative pins fair value at roughly $31.78, slightly above the last close at $30.74. This puts this dividend move in the context of a stock seen as modestly undervalued.

The company's ongoing transformation to a modern, high-horsepower fleet and longer customer commitments (average contract duration now exceeding six years) is translating to higher margins, enhanced operational stability, and increased earnings visibility.

Want the full story behind that fair value? The narrative leans on steadier contracts, richer margins and a profit profile that assumes more than just incremental improvement. Curious which specific revenue and earnings targets sit under that $31.78 figure, and how sensitive the outcome is to a single input changing?

Result: Fair Value of $31.78 (UNDERVALUED)

However, that story can change quickly if U.S. natural gas demand softens, or if new regulations and technologies reduce the need for compression services sooner than expected.

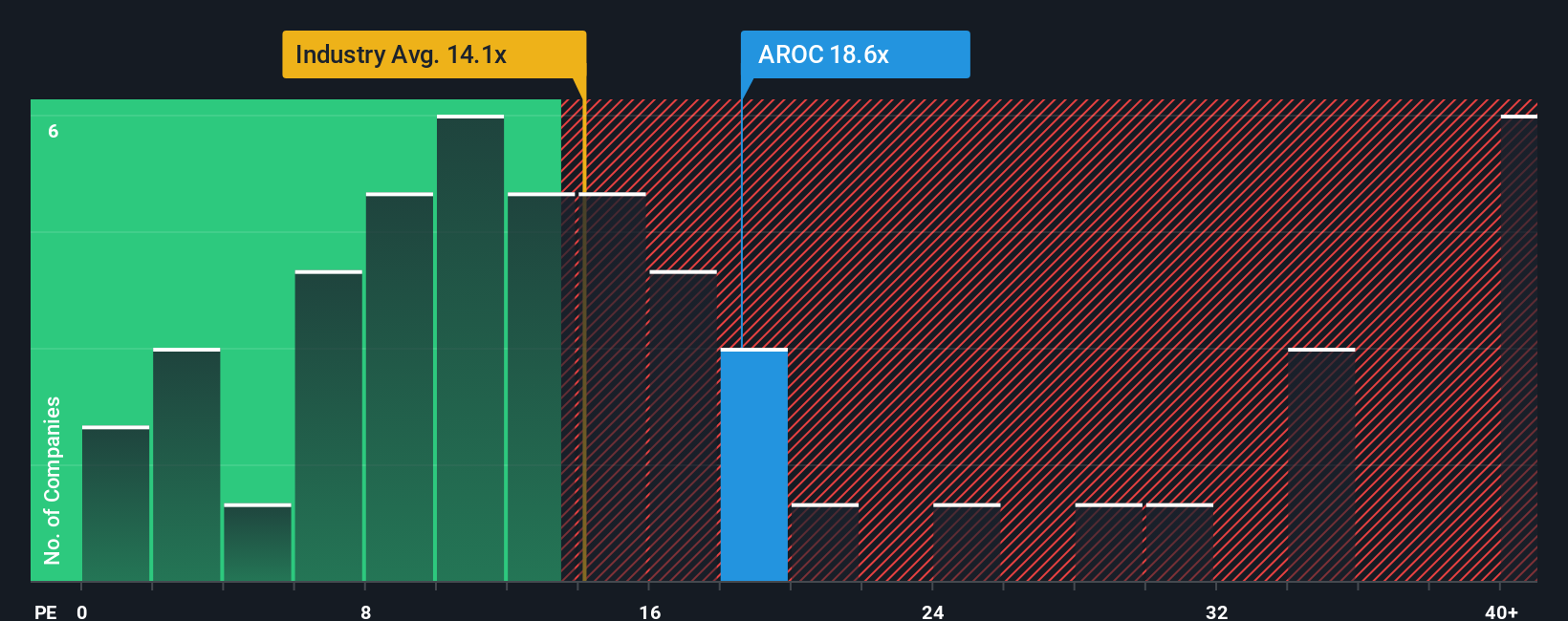

Another View: P/E Sends A Mixed Signal

That 3.3% discount to fair value sits next to a more cautious message from the P/E. At 20.6x earnings, Archrock trades above its fair ratio of 18.8x, yet below the US Energy Services peer average of 23.4x. Is the stock being priced for comfort or for stretch?

Build Your Own Archrock Narrative

If you see the numbers differently or simply want to test your own assumptions, you can build a complete Archrock view in just a few minutes by starting with Do it your way.

A great starting point for your Archrock research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Archrock has you thinking more broadly about your portfolio, now is a good time to widen the net and size up other potential opportunities with clear, data driven filters.

- Target income resilience by checking out 15 dividend fortresses, a set of names with higher yields that may appeal if you want your portfolio to work harder for you.

- Hunt for potential mispricing with 54 high quality undervalued stocks, where you can focus on companies that our model flags as trading below their assessed worth.

- Prioritise capital protection using 79 resilient stocks with low risk scores, so you do not miss companies that score better on our internal risk checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.